Dear New World Investor:

So the Fed continued their pause and said they don’t see inflation reaching 2% until 2025, which implies these rates or higher for another 18 months to two years. I expect a new record length of time between the last rate hike and the first rate cut.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

That’s not what was expected, which was inflation nearly tame by the end of 2024 and rates coming down, but my reaction is GOOD. We need to get back to a normal financial environment, where capital has a price (5% for 10 year bonds seems about right to me), savers get paid, and companies that can’t earn rates of return higher than their cost of capital go out of business. In that environment, high Return On Investment (ROI) companies like – you guessed it – technology get a well-deserved premium valuation.

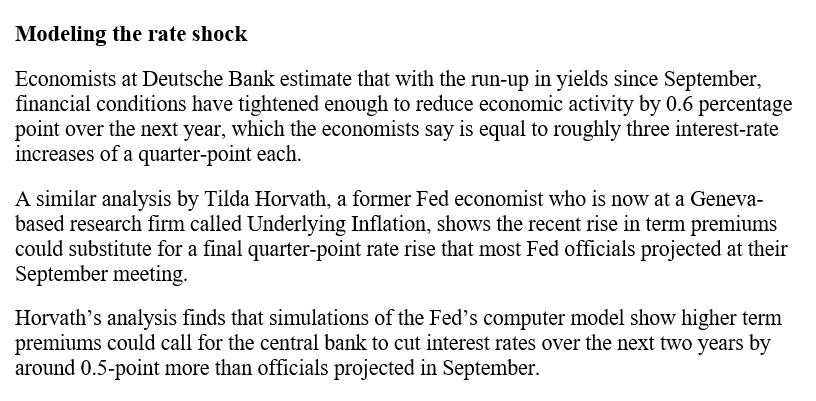

The Fed continues to normalize its balance sheet – another healthy move – by letting bond mature. Several forecasters say the recent tightening in financial conditions could be worth between half a percentage point and a full percentage point (50 to 100 basis points) in Fed-funds-rate equivalent increases.

Click for larger graphic h/t @NickTimiraos

Click for larger graphic h/t @NickTimiraos

Even though Powell said: “The Fed did not put a recession back into their forecast,” I still think we are headed for a shallow, brief recession, probably in the March and June quarters. Americans have a way of making holiday spending happen, so while the December quarter will be weak (the Atlanta Fed’s GDPNow model is at +1.2% while the Blue Chip economists are at +0.9%), it will be up. Then the used-up-covid-savings/credit card debt/student loan repayments should tip the economy into a two or three quarter mild recession, just in time for the Presidential election.

Things are weakening pretty quickly. The ISM Manufacturing PMI reported a surprise turn to further contraction, 46.7 versus 49 prior and the 49 estimate. Below 50 is contraction. Manufacturing Employment was 46.8 versus 51.2 prior and the 50.3 estimate. Manufacturing New Order were 45.5 versus 49.2 prior.

I think that Powell is being smart and prudent in waiting to see what the lag effects are going to do because this is the most aggressive Fed rate hike campaign in all of our lifetimes.

Market Outlook

The S&P 500 added 200 points and 4.4% since last Thursday, with yesterday benefiting from the biggest daily drop in yields since March. After its first three-month losing streak since March 2020, the Index is up 12.5% year-to-date. The Nasdaq Composite gained 5.5% thanks to good September quarter earnings and falling interest rates. It is up 27.0% for the year. The benchmark small-cap index, the Russell 2000 climbed 3.5% but still is down 2.7% in 2023. Last Friday, it hit the lowest levels since November 2020, when the world was still without a vaccine and shut down from Covid.

Click for larger graphic

Click for larger graphic

Both professionals and retail are overwhelmingly negative. The Goldman Sachs Prime book was sold for the third straight month in October. The main reason is heavy shorting. Goldman notes: “The combined net selling from August to October across global equities was the second largest over any three month period in the past 10 years (only Q1:22 was larger) and ranks in the 99th percentile.”

Good luck explaining to your boss that you shorted the recent lows in size and intend to keep that into yearend.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The spread between AAII bulls minus bears has cratered and is trading at the lowest levels since May. The move lower in the spread has been brutal. The bounce in equities is surely frustrating the new bears.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The fractal dimension reversed quickly, showing the most recent decline is just consolidation of the prior uptrend, not a new downtrend. I expect this back-and-forth volatility to continue for a while, if only because of Ukraine and Israel, but the yearend rally is still on.

Top 5

Changes this week: None

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO valuation

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, November 3

ACRDF – Acreage Holdings – Unspec. – Business of Cannabis: New York

October payrolls – 8:30am – +180,000 expected; September was +336,000

Sunday, November 5

Back to Standard Time – 2:00am – “Spring forward; Fall backward”

Monday, November 6

SAND – SandStorm – After the close – Earnings release; call tomorrow

VLD – Velo3D – 5:00pm – Earnings conference call

Tuesday, November 7

SAND – SandStorm – 11:30am – Earnings conference call

GILD – Gilead – 4:30pm – Earnings conference call

QUIK – QuickLogic – 4:35pm – Radiation Hardened Electronic Technologies Conference

ENVX – Enovix – 5:00pm – Earnings conference call

Wednesday, November 8

SFTBY – SoftBank – 3:30am – Earnings conference call

AKBA – Akebia – 8:00am – Earnings conference call

CDE – Coeur Mining – After the close – Earnings release; call tomorrow

NVTA – Invitae – 4:30pm – Earnings conference call

RKLB – Rocket Lab – 5:00pm – Earnings conference call

Thursday, November 9

CDE – Coeur Mining – 11:00am – Earnings conference call

Short Interest – After the close

INO – Inovio – 4:30pm – Earnings conference call

APTO – Aptose Therapeutics – 5:00pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $177.57) reported after the close today. September quarter revenues dipped 0.7% from last year to $89.49 billion, in line with the $89.34 billion consensus estimate. Earnings per share grew 13% to $1.46, beating the $1.39 estimate. (Conference call TRANSCRIPT HERE.)

iPhone sales rose 2.7% from last year to a September quarter record of $43.8 billion versus the $44.00 billion estimate. Mac sales were $7.61 billion, well short of the $8.50 billion estimate. iPad sales of $6.4 billion were just above the $6.14 billion estimate. Wearables, Home, and Accessories came in at $9.32 billion compared to the $9.40 billion estimate. The important Services group booked an all-time high $23.31 in sales, up 16.3% year-over-year and above the $21.42 billion estimate.

They guided for December quarter revenue flat with last year’s $117.2 billion.

On Monday, Apple introduced their “scary fast” M3 family of processors powering a new iMac and the MacBook Pro 14” and 16”. The new M3, M3 Pro and M3 Max processors use 3-nanometer technology and include GPU upgrades. The M3 Max has a 16-core CPU, a 40-core GPU, and comes with 128GB memory. Ray tracing, traditionally reserved for high-end GPUs, is available as part of the new M3 chips and is now available on the Mac.

The new 14-inch MacBook Pro with the M3 chip is 60% faster than the 13-inch MacBook Pro with the M1. It starts at $1,499.

The 16-inch MacBook Pro with either the M3 Pro or M3 Max chip is 40% faster than the 14-inch MacBook Pro with the M1. It starts at $2,499. Both new MacBook Pro laptops have 22 hours of battery life, a 1080p camera, and a six-speaker sound system.

The updated iMac desktop with the M3 processor and a 4.6K Retina display is twice as fast as the M1-equipped predecessor. It starts at $1,299 for the eight-core version or $1,499 for the 10-core processor.

Wedbush said the negative groupthink on Apple is way overdone. They wrote: “The overall sentiment of Apple on the Street is a negative ‘groupthink mentality.’ That’s very disconnected from the current iPhone 15 growth we see in the field based on our recent checks and trip to Asia that gives us a high level of confidence in owning Apple at these levels.”

Wedbush believes over 100 million iPhones in China alone are “in the window of an upgrade opportunity and that remains the golden goose on this cycle for Apple with a very heavy mix of iPhone Pro this time.” They maintained their Outperform rating on the stock with a $240 price target. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $81.23) reports next Tuesday after the close. The consensus is expecting $6.42 billion in revenues and $1.81 per share. For the December period, they expect guidance for $6.72 billion in sales and $1.89.

Gilead’s Kite subsidiary is collaborating with Epic Bio to use Epic’s proprietary gene regulation platform to develop next-generation cancer cell therapies. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $310.87) has developed a strong competitive advantage due to its scale and network effects. They have numerous growth avenues including Average Revenue Per User growth outside North America, WhatsApp monetization, AI, and the metaverse. The stock still trades at a cheap valuation relative to the S&P 500 considering their above-market growth potential.

As for timing, a partial position here as it heads for the upper Bollinger Band with subsequent buys on pullbacks to the lower Bollinger Band makes sense.

Click for larger graphic

Click for larger graphic

META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $21.07) reports next Thursday with a conference call at 3:30am EST. I’ll be looking at recent Vision Fund results and what they are going to do with the ARMplc IPO proceeds. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $10.23) closed the Routejade acquisition, giving them vertical integration of electrode coating and battery pack manufacturing, while adding an established lithium-ion battery business with two factories in Korea, along with complementary products, customers, and suppliers. With coating now vertically integrated, Enovix can realize significant cost savings while speeding up battery development cycles as modern materials are quickly incorporated to improve energy density. Securing the coating supply chain also ensures that incoming battery materials are the highest quality available, which positively impacts manufacturing yield and throughput, reducing costs.

They also report next Tuesday after the close. Wall Street wants to see just $120,000 in revenues and a loss of 23¢ per share, with December period guidance for $530,000 in sales and a 24¢ loss. With the change in strategy they can’t make the December revenue number. The most important information will be an update on Fab2 in Malaysia. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $16.47) reported September quarter revenues up 17.8% from last year to $127.8 million, just above the consensus expectation for $126.9 million. The pro forma loss of six cents a share was smaller than the eight-cent loss Wall Street expected.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said their Dollar-Based Net Expansion Rate – the amount of money a customer spent this year compared to last year – was 120%. They had 3,102 customers in the third quarter, up 30 from the second quarter. 547 were enterprise customers and the average enterprise customer spend was $858,000, up 5% quarter-over-quarter.

They guided the December quarter to total revenue between $137 million and $141 million compared to the consensus of $140.21 million. The pro forma loss should be one cent to five cents, better than the four-cent loss consensus. For the full year, they now see total revenue of $505 million to $509 million versus the consensus of $506.63 million, with a pro forma loss of 19¢ to 23¢ per share. The consensus was expecting a 24¢ loss.

The stock was up 15.6% today on these results. They finished the quarter with $4428.3 million in cash. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $4.59) reports next Wednesday after the close. Due to the one launch failure, the consensus is expecting $68.91 million in revenues and a loss of nine cents a share. For the December quarter, they think RKLB will guide for $85.22 million in sales and another nine-cent loss. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $1.31) reports Monday after the close. The two publishing analysts are looking for $27.00 million in revenues and an eight-cent per share loss. For the December period, they want to see guidance for $29.69 million in sales and a six-cent loss.

The company appointed Schoeller-Bleckmann Oilfield Technology, a manufacturer of high-tech metal components with more than 100 years in business, as its sole contract manufacturing partner operating in the DACH region, which includes Germany, Austria, and Switzerland. Schoeller-Bleckmann will also be Velo3D’s sole contract manufacturing partner for Europe’s oil and gas industry, which is the primary industry it serves. They will add another Sapphire printer to their two existing printers, including a Sapphire XC.

Italian contract manufacturer Ci-Esse Srl bought a Sapphire printer to enhance its additive manufacturing capabilities, providing mission-critical metal parts to its aerospace, defense, and motorsports customers. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $0.88) reports next Wednesday before the open. Although the vadadustat approval in March is the big stock driver, Auryxia sales are still important. Consensus expectations are for $48.18 million in revenues and an eight-cent loss per share. For the December quarter, guidance is expected to be for $52.41 million in sales and a six-cent loss. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after FDA approval in March 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat PDUFA is March 27.

Probable time of next FDA approval: March 27, 2024

Probable time of next financing: Late 2024 or never

Aptose Biosciences (APTO – $2.93) presented surprisingly good interim results from the tuspetinib/venetoclax doublet trial in acute myeloid leukemia (AML) (WEBINAR HERE and SLIDES HERE).

Chief Medical Officer Rafael Bejar, MD, PhD, said: “We are really pleased by our growing safety and efficacy data on tuspetinib in very difficult-to-treat AML patient populations. This includes activity in FLT3-unmutated patients, a population that accounts for more than 70% of AML and has few effective treatment options. Additionally, tuspetinib’s significant activity in patients who have failed venetoclax treatment – a rapidly-emerging population of particularly high unmet medical need – provides a clear development pathway for tuspetinib with the potential for accelerated approval.”

Aptose anticipated dosing up to 30 patients with tuspetinib/venetoclax by the European School of Hematology 2023 Conference, but investigator enthusiasm resulted in dosing 49 patients as of October 23, and patients continue being enrolled.

91 other patients have received tuspetinib as a single agent with an excellent safety profile. It delivered a 42% Complete Remission (CR) rate across all patients and a 60% Complete Remission with Incomplete Hematologic Recovery (CRh) response rate across FLT3-mutated patients, among evaluable VEN-naïve patients at the 80mg daily recommended Phase 2 dose.

Tuspetinib demonstrated a 29% CR/CRh rate in VEN-naïve FLT3 unmutated (wild type) AML at 80 mg daily, unlocking the potential for tuspetinib to treat the additional 70% to 75% of the AML population without FLT3-mutation not currently addressed by any approved drugs.

Click for larger graphic

Click for larger graphic

Upcoming news to drive the stock:

* * They report next Thursday after the close and will go over this data again, maybe with an update on the patient count.

* * Next tuspetinib/venetoclax data readout (November data cutoff) at American Society of Hematology December 9-12 (This is a big one – lots of partner/merger deals after ASH)

* * Phase 2 trial extension into Higher-Risk Myelodysplastic Syndrome (HR-MDS) and Chronic myelomonocytic leukemia (CMML) by yearend

* * Tuspetinib/venetoclax data on duration of response in R/R AML in March and June quarters

APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Arch Therapeutics (ARTH – $0.96) said AC-5 will be featured at the 2023 Symposium on Advanced Wound Care Fall Meeting. This Saturday, November 4, they’ll present a clinical case poster on treating three large recalcitrant 20-year-old venous leg ulcers.

Then, on Sunday, AC5 will be featured in the Advanced Wound Care Therapy for the Lower Extremity: Hands-On Skills Lab. In this demonstration workshop, attending clinicians will be provided both hands-on experience with AC5 and an opportunity to learn about its mechanism, preparation, application, and utility in various wound types. ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2024

Probable time of first FDA approval: External done. Internal 2025

Probable time of next financing: December 2023 quarter

Compass Pathways (CMPS – $5.95) reported a September quarter loss of 67¢, much worse than the 46¢ loss expected. On the conference call (AUDIO HERE and SLIDES HERE), management said it’s expensive to start-up Phase 3 trials as new clinical sites are chosen and trained.

The company is preparing for scale at launch:

Click for larger graphic

Click for larger graphic

And they are more than COMP360 for treatment-resistant depression.

Click for larger graphic

Click for larger graphic

We’ll get data from the Phase 2 PTSD trial before the end of this year, Phase 3 trial 1 next summer, and Phase 3 trial 2 in mid-2025. Their US patents expire in 2038, and they will apply for five years of patent term extension.

They finished the quarter with $238.0 million in cash, enough to carry them to late 2025, and will only burn $9 million to $15 million in the December quarter. They adjusted their full year cash burn guidance lower to $79 million to $85 million. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inovio (INO – $0.39) reports next Thursday after the close (busy day!). The consensus thinks they’ll do $120,000 in revenues and lose 13¢ per share. For the December period, they expect guidance for $140,000 in sales and another 13¢ loss. As always, it will be updates to their various trials that move the stock. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: 2025

Invitae (NVTA – $0.63) reports next Wednesday after the close. Wall Street expects $120.76 million in revenues and a 31¢ loss per share. For December, they expect guidance for $126.85 million in sales and another 31¢ loss. I expect the cash burn to be less than Wall Street expects, which is the key to a recovery in the stock. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.16) did the right thing, told Nasdaq to shove it, and delisted to the pink sheets and their Toronto Stock Exchange listing. The symbol stays the same for now. The CEO said: “Our Board of Directors concluded that within the context of the current biotech markets, the Company and its stockholders do not benefit from a Nasdaq listing considering the associated significant costs and resources required. We remain in good standing with our TSX listing, have no debt and have sufficient cash to potentially fund the company well beyond key value inflection milestones from the MDNA11 Phase 2 monotherapy and combination trial. We look forward to sharing additional new data at major conferences next month for the MDNA11, BiSKITs and bizaxofusp programs.”

The stock took a hit, but the way forward is continued successful clinical trials. The stock will go up then whether it’s on Nasdaq or not.Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

TG Therapeutics (TGTX – $10.41) reported a strong September quarter with $25.1 million in Briumvi sales and the $140 million license revenue from Neuraxpharm combining to produce $165.82 million in revenues compared to the – oops – $63.34 million estimate. GAAP earnings per share of 73¢ clobbered the 17c estimate.

On the conference call (AUDIO HERE), management said they have had about 2,200 Briumvi prescriptions since the launch from over 500 healthcare providers across approximately 350 centers in the US. Payer coverage is in place for approximately 95% of covered lives.

I expect more than $30 million in Briumvi sales in the current quarter. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

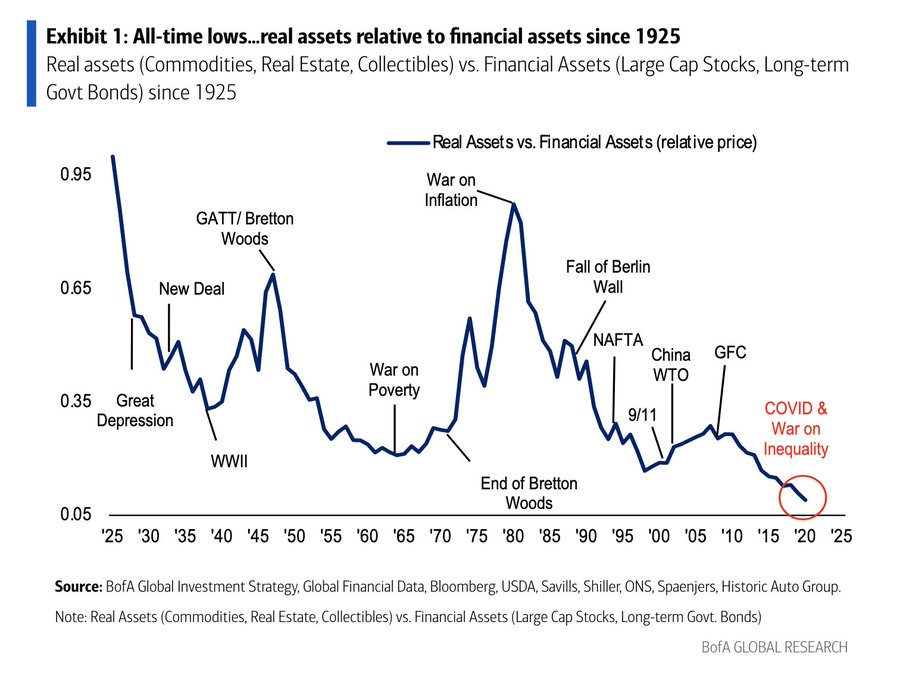

Commodities

Hard assets are at their lowest relative price since 1925. Unless you think we are about to slip into deflation – possible, but not very likely – you need to own some of these.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

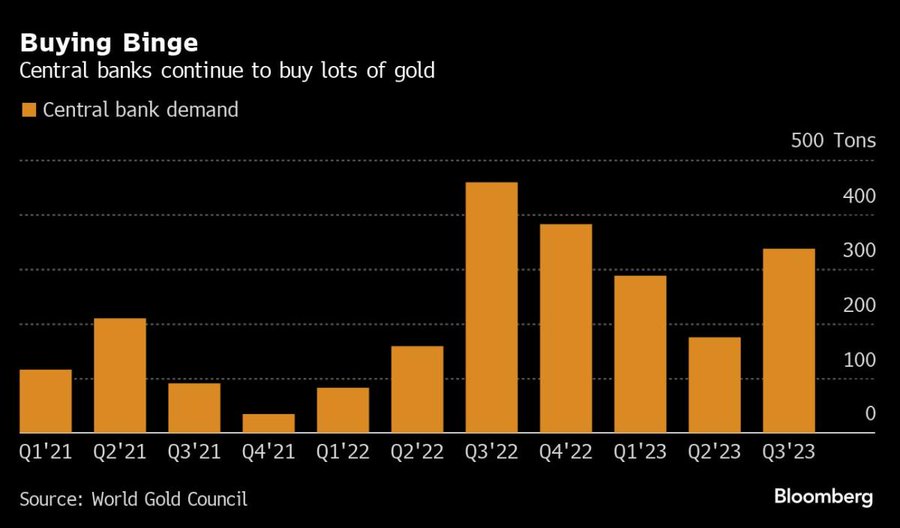

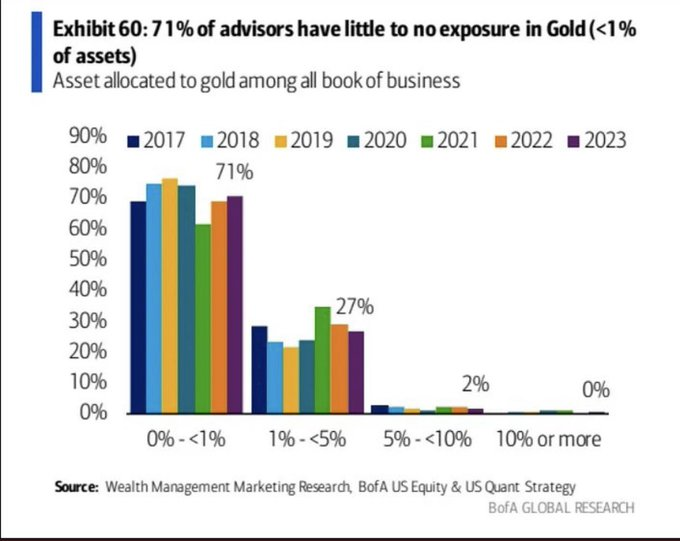

Gold ($1,993.30) got over $2,000 for the first time since July. Although it couldn’t stay there, the retreat has been small and slow – a good sign that a big upturn is imminent. The central bank gold-buying binge is even bigger than we previously thought.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Very few advisor-guided accounts hold gold, and those that do hold a minimal amount of it. This makes me think: 1) Advisors are missing out diversifying to an asset that can substantially benefit their standard 60/40 portfolios; and, 2) It’s possible we see a heck of a bid if even some of them realize that fact.

Click for larger graphic h/t @BobEUnlimited

Click for larger graphic h/t @BobEUnlimited

The fractal dimension shows the obvious consolidation you can see on the chart. Consolidations that last this long lead to BIG moves.

Miners & Related

Coeur Mining (CDE – $2.41) reports next Wednesday after the close, with a conference call Thursday morning. The consensus is looking for $257.4 million in revenues and a penny loss per share, with December quarter guidance for $254.5 million in sales and a one-cent profit. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $4.45) reported a poor quarter, with revenues down 9.2$ from last year to $133.2 million (consensus $134.0 million) and a pro forma loss of four cents a share instead of the two-cent profit Wall Street expected. As I previously reported, they produced 6.3 million silver equivalent ounces, consisting of 2.5 million silver ounces and 46,720 gold ounces, comparable to the June quarter. They realized an average price of $22.41 per ounce during the quarter, a 14% increase compared to the third quarter of 2022. The earnings disappointment was due to the temporary suspension of operations at Jerritt Canyon in Nevada, slightly lower production at its San Dimas and La Encantada mines in Mexico, and higher costs.

The stock slumped to a seven-and-a-half year low after they cut the dividend. But First Majestic still is a leveraged way to play the higher precious metals prices ahead, so AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $4.56) reports Monday after the close, with a conference call Tuesday morning. Analysts want to see $41.4 million in revenues and two cents per share. For the December period, they expect guidance for another two cents a share. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sprott Inc. (SII – $29.94) reported September quarter revenues down 2.1% from last year to $30.1 million, a big miss from the $36.8 million consensus expectation. They earned 27¢ a share. Assets under management increased 8% from the end of 2022 and 1% from the end of June to $25.4 billion.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management pointed to their “energy transition” assets now accounting for about 25% of assets under management.

Click for larger graphic

Click for larger graphic

They are the world leader in uranium investing, which is going to be HUGE over the next 12 months.

Click for larger graphic

Click for larger graphic

Sprott is continuing to grow in a challenging investment environment. Assets under management, net income and adjusted base earnings before interest, taxes, depreciation & amortization (EBITDA) all were up in the September quarter. Their energy transition franchise is rapidly building scale. The clean-up of non-core businesses is largely complete with the divestitures of their Canadian broker-dealer in the June quarter and their Korean operations in the September quarter.

Management said they are seeing strong performance in key strategies early in the current quarter. I think the long-term trends support their positioning in precious metals and energy transition investments. Buy SII under $40 for a $70 target price.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $34,910.52) is holding up well. I think there is a sharp upmove ahead of us as spot bitcoin exchange-traded funds are approved by the SEC, and we probably will take advantage of that pop to exit. I’d like to hold on until the early 2024 halving, but much of the support for bitcoin comes from tether, which appears to be an out-and-out fraud.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $27.17) is the best way to play SEC approval of exchange-traded funds. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $82.48

Wednesday morning, oil perfectly erased all of the war-premium from Israel, even though that war is ongoing and may be expanding. But the Biden Administration told Reuters that they are contemplating releasing up to 180 million barrels of oil from the Strategic Petroleum Reserve, perhaps a million barrels a day over several months, in a bid to lower fuel prices and curb inflation.

If the White House follows through with this plan, it would be the largest release from the Strategic Petroleum Reserve in its nearly 50-year history and mark the third time in the past six months that the government has tapped into its emergency supplies. 180 million barrels of oil is equivalent to approximately two days of global demand. It’s a terrible, even dangerous, idea and Chairman Xi must be laughing.

The Energy Administration Administration revised up (quite a lot) its estimate for American road fuel demand in August, based on monthly data versus the previously-used weekly data. It now pegs gasoline consumption at 9.30 million barrels a day, up from 9.06 million barrels a day. They did the same for diesel, 4.13 million barrels a day versus 3.76 million barrels a day.

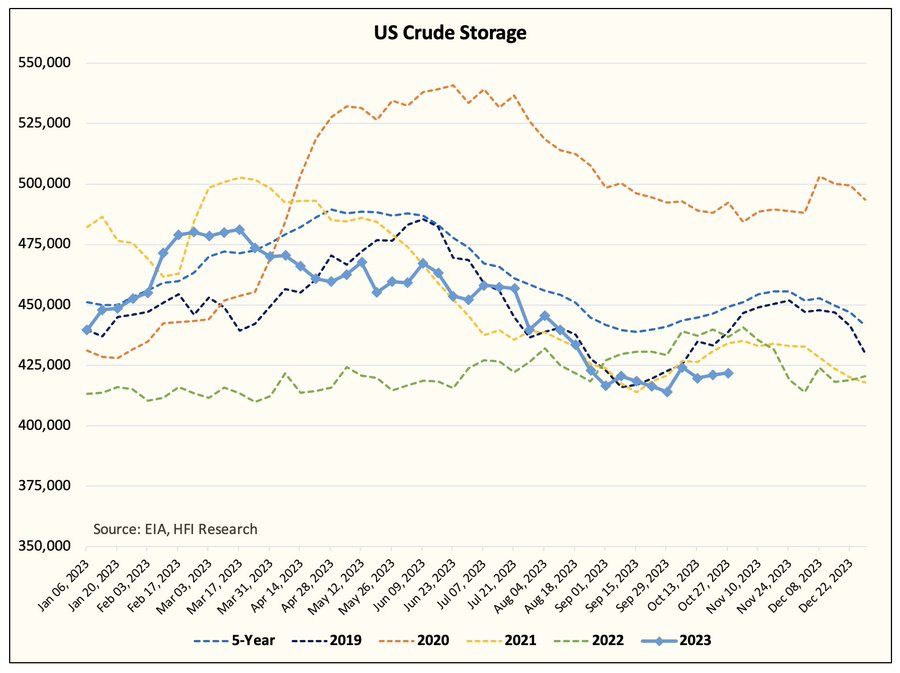

At the same time. US commercial crude storage isn’t building the way it should during refinery maintenance season. I think US commercial crude storage could fall to ~405 million barrels by yearend.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

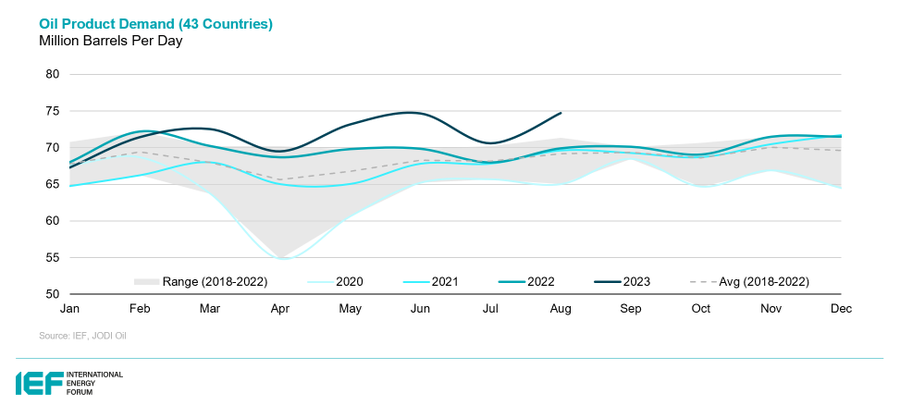

Global oil demand rebounded in August to record seasonal highs The month-over-month increase was driven by China, Indonesia, the US, and Saudi Arabia.

Click for larger graphic h/t @JODI_Data

Click for larger graphic h/t @JODI_Data

For the oil market today, we’ve come to a stalemate. With the Saudi/Russian voluntary production cut, crude is being squeezed higher, while product prices have come under pressure. This has resulted in downward pressure on refining margins. With the refinery maintenance season coming to an end and margins failing to gain any reactions despite a $10+ drop in crude, we are going to see some refinery run cuts into year-end.

The July 2026 Crude Oil Futures (CLN26.NYM – $69.71) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.96) is a Buy under $40 for a $100+ target.

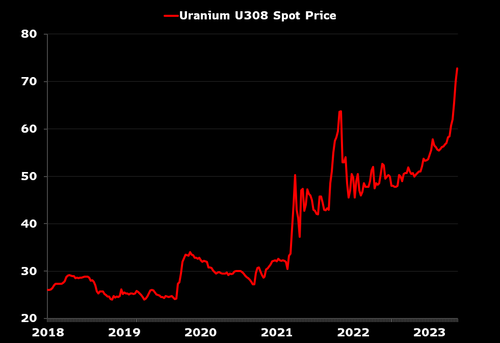

Energy Fuels (UUUU – $8.16) got a nice write-up on Seeking Alpha: Energy Fuels: Not Far From Becoming A Force To Be Reckoned With.

Click for larger graphic

Click for larger graphic

According to Zerohedge, several hedge fund managers are expanding their allocations to uranium stocks, with a conviction that an increasing embrace of nuclear energy as part of a “green” future – along with geopolitically-rooted ambitions to reduce dependence on Russian oil and gas – means the trend has a lot of room to run. The International Energy Agency says that, in order to meet “net zero” goals, global nuclear generation capacity must double from 2020 levels by 2050. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

International & Other Recommendations

It is important to hold some non-US assets, especially in China. Chinese stocks just saw net selling by foreign investors for a third consecutive month, the longest in history.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

As always, if the consensus zigs, you should zag. EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $28.72) is a Buy under $38 for a $66 target in 12 to 18 months.

KraneShares Bosera MSCI China A Share Fund (KBA – $21.57) is a Buy under $40 for a three- to five-year hold.

Morgan Stanley China A-Share Closed-End Fund (CAF – $11.92) is a Buy under $18 for a three- to five-year hold.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $26.28) is a Buy under $40 for a double over the next three years.

Primary Risk of all four of these: China falls into a recession.

Acreage Holdings (ACRDF – $0.36) introduced its Superflux craft cannabis brand in New Jersey. To show you how nutty this business is getting, it includes four limited-edition, small-batch flower strains crafted with bespoke genetics, including:

Cherry Lemon Gusher – A hybrid strain bred and selected to bring together a special cherry-scented Lemon Cherry Gelato, Lemonade Gushers, and Purple Zkittlez, delivering a soft, floral, citrus-berry aroma, and harmonious blending of sweet, floral, and red fruit flavors, like a raspberry mimosa.

Chocolate Cherry OG – A rich, indica-dominant strain, melding some of the most sought-after OG Kush plants with both Black Cherry and Lemon Cherry Gelato, offering a chocolatey rich, grainy sweetness with a creamy gas aroma and hints of fruit.

Red Carpet Runtz – A unique-scented and potent varietal, this indica-dominant strain blends Gelato, Cookies, Afghani, and a sprinkle of OG, giving a savory herbal top note with an underlying sweet gas aroma.

Silly Rabbit – Unleashing a complex sweet-meets-gas aroma with distinct notes of sweet cereal milk and light fruity qualities, this indica-dominant strain blends the “Guava” cut of Stardawg, Gelato, Zkittles, and Wedding Cake for some serious genetic pedigree.

ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

Click for larger graphic

* * * * *

* * * * *

Your thinking the Russia/Ukraine war is about over Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 11/2/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $177.57) – Buy under $150 for new iPhones

Corning (GLW – $27.38) – Buy under $33, target price $60

Gilead Sciences (GILD – $81.23) – Buy under $80, target price $120

Meta (META – $310.87) – Buy under $150, target price $400

SoftBank (SFTBY – $21.07) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $10.23) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $45.04) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.47) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $20.47) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.25) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.59) – Buy under $13, target price $30+

Velo3D (VLD – $1.31) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $0.88) – Buy under $2, target $20

Aptose Biosciences (APTO – $2.93) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $5.95) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.39) – Buy under $7, hold a long time

Invitae (NVTA – $0.63) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.16) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.80 – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $10.41) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($22.86) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.52) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.02) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.52) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $23.94) – Buy under $30, target price $50

Coeur Mining (CDE – $2.41) – Buy under $5, target price $20

First Majestic Mining (AG – $4.45) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.30) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.56) – Buy under $10, target price $25

Sprott Inc. (SII – $29.94) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $34.910.52) – Buy

Grayscale Bitcoin Trust (GBTC – $27.17) – Buy

Ethereum (ETH-USD – $1,794.76) – Buy

Grayscale Ethereum Trust (ETHE – $14.00) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $69.71) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.96) – Buy under $40; $100+ target

EQT (EQT – $44.35) – Buy under $35; $70 first target

Energy Fuels (UUUU – $8.13) – Buy under $8; $30 target

Freeport McMoRan (FCX – $35.01) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $28.72) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.57) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $11.92) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.28) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.36) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.01) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $0.96) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Hallelujah for Judith Curry for debunking the climate warming fear mongering. The latest insanity is the politics involving waste from animals like milk cows. Ireland is now a target to slaughter 600,000 dairy cows because of the co they release when they poop. And they are calling for countries to return their land to its natural state. (Some 30 percent of their land mass. Which is not a problem for the US because we have lots of land. But for countries in Europe, it’s going to be a huge problem. There is a climate scientist in my local area who has been doing climate work for 35 years who has echoed Judith’s words several times on a local radio show. So thank you, Judith Curry. We applaud you and appreciate your words of wisdom.

That is only sort of true. I worked in dairy software and after 5 lactations, the animal is killed for food. This has nothing to do with carbon emissions. It’s business.

Big oil has obviously got into this Curry chicks pockets. Looking forward to Florida being 7 feet underwater LOL.

Florida is just a glorified swamp to begin with. I can’t understand why anyone would move there or build there when the sea level and land mass are basically equal. If they ever have an earthquake off the coast of any magnitude, Miami and other cities there will join other civilizations under water. (Remember the tsunami that hit Japan not so long ago?) But , amazingly , the people in Florida keep saying it’s NOT going to happen here!!

Maybe for the same reason Bill Gates bought a beachfront mansion. Rising sea levels might be BS.

PS – My oldest daughter lives in Florida and loves it. Been trying to get me to move there for 20 years.

Bill Gates can toss that mansion and not give a f. Do you believe in actuarial tables? More than a dozen property insurance companies have left Florida and getting waterfront insurance is practically impossible.

Why do you think that might be? Maybe they just don’t like Florida?

Just some really basic research will show you that coastal areas of Florida, particularly Miami are having real problems.

Let me help your research. Google “is Miami having water issues?” That should get you started.

You are smart not to do. My sister used to live there as well. I have been there many times myself. Still am not impressed. Every time I get on a plane and leave there I feel safer. And that’s saying something sense I am 30000 feet above there flying at 500 mph!! Just those hurricanes is enough for any sane person to say no thank you. Let alone the possibility of a tsunami happening from an earthquake somewhere off the coast. I guess if you stick your head in the sand you can just ignore all of that.

Who is Judith Curry ?

Watch the YouTube linked at the bottom of this issue.

I’ve been reading about the exothermic cause theory of climate change. Some scientists believe that increases in the earth’s temperature precede increases in CO2 levels, opposite the current belief. The normal long-term fluctuations in the earth’s core as it enters a period when it is nearer the surface heat the deep ocean (which is heating but can’t possibly be by surface temperatures). Interesting stuff!

PS – The oil companies pay me nothing.

Please stick to things that you know, like picking bio stocks … oh wait.

And not learn about new things like exothermic climate change?

How is this even a debate anymore? Did Trump win the election in your mind?

MM–on TGTX, your typo. Briumvi Q3 sales were $25.1 MM, not your $23.1 MM. This was better than expected, so the stock bolted up. Please address my general question on the last board about the best way to value current share price. What price/sales multiple is appropriate for a growing company like TGTX? For target price, do you use current sales or projected peak sales? I know that your target prices are based on your estimate of market potential, but actual sales are a harder number. Thanks.

Typo fixed, thanks. I look at the same thing an acquirer would look at: what are the potential peak sales for the drug, how long will it take to get there, what’s that worth today?

Thanks. I listened to the Nov 1 conference call reporting better than expected sales. At the end, an analyst asked about oral BTK inhibitors. Mike Weiss said that TGTX is perhaps developing a BTK inhibitor, which is considered appropriate for MS at certain stages, a different patient class than for anti CD such as Briumvi or Ocrevus. To me, this is arbitrary. Neither anti CD nor anti BTK drugs address root causes, and are merely great bandaids. Regardless of that, Weiss seemed evasive and uncomfortable, and this analyst suggested that anti BTK drugs are the main risk for Briumvi. They speculated that perhaps one day, oral anti BTK drugs may take away use of anti CD drugs like Briumvi. Earlier in the Q&A, Weiss and Waldman, the marketing chief said that some patients on therapies other than anti CD are switching to Briumvi, a positive. Many TGTX bulls say that Briumvi is THE best drug for MS, but we should research anti BTK and perhaps other classes of drugs which are competition. What do you know at this point?

If all this is true, Weiss may be seeking an exit strategy by selling the company before anti BTK or other drug classes claim preferred status.

DonB–I gave you further info at the end of the last board. In addition, make sure your weight is slender. Body mass index (BMI) is not accurate, but get a body fat scale for $30 to measure your body fat (BF) percentage. Optimum BF is 15% for a nonathletic male. Mine is 15-16%, at 6 feet, 165 pounds in clothes and shoes before lunch. Covid mortality is almost zero for slender people and Vit D levels 50-80. Add the use of liposomal GSH and Vit C if you get ill, and you can sleep well at night without any vexes, even at your advanced age.

MM,

Did you just change the buy price for Meta in the Recommendations Section ( Meta (META – $310.87) – Buy under $250, target price $400) or is that a typo?

A mysterious typo. Fixed to $150, thanjs.

Chris–a few people here are invested in ACXP. 96% short term cure rate with their drug candidate is great. Vanco had 100% cure. Both drugs were studied in only a few patients for this 2B trial. I would say an insignificant difference. More telling will be the extended time to assess recurrence. When do you expect that info? It is very likely that Vanco will have greater recurrence and be inferior. Phase 3 may have to be done solely by ACXP. Is the cash of $9 MM enough to get through phase 3? More worrisome, enrollment in phases 2A and 2B was very slow, and phase 3 may take many years, or like Algernon, the company may fold. These are the stock risks. I kicked myself recently for missing the low of $1.20 because of these risks, although you had the good sense of buying more around then. I may get another chance to buy more at that low price. What do you think?

ACXP holds their quarterly conference call on the 14th and your questions are likely to be addressed during the Q&A.

Regarding Phase 3 funding, in previous presentations & in their Q2 call they had indicated that they would pursue an M&A initiative after receiving Phase 2 data and on a parallel track with preparing for Phase 3. If they weren’t satisfied with the responses they indicated that they had the money to get to the first interim review of the Phase 3 data and would again pursue an M&A initiative at that time. I’m sure funding will once again come up in this quarters Q&A.

Of course Vancomycin, with an 81% historical cure rate, comes in at 100% for this trial. Unfortunate proof of what can happen with very small sample sizes. I’ll be curious to see if ACXP has been able to learn anything yet regarding the one patient that wasn’t cured. Regardless, ACXP has several compelling advantage over Vancomycin even if the cure rate doesn’t end up being that much different.

We need to see how the ACXP and Vanco patients do with much longer observation to judge recurrence rate. Because of the healthier microbiome for ACXP, we predict that Vanco will have a higher recurrence rate. Personally, I’d like to see a moderate number of patients for another comparator between ACXP and Vanco, with a long enough observation period, rather than a large number of patients with a shorter observation period. With the latter design, that phase 3 has a higher chance of failure, than with the former design. It seems that recruitment is very slow, so the former design could get done with less funding, and it would be more meaningful for AXCP shareholders and a potential acquirer.

Chris?

There’s a new Seeking Alpha article on ACXP out today.

https://seekingalpha.com/article/4647935-acurx-undervalued-set-for-potential-mna-with-next-gen-c-diff-treatment

MM – I’m baffled by your bitcoin comments about exiting on next “pop” which seems to be a reversal of your long term support and projection its heading to $100k and as most advocates think, much past that post 2024 halving. I get you think taking profits along the way is prudent but why would you “exit” bitcoin before the bigger long term rise happens?

As you know, bitcoin is volatile. Tether is a fraud that has been used to run bitcoin pump and dumps. The imminent transition to real buyers could put it at $65K+, and if the SEC is going to kill Tether, as seems likely to me, that pop would be a good time to step aside with at least part of your position.

But do you still believe bitcoin is headed to $100k and when?

How do you buy shares in MDNA now?

MDNAF

Won’t all the massive federal infrastructure, etc., dollars start to be spent, possibly preventing a recession?

Probably not soon enough or big enough to prevent it, but that’s one reason I say “shallow.”

Conventional socialist economics holds that spending money yields economic growth. But that reduces the money available for other things. This is the famous fallacy of “the broken window.” Criminals break the window, and the dumb masses cheer it because the owner of the building with the broken window has to spend money to repair it. This benefits the construction crew and glass maker, but the money for that is not available for other spending, so the people not involved in the glass business suffer. Yet in socialism, money printing lets everyone claim their “fair share” (puke horrors) with severe longterm inflation that screws everyone ultimately.

If spending for project A is more productive than project B, then net growth would be A minus B. It is debatable whether federal infrastructure spending (A) is more productive than private individual and corporate spending. I’m being too polite, because the most productive countries are those where private spending is much more dominant over govt spending. The reason is that individuals and businesses are more careful about their spending, since they go bankrupt for unwise spending, but govts just print more money to cover up for their politically pressured stupid spending.

As a regular reader I’ve noticed that a frequent poster and fellow Rhode Islander, Donald Galamaga, hadn’t posted in quite a while. I always found his postings to be interesting and informative so I did a little research and sadly Donald passed away last October.I didn’t know Donald but I wish I did. He was an interesting and accomplished man. I’ve included a link to his obituary. I think he will be missed on this board.

https://www.providencejournal.com/obituaries/ppvp0336723

Tom, thank you for informing us, Dons intelligence, insights and his constant respectfulness of others opinions will be missed, he was a true gentlemen.

Mr. Dempsey: thank you for that info on “Captain” Galamaga. I too, enjoyed his perspectives.

Me too.

Sorry but that guy was a wack job. He was claiming that Sydney Powell was going to unleash the kracken after the 2020 election. Probably a nice guy but completely off the rails.

WRONG. Donald was a great gentleman who analyzed both sides of many issues in a respectful and honest way. He understood sound economics and knew humanity in ways that nearly completely elude you.

A post on the previous board presenting facts from insightful doctors along with your deprecating response shows who the real wack job is.

traveltube

Reply to Michael

October 30, 2023 7:42 am

I guess some people can only see one side of a discussion? And speaking of schools: Johns Hopkins, Harvard, Stanford, Oxford, Yale…guess you know more than these folks? Genius!

Keep the blinders on and ignore epidemiologists who are calling for the immediate discontinuation of the mRNA products. You know, hacks like these guys who know far less than you or the Ethiopian non doctor who heads the WHO.

Stanford’s Jay Bhattacharya

https://profiles.stanford.edu/jay-bhattacharya;jsessionid=66377F5BEB7486AB995EF1E5807E45B1.cap-su-capappprd99

Yale’s Harvey Risch

https://ysph.yale.edu/profile/harvey-risch/

https://www.hopkinsmedicine.org/profiles/details/martin-makary

Plus:

Harvard’s Martin Kulldorff, PhD Biostatistician. He is a member of the FDA’s Drug Safety and Risk Management Advisory Committee and a former member of the Vaccine Safety Subgroup of the Advisory Committee on Immunization Practices at the CDC.

OR: Oxford’s professor of epidemiology Sunetra Gupta

Stanford. Yale. John’s Hopkins. Harvard. Oxford.

And you think it actually works, after all of the propaganda that turned out to be complete lies???

Get vaccinated and you won’t get sick. Get vaccinated and you won’t transmit it.

Since that was bullshit and had no basis in fact, it became get vaccinated to avoid hospitalization and death for a disease with an IFR of the annual flu…something that can’t be proven one way or the other, but keep on pushing it…

Says the guy who loves the country that silences speech and forces medical procedures on healthy people, if they want to live their lives, keep their jobs, travel on public transportation, etc…

Forced ‘vaccination’ of a product that doesn’t keep you from getting sick or spreading it should get sick…again, Fucking Genius!

-1

Reply

Michael

Reply to traveltube

October 31, 2023 5:13 pm

Wow. What an angry person. Calm down.

0

Reply

traveltube

Reply to Michael

November 3, 2023 2:43 pm

Typical liberal…lay out facts, get a stupid response. That’s it, in summary…I pray you get many more boosters on your health journey…you’ll be the 2% going forward…

0

Reply

This goofball dragged out a handful of randoms and used it as proof. Is that scientific? I could post 10s of thousands of research papers that show the vaccine was effective at REDUCING DEATHS. What a waste of time.

Then he/she points out that liberals respond to “facts” with stupid responses. Is that a rational opinion?

We are down to 2 or 3 people contributing to this board with the bandleader posting complete nonsense when he should be picking stocks that don’t go to 0.

I’m not going to debate stupid topics with stupid people. Let’s hear about good stock picks rather than rehash conspiracies.

Deal?

You better pay attention–these are NOT stupid topics, but you are stupid to be indoctrinated by mainstream media (MSM) which is censoring truth tellers. Millions of the masses who don’t know anything outside of what MSM pukes out are jungle dirt compared to words of wisdom and experience from a few who know what they are talking about. BTW, in a scientific clinical trial, treatment arms are matched as closely as possible for baseline characteristics. Your post matches millions of ignorant masses against a few learned experts such as cited by traveltube. NO CONTEST–your post is a model of bad science and idiocy.

The real conspirators are the censors in MSM.

Don Galamaga, Requiescat In Pace

Thanks for letting us know; I too had noticed his absence.

Heard it thru the grapevine. Two newsletter editors are now saying NVDA , Nvidia is going to crash. The reason, Elon Musk and others are designing a custom AI chip (for Tesla) and other interest. Net result, Tesla stock will shoot up. Also MDNA symbol has changed to MDNAF. Shot up the last few trading days.

Check your grapevine. NVDA is a trillion dollar company and is the leader in AI chips by a mile. It’s not going away.

The real winner in chips is ARM. NVDA just partnered with them and most others will follow, including TSLA.

NVDA is at 469.50. I will put it on my watchlist and check again at the end of this month and next. Also EV’s are still struggling. Ford is losing $36,000 on every EV it sells. Just sayin.

Wow, Judith Curry gives a diff. take on climate.

A take that isn’t followed by 99% of scientists but yes, it is a take.

Have you noticed that when science changes, it’s always less than 1% who lead the change?

No I haven’t but I’d love to see the data.

You don’t need data. All new ideas originate from a single person, not a consensus committee. Many new ideas don’t survive further investigation, and they are dropped. But the ideas that are true after further work are first ridiculed by the committees, then grudgingly accepted, then considered so obvious that how could anyone deny them. Elon Musk was considered crazy at first, now he is in high esteem.

Seek your medical care from the 99% of MD’s who are mere AI socialist robots who don’t grasp root causes of disease and offer only drugs, surgery, chemotherapy and radiation therapy. If you want the best medical care, you will pay cash out of your pocket to the 1% or fewer docs who don’t accept any insurance.

So let me get this straight. Are you proposing that we pay our whole lives into Medicare and then skip it and pay out of pocket?

Answer me two questions: 1. are you taking Medicare when you turn 65 2. are you taking social security.

If yes on both I don’t want to hear another word on your views on socialism.

What a confused post. Forcefully stealing money from your paycheck for medicare and SS forces you to try to collect your “benefits” in retirement. This behavior is what a rational child learns when a kid hits him and he hits back. Yes, I have MCR and collect SS. Neither are benefits, but are merely fighting back for what was stolen from me, and continues to be stolen since I still work. That is what socialism offers. And MCR and SS funds are politically siphoned off for programs I hate. Socialism pits people and its own programs against each other. You can take mediocre medical care that MCR pays for. But if you want better care that private pay offers, that is still an option. What I see in medical practice (and you don’t) is that most people have very little money for better medical care because their money has been depleted by expensive insurance premiums to pay for expensive drugs and other treatments that are just bandaids and offer poor value for quality of life benefits. The obese patient needs to follow a diet, rather than scheming to have the system waste money on cholesterol, diabetes, hypertension drugs. It is far more prudent to pay $1000 cash to a private MD who works to help him lose weight in several visits, rather than $1 million for many decades of drugs and procedures that MCR pays for. A person in a free market is offered a choice–spend a little money periodically and do the right thing, or pay incessant 100’s/1000’s of bucks every month for drugs, etc. The free market gives the motivation for nearly everyone with a brain to have individual responsibility or else face poverty. Donald Galamaga wrote extensively about all this, echoing my approach. And yet you foolishly deprecate him. SHAME ON YOU.

But the free society doesn’t steal your money, except for a small 10% to provide for things like police, fire, road repair that the free market has difficulty implementing. The individual must have responsibility for his own life, but he can invest his own money in whatever HE wants rather than what OTHERS force on him.

As an individual, you have the right to be as crazy as you want, as long as you don’t steal money from me or anyone who disagrees with you. But in socialism, you are barging into my home and imposing your politically supported preferences and mandates on me. As a mentally deranged socialist, this paragraph is poorly understood and defiantly rejected by you. You will continue to hear from me when you make thoughtless pro-socialist remarks, in self-defense against you and other socialists who are destroying this once free country.

Maybe some socialist official will say to you that he is protecting your welfare by letting you invest only in bank CD’s, and forbidding you from investing in bitcoin, biotechs, AI stocks, even blue chips. Maybe that’s what it will take for you to wise up and shun socialism.

Well said, thanks for the clarity on reality.

TLDR. So you participate in socialist programs while decrying socialism. Got it.

Who is confused here?

You either misunderstood my reasoned post, or you willfully deny it. Both possibilities are applicable to socialists.

This fact alone is a justification why a well functioning society needs freedom from coercion from private or govt idiots. In a free society, idiots are entitled to their opinions and actions. Since they don’t interfere with others’ lives, they can be respected from a distance for their alternative opinions. But in a socialized society, their actions directly interfere with others.

If you don’t understand my lengthy post above, just understand the preceding paragraph.

And she is right. And she has the guts and common sense to stand up to the throngs of people who have convinced the people in power that we are all going to die from the current global warming nightmare. What they fail to mention is we had similar weather related issues in the 30’s.(one of which is the dust bowl) And we had far less fossil fuel use then than we do now. How can they spin that? Other scientists are saying that the recent changes in the earth’s weather is simply caused by sun flares. Other scientists say that humans are only responsible for 25 percent of the CO produced in the world . The rest occurs naturally. If you gather up scientists who preach the climate change narrative and then gather up media groups who buy into it because bad news sells you can create a potential crisis. Which is what has been happening now for some time.

I knock MM’s picks but it looks like GBTC is solid. I prefer to own BTC in cold storage but for those that can’t or don’t want to, GBTC looks good.

Michael, why is suddenly GBTC more attractive to you, youve spent months calling it a huge risk?? Also interested in your projections for bitcoin, how high and when?

GBTC was selling at a significant discount to BTC. This has shrunk to around 14 percent. I’ve done very well with BTC, no idea where the it’s headed but it’s NOT A BUBBLE. It’s a real asset. Could it be a million? For sure.

NVTA

OK LEMMINGS , get out. Get out while you still can.No significant sales growth for several quarters. Don’t follow another loser over the cliff.One for ten consolidation coming. Got rid of ever last share months ago when it went sub $1 and so glad I did. This will be worthless by the spring. Ironic as this is the bowing season.

Zman – get out of what???

NVTA and CWBR are the only MM picks sitting in my portfolio. Both essentially worthless.

But I have to say .. my absolute worst pick was my own. APPW AppHarvest. I figured that large scale greenhouses that could operate with no pesticides and way less water year round would be a winner. Well maybe, someday 🙂

SA on ENVX:

https://seekingalpha.com/article/4649763-enovix-breakthroughs-in-silicon-anode-battery-technology?mailingid=33313081&messageid=2800&serial=33313081.809&utm_campaign=rta-stock-article&utm_medium=email&utm_source=seeking_alpha&utm_term=33313081.809

Didn’t do it any good. Down nearly 9%.

Hey mm,we know your busy with all the earnings reports out this week,we’ll is there any way you could chime in about the earning call on nvta before tonight since it’s trading at 45 cents com on man,give us your thought would you

NVTA- Tragic, sort of another ARTH…

It may end up as the AMZN of genetic testing but owned by somebody else that bot it out of bankruptcy.

New World Investor for 11.9.23 is posted.