Dear New World Investor:

As I expected, Nvidia (NVDA) reported a strong January quarter after the close yesterday and guided the April quarter above estimates. The stock was up $110.66 or 16.4% today to new record highs as Wall Street fell all over themselves to raise their ratings and target prices. Nvidia is a great company that I first recommended in 2000 in the California Technology Stock Letter and still recommend in Boomberg. CEO Jensen Huang told me in 2000 that Nvidia would be a bigger company than Intel (another Boomberg recommendation) and he was right.

It’s a bad idea to bet against Jensen.

Click for larger graphic

But. Carefully listening to the conference call (AUDIO HERE) and reading the transcript (TRANSCRIPT HERE) tells me that Nvidia is successfully accelerating contracted production of their AI processors, so supply is going to catch up with demand. That means the quarterly revenue beats and estimate raises are coming to an end. And that means Wall Street is setting up one of their classic rug pulls.

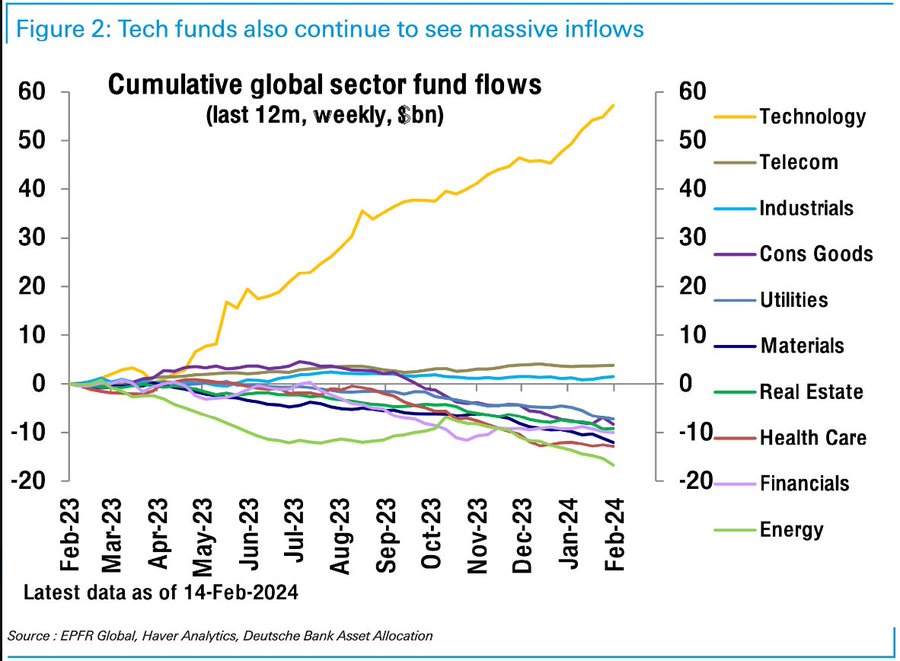

There’s been a real pile-on in tech over the last year:

Click for larger graphic

Click for larger graphic

And sentiment has moved from Greed to Extreme Greed:

Click for larger graphic h/t CNN

Click for larger graphic h/t CNN

The rug pull will not necessarily be on Nvidia, which is genuinely a great company that all the investment pros have to own. But Nvidia’s beat and raise drove the S&P 500 up 2.1% today to a record close, even though most of the S&P companies don’t make AI chips or software, and in many cases are more threatened than benefited by the AI revolution.

Given that, and given that I’ve held two very different outlooks from Wall Street for quite a while, namely High – but not higher – for Longer on the Fed funds rate and that there will be a recession this year, I think it’s time to buy some portfolio protection. I’ve been thinking about this for a while but the fractal dimension is screaming that a correction is imminent (see below), so now is the time.

First, some caveats. Portfolio protection is insurance, and the cost of it is the insurance premium. Just like you don’t want your house to burn down so you can collect on your fire insurance, or your car to be wrecked, you don’t want to make money on portfolio insurance. It’s there to let you stay invested in this secular bull market that won’t hit a major top until 2036.

Second, you do not want to make a huge bet on a down market. This is not a speculation. Consider the cost of portfolio insurance as an expense – gone money you never will see again.

Third, there are many ways to protect a portfolio – index puts, VIX puts, reverse funds, and so on. There’s no “right” way and some of you might want to try a mix of things. Because puts on the SPDR S&P 500 ETF Trust (SPY) are historically cheap, I’m going to recommend two of them,

Buy the April 30 SPY $505 put (SPY240430P00505000)

Buy the April 30 SPY $410 put (SPY240430P00410000)

The April $505 put fell 46% today to close at $8.21, so each contract for 100 positions will cost you $821. We’ll be selling these puts around mid-March, possibly to roll them out to a later expiration date by buying June or July put contracts. At today’s close, these had 1,362 existing contracts (open interest), so they are fairly liquid. The sharks at the Chicago Board Options Exchange will low bid an illiquid option when you try to sell it near expiration.

The April $410 put fell 24% today to close at 56¢, so each contract for 100 positions will cost you $56. These contracts have a much higher risk of a total loss. We’ll also be selling these puts or rolling them out around mid-March to avoid the rapid decline of the time premium after that. At the close, these had 1,803 open interest, so they also are fairly liquid.

If all that was just bafflegab to you (or you hate/can’t buy options) the best portfolio protection is to raise a little cash to be ready to buy bargains when (and if) we get the market correction I’m expecting. You also could buy any reverse index fund like the ProShares Short S&P 500 ETF (SH). It’s the most popular inverse ETF, with an expense ratio of 0.89%. ProShares also has a 2x fund that doubles the daily gain or loss, the ProShares UltraShort S&P 500 ETF (SDS), and a 3x fund, the ProShares UltraPro Short S&P 500 ETF (SPXU), with about the same expense ratio.

Or instead of betting on an Index decline you could just bet on increasing volatility with the ProShares Ultra VIX Short-Term Futures ETF (UVXY), which goes up as volatility increases. For you daredevils, the UVXY April 19 $7 put (UVXY240419P00007000) that closed up 10% today to 85¢ should provide plenty of thrills until the summer roller coaster season opens up.

Recession Watch

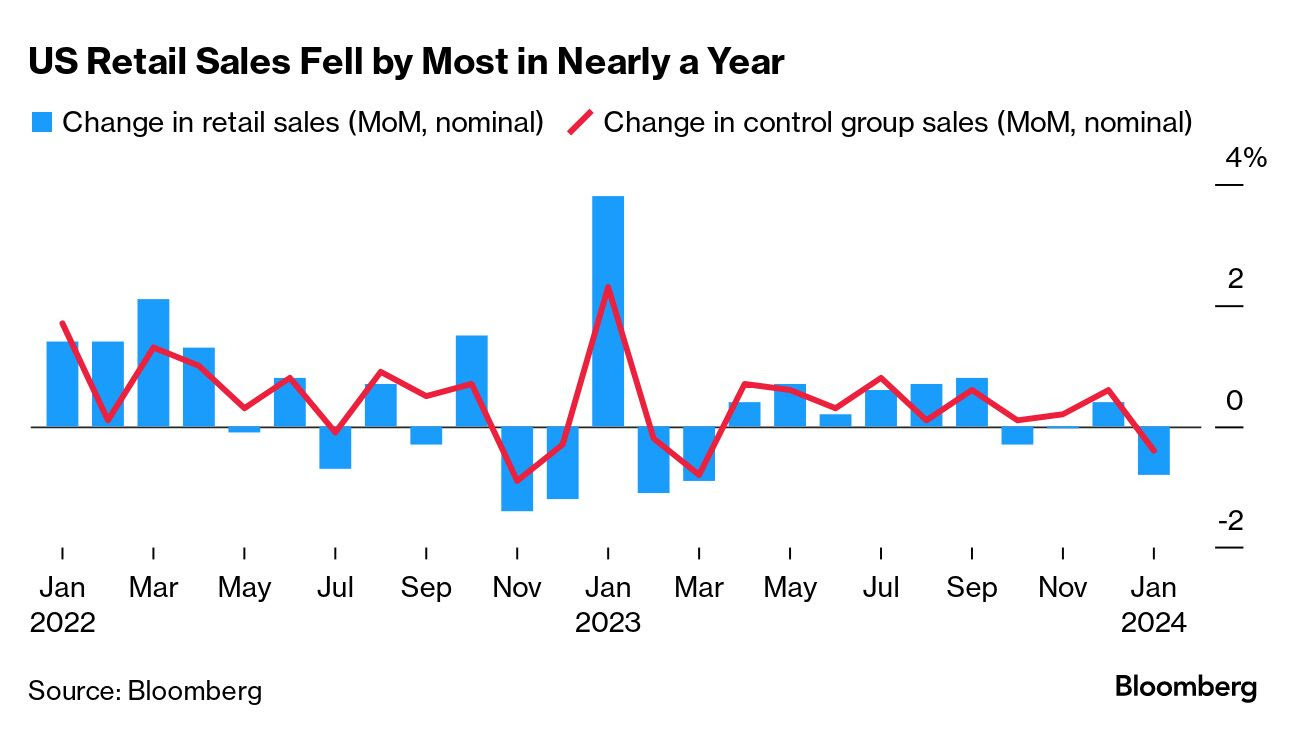

Retail sales plunged by 0.8% month-over-month in January versus the -0.1% estimate, the sharpest drop since March 2023. Control-group sales (used to calculate GDP) fell 0.4%, the first decline in 11 months.

Click for larger graphic h/t Daily Chartbook

Click for larger graphic h/t Daily Chartbook

Market Outlook

The S&P 500 added 1.1% since last Thursday to new record highs today. The Index is up/down 6.7% year-to-date. The Nasdaq Composite gained 0.9% after today’s3.0% jump, its best day in more than a year and pressing near a record-high for the first time since November 2021. It is up 6.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 0.9% and is up 5.4% year-to-date. The small-cap Russell 2000 dropped 2.3% and is back in negative territory for the year, down 0.7%. Even the venerable Dow Jones Industrial Average banked a 457-point gain today. It was a global party: Japan’s Nikkei 225 index finally beat a record that had stood since 1989 and the pan-European Stoxx 600 hit a fresh all-time intraday high.

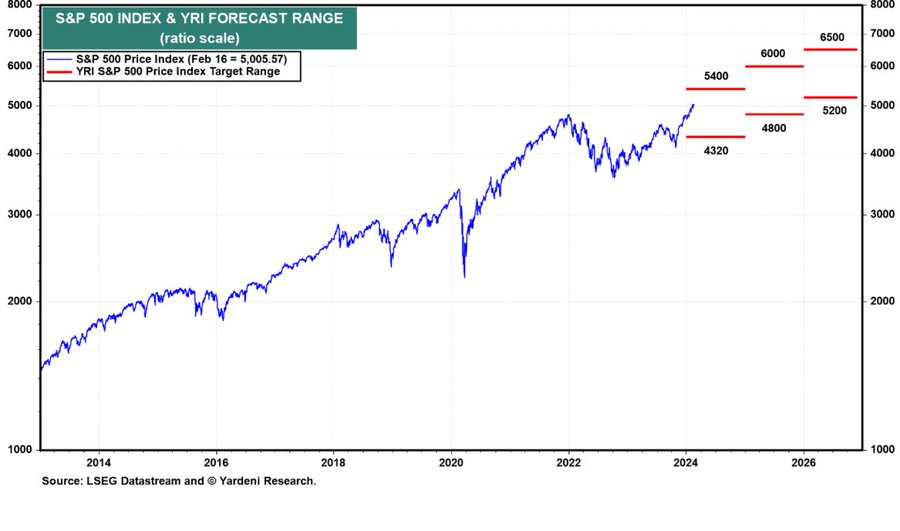

The excellent Ed Yardeni reiterated his forecast for the S&P 500 Index of 5400 at year-end 2024, 6000 in 2025, and initiated 6500 in 2026.

Click for larger graphic h/t @yardeni

Click for larger graphic h/t @yardeni

The fractal dimension is ridiculously low, meaning a consolidation – sideways for weeks or a serious drop – is overdue.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, February 26

AG – First Majestic – Through 2/28 – BMO Capital Markets Global Metals, Mining & Critical Minerals Conference

AG – First Majestic – Through 2/29 – Investment U 2024

Tuesday, February 27

Short Interest – After the close

RKLB – Rocket Labs – 5:00pm – Earnings conference call

QUIK – QuickLogic – 5:30pm – Earnings conference call

Wednesday, February 28

December Quarter GDP – 8:30am – Second estimate

AAPL – Apple – 12:00pm – Annual meeting

Thursday, February 29

PCE – Personal Consumer Expenditures Index – 8:30am

TGTX – TG Therapeutics – 6:00pm – Poster presentation sat Americas Committee for Treatment and Research in Multiple Sclerosis (ACTRIMS) annual forum

Friday, March 1

GLW – Corning – 1on1s – Susquehanna Technology Conference

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $184.37) put 12 games on Apple Arcade designed for spatial computing with Apple Vision Pro. Players are able to tee up the perfect shot as they move freely around a quirky golf course right in their home in WHAT THE GOLF?, slice apples with their hands as their living room transforms into their very own dojo in Super Fruit Ninja, and escape into a mesmerizing audiovisual experience in Synth Riders or LEGO Builder’s Journey.

They also introduced Apple Sports, a free app for sports fans that delivers fast access, real-time scores and stats. It puts users’ favorite leagues and teams front and center. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

SoftBank (SFTBY – $29.33) rose as CEO Masayoshi Son considers the creation of a $100 billion chip start-up that would supply AI-enabling semiconductors. Open AI CEO Sam Altman also is talking to big investors like the Saudis about a $100 billion startup. Guys, the total market value of Intel is just north of $180 billion and they actually know how to make semiconductors.

A software CEO like Altman thinking he can do a semiconductor startup and make any money is just funny. Masa could do it, but why? The stock is on its way to my $50 first target, but if Masa really does this we may have to bail. For now, SFTBY remains a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $9.72) announced a very good December quarter. Revenue was up a nice 572.7% to $7.4 million, more than double the $3.42 million estimate. They had a GAAP loss of 28¢ a share, smaller than the 36¢ loss expected.

The revenue strength was driven by strong performance from Routejade plus continued volume shipments of BrakeFlow-enabled batteries to the US Army. On the conference call (LIVESTREAM HERE and LETTER TO SHAREHOLDERS HERE and SLIDES HERE and TRANSCRIPT HERE), management said accelerated depreciation associated with the strategic realignment of Fab1 increased cost of revenue by $6.2 million and operating expenses by $12.3 million – these also will knock 10¢ a share off March quarter earnings, but they are are not recurring expenses.

For the March quarter, they guided for revenue between $3.5 million and $4.5 million, and a pro forma loss of 29¢ to 35¢, including the 10¢ impact.

CEO Raj Talluri said: “…we have laid the groundwork on how to scale up in 2024…we are in the process of completing our factory acceptance testing, and a good amount of our Gen2 equipment is now in Fab-2 in Malaysia, ready to produce the first batteries in April.”

COO Ajay Marathe gave a brief Fab2 update from Malaysia:

Click for larger graphic

Click for larger graphic

During the quarter, two of the top smartphone OEMs in China entered discussions on how to collaborate on making batteries for their phones. In the June quarter, Enovix will sample a 1,000-cycles smartphone-class battery. The smartphone industry needs a higher energy density battery as soon as possible to cope with a tidal wave of power-hungry AI-based applications. Capturing video with AI features enabled on two leading flagship smartphones consumes over 50% more battery life than without AI. Running chatbots like ChatGPT3 and Llama 2 uses 2x to 11x more battery life than watching videos on YouTube. Today’s standard of all-day battery life on the smartphone is not sustainable without a battery breakthrough like Enovix. They already are engaged with Vivo, Xiaomi, Lenovo, and others (probably Apple).

Click for larger graphic

Click for larger graphic

They also entered into a development agreement with a leading automaker to validate the advantages of the Enovix cell architecture for an EV battery. I expect them to either license the technology or manage the production process, with the automaker funding the equipment. The EV battery market is expected to exceed $500 billion by 2040.

Click for larger graphic

Click for larger graphic

They used $27.2 million in cash during the quarter for operations and another $28.8 million for capital spending, and ended with $306.8 million. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

QuickLogic (QUIK – $12.92) reports earnings next Tuesday after the close. Wall Street (two publishing analysts) expects revenues up 81.2% to $7.4 million with pro forma earnings of 13¢ per share. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $4.44) also reports earnings next Tuesday after the close. The consensus is for revenues up 21.5% from last year to $62.89 million and a loss of 10¢ a share.

They successfully launched the ADRAS-J satellite and after March 9 will launch their 45th Electron mission for Synspective, a Japanese Earth-imaging satellite constellation operator. This is their fourth launch for Synspective. Shortly after that they’ll launch a dedicated mission for the National Reconnaissance Office from Launch Complex 2 in Wallops, Virginia. The National Reconnaissance Office is the US government agency that designs, develops, acquires, launches, operates, and sustains our intelligence satellites. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $4.85) reported 2023 full-year revenues of $38.0 million, just under the $38.13 million estimate. The partnership business generated research fees of $35.6 million, compared to $40.8 million in 2022. Licensing revenue was $1.0 million. They lost 51¢ per share, a bit more than the 47¢ loss estimate.

On the conference call (CALL SUMMARY HERE and SLIDES HERE and TRANSCRIPT HERE), management said R&D increased to $175.7 million in 2023, reflecting growth in program execution and investments in internal programs. The number of discovery partners increased from 40 to 46, while the number of programs under contract increased from 174 to 203. A total of 13 molecules have reached the clinic, up from 8 in 2022.

They are increasingly focused on strategic partnerships and have deals with Lilly, AbbVie, Regeneron, Novartis, Incyte, and many others.

Click for larger graphic

Click for larger graphic

CEO Carl Hansen said: “As we enter 2024 and after nearly 12 years of investment, we are now in the final stages of building our engine with the remaining efforts concentrated on our manufacturing capabilities. Through this work, we have built a competitive advantage in the discovery and preclinical development of antibody therapies and we will soon be fully integrated from target through to the clinic.

“We have tested and proven our capabilities across more than 100 programs and we have done this in partnerships with the top tier of biotech and pharma companies. Through these partnerships, we have built a portfolio of passive royalty positions in therapeutic programs. We believe this portfolio represents a growing and unrecognized store of value that will mature into future high margin revenue streams.

“Over the past three years, we have increasingly focused on only those partnerships that we see as strategic and that we believe will yield the highest value. This has included the addition of multiple co-development programs in which we have the option to maintain a 50% ownership stake. Alongside of our partnership business, we have made internal R&D investments over the last five years to unlock difficult target classes including GPCRs and ion channels. This work is now bearing fruit. And last year, we announced our first internal program from this effort that has advanced into IND-enabling studies. We believe this is just the beginning and that it foreshadows a series of potential first-in-class therapies over the coming years.”

Click for larger graphic

They ended the year with $787.8 million in cash and still have another $220 million available from government programs. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Compass Pathways (CMPS – $10.01) is expected to rise 300% this year by Wall Street analysts. That could happen if Compass reports positive top-line data from their first Phase 3 trial this summer, as I expect, AND Lykos Therapeutics (private) gets FDA approval on their August 11 PDUFA date for their combination of MDMA (ecstasy) and psychological support to treat post-traumatic stress disorder (PTSD).

That would upending decades of prohibition and mark the start of a new age of treating mental illnesses. If the FDA is board with the general idea that it is possible for psychedelics to be safe and effective, changes at the Drug Enforcement Agency (DEA) are practically a given, rescheduling psychedelic molecules to be easier to use medicinally and provisioning for federal research dollars to go into psychedelics research. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Invitae (NVTAQ – $0.01) filed for Chapter 11 bankruptcy protection and added the dreaded “Q” to their stock symbol. I believe the current stockholders will own part of the company that emerges from bankruptcy, but we’ll see. The auction is April 17. Until then, Hold NVTAQ.

Primary Risk: Current shareholders don’t own any of the restructured company.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Mid-2024.

Inflation MegaShift

Gold ($2,034.40) recovered from a brief dip below $2,000 that probably cements that in as solid support. The fractal dimension consolidation continues.

Miners & Related

Coeur Mining (CDE – $2.66) reported December quarter revenues up 24.7% from last year to $262.1 million, beating the $257.27 million estimate. A pro forma loss of two cents a share fell short of expectations for breakeven. They produced 3.1 million ounces of silver and 101,609 ounces of gold in the quarter.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said the crucial Rochester Mine expansion ramp-up is advancing towards the expected completion by the end of June. The Wharf Mine delivered all-time record annual cash flow of $82 million, while the Silvertip Mine drilled one of its highest-grade intercepts ever.

They guided 2024 for production of 310,000 ounces to 355,000 ounces of gold and 10.7 million to 13.3 million ounces of silver. Management has done a great job of boosting mine production while expanding their resources. Now it’s up to precious metals prices to make this a home run. Coeur ended the quarter with $62 million in cash and $185 million of capacity on its revolving credit line. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $4.12) held their conference call last Friday. As I reported last week, they announced record 2023 results. December quarter revenues grew 15.7% from last year to $44.5 million. They earned eight cents a share, obliterating the one-cent consensus estimate. On the conference call (SLIDES HERE and TRANSCRIPT HERE), CEO Nolan Watson said: “I’d like to take the time to give an update of Sandstorm’s business and the things that I will specifically focus on which I believe are important to shareholders are five-fold.”

The first one was updated five-year term guidance, including the timing of two growth projects, Hod Maden and MARA. Their updated production expectations for the next 15 years show substantial growth. By the end of 2024, Equinox will have its Greenstone mine in production and Ivanhoe will have its Platreef mine up and running. Production will increase in future years from these high quality, long-life mines.

Click for larger graphic

Click for larger graphic

The second one was projected debt repayments in 2024. Bank debt will be under $350 million by the end of the year. They’ve already sold $17 million of the non-core assets.

Click for larger graphic

Click for larger graphic

The third one is their share buyback plans once debt is under $350 million. That is a level so comfortably low that they can begin dividing future cash flows between debt repayments and share repurchases.

The fourth one is what their production guidance means in terms of cash flow expectations at today’s gold price. As Greenstone, Platreef, Robertson, Turquoise Hill, Hod Maden, and MARA all start producing over time, their cash flow increases to over $200 million a year even if the price of metals is flat.

Click for larger graphic

Click for larger graphic

The fifth one was a summary of the five key catalysts that shareholders can look forward to:

Click for larger graphic

I recommended Sandstorm because it is an extremely well-run streaming company that will benefit strongly from increasing precious metals prices without significant mining risks. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sprott Inc. (SII – $37.00) reported December quarter revenue up 18.3% from last year to $36.67 million with GAAP earnings of 38¢ per share. On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said in 2023 they grew assets under management by $5.3 billion to $28.7 billion. They had seven new ETF launches in the US and Europe with two more pending and launched their actively-managed Physical Commodities strategy. Sprott is the world leader in uranium investing, now 30% of their assets under management, where I am very bullish:

Click for larger graphic

Click for larger graphic

They paid down $19.2 million of their outstanding debt in the quarter, bringing them to $30,2 million for the year. At the end of December they only had $24.2 million in debt remaining. They finished the year with $31.2 million in cash. Buy SII under $40 for a $70 target price.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

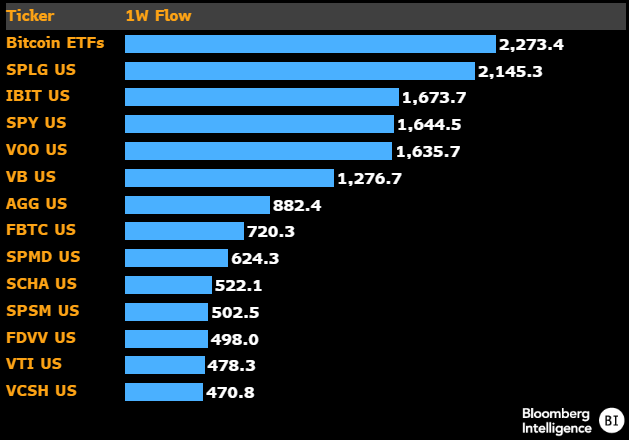

Bitcoin (BTC-USD on Yahoo – $51,619.38) traded over $51,500 this week, the highest level since 2021. The ten bitcoin ETFs netted $2.27 billion last week after the ongoing GBTC bleed.

Click for larger graphic h/t @EricBalchunas

Click for larger graphic h/t @EricBalchunas

Bitcoin rallies have averaged 32% in the eight weeks leading up to the reward halving, according to 10X Research. Bitcoin’s fourth halving is due on April 19 and a 32% gain would put it near its all-time high of $68,790. Also, bitcoin’s daily relative strength index (RSI) has crossed above 80 for the first time since December. 12 out of 14 such previous RSI signals presaged accelerated uptrends, producing an average gain of 54% in the following 60 days. Bitcoin traded at $48,294 when the last signal was triggered, and if it increases 54% it will rally to $74,600.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $29.72) had the second-largest inflows last week in the table above and now has more than $5 billion in assets, so probably will hike the management fee to 0.25% per year – still a good deal. IBIT is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $2,979.87) hit $3,000 for the first time since April 2022. It may be the only digital asset other than bitcoin to get spot ETF approval from the SEC, according to the Bernstein brokerage firm, and there’s a 50/50 chance it could happen by May. Franklin Templeton, BlackRock, Fidelity, Ark and 21Shares, Grayscale, VanEck, Invesco and Galaxy, all of which had bitcoin ETFs approved, are among firms that have already submitted applications for an ether ETF.

Dencun, the ethereum blockchain upgrade due in March, will slash transaction costs. I’ve developed a token on ethereum and also minted NFTs, and the transaction costs are ridiculous. At the same time, even though there is no hard cap on ether creation as there is on bitcoin, there has been a significant drop in ether supply since ethereum transitioned to a proof-of-stake consensus mechanism in September 2022. Since the transition, 1,047,643 ETH ($3.05 billion) have been issued and 1,407,200 ETH burned, or taken out of circulation, causing a net supply reduction of 359,557 ETH, according to data tracking website Ultrasound.money. I did not expect that. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

Grayscale Ethereum Trust (ETHE- $25.88) holds 0.00951747 ether per share worth $28.40, so the discount to net asset value still is 8.9%. It’s not a whole lot, but it is free money compared to buying ether directly. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $78.46

Oil rose after the Energy Information Administration reported a mildly bullish oil storage report today. Refinery throughput once again disappointed to the downside, coming in at 14.574 million barrels a day, equivalent to last week’s 80.6%. The Whiting refinery restart this week should result in a rebound next week.

Most of the recent crude build is the result of low refinery throughput, which means product storage is declining:

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

One of the key engines of the latest oil rally, refining margins, has pulled back. Until refining margins move higher again, crude may have peaked for now. Be patient – much higher prices are coming.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The July 2026 Crude Oil Futures (CLN26.NYM – $67.19) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.55) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.01) is a Buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

EQT (EQT – $37.32) benefited from higher natural gas prices after Chesapeake Energy (CHK) played the role of OPEC for natty. Chesapeake announced a major reduction in capex and production, 0.73 billion cubic feet per day (Bcf/d) in 2024 compared to the December 2023 quarter.

Click for larger graphic

Click for larger graphic

They were promptly followed by Antero Resources (AR) cutting by 0.1 Bcf/d and Comstock Resources (CRK) by 0.054 Bcf/d. EQT is increasing production by 0.03 Bcf/d. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $6.10) will be a big beneficiary of the surging price of uranium. In their earnings call, Sprott management said: “Recently the price of uranium has breached the $100 a pound threshold. This is a price we have not seen since 2007. Based on all the builds in progress and plans around the world, we anticipate that annual uranium demand will grow from £180 million per year to somewhere in the range of £250 million, most likely £300 million in the year 2040. Uncovered utility requirements range from £1.5 billion to £2.3 billion, which is quite staggering going out to 2040.

“We’ve also seen a number of supply challenges. With every commodity bull market, you would obviously assume a supply response. And what we have seen over the last six months is two of the world’s largest producers of uranium have both signaled some near-term and short-term production challenges, and we don’t expect any material new uranium mine to be built in the next four to six years. It’s fair to say that geopolitical risks related to uranium and the nuclear fuel cycle remained very high. There is a bill that will inevitably get passed in the US that will ban Russian uranium importation, which we think will potentially disrupt the market.”

At the COP28 climate summit at the end of last year, the United States and 21 other countries pledged to triple nuclear energy capacities by 2050. Uranium price surged 11% in January to $101 per pound, a 16-year high, fueled in part by Kazatomprom’s 14% cut in production guidance for 2024. Junior uranium miners were top performers for the month, climbing 18.78%. Supply uncertainties continue to dominate markets, given the situation in Niger and possible bans on Russian uranium. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

* * * * *

Your learning about RFK Jr. Editor, (movie is free during February)

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 2/22/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $184.37) – Buy under $150 for new iPhones

Corning (GLW – $32.69) – Buy under $33, target price $60

Gilead Sciences (GILD – $72.78) – Buy under $80, target price $120

Meta (META – $486.13) – Buy under $345, target price $400

SoftBank (SFTBY – $29.33) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.72) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $55.69) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $14.65 – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $23.15) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $12.92) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.44) – Buy under $13, target price $30+

Velo3D (VLD – $0.27) – Buy under $6, target price $50

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $4.85) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.39) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.78) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $10.01) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $7.66) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.79) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.65 – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $13.44) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($22.80) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $21.33) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $26.05) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.50) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $22.99) – Buy under $30, target price $50

Coeur Mining (CDE – $2.66) – Buy under $5, target price $20

First Majestic Mining (AG – $4.48) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.12 – Buy under $10, target price $25

Sprott Inc. (SII – $37.00) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $51,619.38) – Buy

iShares Bitcoin Trust (IBIT – $29.72) – Buy

Ethereum (ETH-USD – $2,979.87) – Buy

Grayscale Ethereum Trust (ETHE – $25.88) – Buy

Commodities

Vermilion Energy (VET – $11.01) – Buy under $11; $24 target

Crude Oil Futures – July 2026 (CLN26.NYM – $67.19 – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.55) – Buy under $40; $100+ target

EQT (EQT – $37.32) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.10) – Buy under $8; $30 target

Freeport McMoRan (FCX – $38.67) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.00) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $20.85) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.12) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $25.75) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.21) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.04) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.80) – Hold for buyout

Invitae (NVTAQ – $0.01) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

I’ll second that….

MM–on UUUU, with bullish forecasts on the uranium price, why is the stock plunging of late? When and where’s the bottom for the stock?

Uranium is tied to oil prices. Oil is well off it’s high and uranium reflects that. If MM is right about a recession, oil and uranium will drop hard. I don’t think he’s right though. Any hint of a recession and Powell will be doing the rate cut boogie.

I fear that today’s earnings report isn’t going to do the stock any favors. We’ll probably see a price dip at the beginning of next week, and it could easily test the year-ago $5 low before too long. I like the uranium thesis, but I’m not sure that UUUU makes as much sense as Cameco, which has performed much more strongly over the last 2 years.

I estimate ENVX has about two years of cash (at recent spend rates) and about 14 months until they can potentially begin receiving production revenue. Do you expect a raise before this time, e.g. ~Jan. 2025?

re: “Nvidia is successfully accelerating contracted production of their AI processors, so supply is going to catch up with demand. That means the quarterly revenue beats and estimate raises are coming to an end”

I don’t draw the same conclusion. If supply catches up, that means they can meet increased demand, not that demand is decreasing. One could argue that the margin may begin to decrease since there won’t be multiple demands for a given GPU. But I expect it to be a bit of a wash. And I expect demand to further increase, especially if price comes down a bit. I also think they will have “layered” demand — those that are first time purchasers of their GPUs and those that are upgrading to the latest high performance GPUs being offered. This could occur every 2-3 years, if a company wants to be a market leader with their capability.

grabbed those 505 puts today Micheal at 7.50 a contract. wondering what your stop loss would be if the trade decided to go the wrong way thanks

Options have got to be one of the hardest ways to play the market. You need to get the direction AND the timing correct. Very difficult. Stop losses are rough as well as overnight action can kill your option values before the market action opens.

I’ve lost more money on options than I would ever admit 🙂

same hear on money lost in options. i do like the 505 risk reward. i know hope is not a trading style. IF!!! we get that pull back over the next 2 weeks to like 490ish? this option will pay out nicely. did not go with the 410 put to far out of the money. learn my lesson on that with nvda calls. bought the march 1 900 calls at 3.00 dollars 2 minutes before the market close on the day they announced earnings. stock went up 110 dollars the next day and option opened at 1.50. and closed around that price. had to do a double take thought i bought a put. learned about IV crush on that one, buying an option before earnings you are paying a premium. luckily yesterday push up to around 810 area on NVDA i was able to get out at break even. reason i was asking stop loss is if the SPY keeps pushing over the next 2 weeks 510,515,518 do you have a mental stop where you are thinking of cutting your losses thanks Micheal.

If a recession is coming, would oil be a buy? Seems counterintuitive.

Insurance rarely works out, especially given the rather tight timelines you are suggesting. If the Fed even smells a hint of a recession, they will be sending out their talking heads talking about rate cuts. Can’t have a recession in an election year .. wink wink.

good point about how having a recession in an election year. the democrats or the republicans( if the president was republican ) would be throwing so much money anywhere they could not to have a recession in an election year. it is basically signing your own death wish buy letting a recession happening in a election year if you are in charge.

Recession with significant inflation would keep interest rates steady, so that would be negative for oil. But recession with low inflation would allow rate cuts, positive for oil. The uncertainty of these statements is that the market looks ahead, anticipating these things with an uncertain time frame. Gold also reacts similarly with rate cuts, as in the 90’s and 2000-10 or so when there was little inflation and rates were low. Gold rose.

Anyone here buy BLGO, which I mentioned last week? Up over 19% today on relatively HUGE volume.

Lovin it. Always interested in what you have to say and investment ideas. Thanks

Tx also for your recommendations Chris,still holding ACXP,looking at blgo

I was swamped last week and missed your post. Damn . But thank you anyway. Very much appreciate your input, Chris. Are they projecting future good news ?

See below

I missed also, Chris, is BLGO still a buy? What are your other top recos to buy right now: ACXP? JGMD? NGENF? Appreciate your feedback

Is BLGO still a buy? I say “YES. but … Don’t invest more than you can afford to lose. The company could be worth many times its current price if 1) the EPA enacts its proposed PFAS rule after the 60 day comment period ends, AND 2) BLGO’s PFAS solution recently installed in NJ works as well as advertised.

Here’s what I posted after the close on Friday, Feb 16 when shares closed under 30 cents (now at 39 cents):

I don’t think I have previously mentioned this speculative stock that I recently bought which could be HUGE. I first became aware of BLGO watching an investor conference more than a year ago, maybe late 2022. The company has various divisions working on disparate science problems and has yet to make a profit. It had a large scale battery project, an odor removal product on the verge of commercialization and some kind of water pollution control technology among other things. The idea was to commercialize these technologies with willing partners who specialized in those industries and when shown to be profitable, sell the tech and collect royalties. I did not see them as investable at the time. At the end of 2023 I took another look and decided it was worth investing a bit of my money as the stock was trading under 18 cents but was growing revenues, had a pet odor removal product that was selling in all the big retailers and appearing in tv commercials. Company revenues doubled in 2023 over 2022 and had doubled from 2021 to 2022. I thought the company could be profitable in 2024 and with an annual profit of 1 or 2 cents might even appear cheap on a P/E basis. I went back and looked at them again, focusing on their water pollution solution. They said their solution for removing PFAS chemicals from water produces only 2 pounds of toxic waste compared to competitors producing 800,000 pounds of toxic waste https://www.wateronline.com/doc/biolargo-s-solution-for-effective-low-waste-pfas-removal-and-destruction-0001 and that they were on the verge, they believed, of signing a deal with a municipal water company to buy their equipment. On Dec 20, 2023, BLGO announced the deal was signed.

“Once the system is installed, BioLargo will enter into an ongoing service contract for the maintenance of the system as well as the removal and disposal and destruction of the PFAS-laden waste.

John W. Clark, Jr. President of Lake Stockholm Systems, Inc. said, “After an extensive review of the available technologies, including input from our engineers and the state of New Jersey, we selected the BioLargo AEC to ensure the drinking water in our community was free of harmful PFAS chemicals. BioLargo’s solution will give us the peace of mind and guarantee that we can meet remediation requirements, both today and in the future.”

I also knew that the EPA was considering making rules limiting the amount of PFAS chemicals that might be acceptable. I figured if BLGO’s solution is that much better and every water company in America needs to eliminate or reduce these chemicals, this could be very big.

Then on Feb 3, 2024, a link to this piece of news appeared in my inbox:

https://www.epa.gov/hw/proposal-list-nine-and-polyfluoroalkyl-compounds-resource-conservation-and-recovery-act This news link shows that the EPA has published its proposed new rule regarding PFAS chemicals and put it out for a 60 day period during which anyone can submit their comments regarding the rule. It looks like PFAS regulation is “just around the corner”. Do your own diligence, but it looks to me like everything may be falling into place for this company.

HAHA, I am now a stock symbol.

I hate ACXP at current prices. It is in limbo waiting for Luci to nail down a deal with a partner to fund phase 3. With the tiny number of successful patients in phase 2, there is no way a BP would offer more than $5 without phase 3. It would be more prudent for BP to fund phase 3 and get it done quicker than ACXP could alone. At the end of the last New to the Street interview, Luci said that sometime in 2024 there would either be a deal, or ACXP would have to go it alone. He was glib in saying that he would raise some money beyond his cash balance of $7 million to do that. He said it will be “a nip or a tuck.” I really hate flowery euphemistic language like that, the mark of an untrustworthy salesman. We could sit for the rest of the year, and the stock could decline to $1-2. Upon news of BP funding of phase 3, the stock might advance to $6, and settle down lower to $4-5 while we wait for results. I would be happy with that, which is why I am holding but not selling now. In 9 months with no news, I might gamble and buy more at a cheap tax selling price near $1.

NGENF is worth the wait until Q3 when they finally report SCI trial results. Chris said that we should have most of our position by then. I agree.

Bought a small position.

As I sit here still trying to come to the realty from my investment in NVTA waiting for April 17th in hopes of it going to 5 cents, just to think 3 years ago right about now it was trading for 38.50 with all the knowledge and experience that MM had on it,as he stated the company was doing everything right and were on there way to becoming the Amazon of genetic testing buying up 50 dollars a share,the saddest part is he as alot of us still believed in his research and continued to dollar cost average all the way down,listening to his recommendations on the stock,he had always been positive though,he never saw a red flag with it ,so I in turn had faith,Feb 1st newsletter still was recommending to buy up until 10.00 stock closed that week at 39 cents and then we all saw what happen monday,to all of you who did what I did,I feel your pain,believe in yourself and your own abilities,the sun does reappear but not for NVTA .Have a blessed day,nvta sitting at a penny

Well said! unfortunately, you are not alone.

Fyi,lawsuits ate out against NVTA ,has anyone here ever recouped any money after signing up for this,or is it just a waste of time,they should all go to jail the board the way they pulled this off ,they were cost cutting and everything else,didn’t ever have the curiosity to the shareholders to wait for the earnings to post,the top 3 got 1.7 million a piece,they got paid,they need to shut this company down…

I did recover significant amounts from Arena (MM recommendation) settlement but that was a non-bankrupt company. Can’t remember the exact amount but it was in the thousands so it was worth filing the claim. I think the money arrived 2-3 years down the road.

Nice tx guess that’s what has to be done

Bought QUIK 383 @$13.03 and $13.03 on 2/26/2024.Record earns today. Thanks MM for your recent post.

Somebody (over at SA) likes ENVX:

https://seekingalpha.com/article/4674222-enovix-q4-a-solid-entry-point-technical-analysis?mailingid=34502711&messageid=2800&serial=34502711.552&utm_campaign=rta-stock-article&utm_medium=email&utm_source=seeking_alpha&utm_term=34502711.552

I hope this is in Potter’s wheelhouse and not potter’s field.

The DOW and the Nasdaq were both down today. However, QUIK was up. Closing at $15.67 . My shares were up 23.28 percent today. Thank you again MM for your timely post of the two analysts who said QUIK was about to report record earnings.

Is anyone watching MDNAF (a M. Murphy recommendation)? I got it at 30 cents, and it just hit 1.07 and has backed down at this point to 90 cents ( a triple). Michael has a $20 first target. I checked several other sites that show a one year target of about $7.00.

William, what’s the catalyst that will drive it, I cant find the newsletter write up on it? Do you believe this is for real and can hit $7 or close to $7? Any other subscriber opinions on this one is very welcome – including you MM!

William, can you advise of the other websites touting this stock? Thanks

It’s under 20-1 list above (it is Medicenna). It’s a canadian business. I didn’t read write ups. I looked for “MDNA FORECASTS”. Murph did a write up of it a while back. It is a drug development business.You can probably find a web site for the company.

I ‘ve got to go for now. Will try to find something later.

A couple of forecasts for MDNAF. There are a number of lesser forecasts. I’m not trying to sell it. Murphy wrote a good word I believe back in late 2023. I don’t know why the sudden surge.

https://fintel.io/s/us/mdnaf

https://www.barchart.com/stocks/quotes/MDNAF/analyst-ratings

This was a Murphy write up 10-13-23. I won’t make any more references about MDNAF. It just looks like a stock on the move.

Medicenna (MDNA – $0.29) appointed Humphrey Gardner, MD, as Chief Medical Officer (CMO). He has over 30 years of experience, starting as Assistant Professor at The Scripps Research Institute, Research Fellow at the Whitehead Institute at MIT, and Clinical Fellow at Harvard Medical School. He then held senior roles at AstraZeneca as Clinical Vice President Translational Medicine, Oncology; Novartis as Executive Director, Oncology Translational Laboratories; and Biogen. Then he was the CMO at Stingthera, CMO in Residence at Roivant Sciences, and Chief of Medical Oncology at Evelo Biosciences. Most recently, Dr. Gardner served as CMO at Harbour BioMed, advancing novel antibody and bispecific therapeutics in oncology. He has leadership experiences advancing immune-based therapies for cancer and other diseases from the earliest stages of development through regulatory approvals. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

Thanks William, much appreciated!

MM – do you have an update on MDNAF? Whats date of first drug approval in 2024? Is this a good near term risk?

I’m no stock guru but I think the best shot at success is ACXP. Not a MM pick. Chris told us about it and I have read every thing I could on it. Market cap 40 million,float 13 million shares. CEO is a lawyer familiar with M and A. Sold companies in past with far less data. Big pharma is sitting on 25 billion dollars. I think they’ll pay half a billion for a drug worth a billion a year. I do wish MM would take a look at it and give us his take. Seems like a long shot but maybe not so long. To make a lot of money would love to roll profits to NGENF if it can stay down. Own both in a roth so no taxes if it works.

I always read every comment from JGMD and Chris and look forward to it. Would like to buy stock in JGMD (just kidding). I do think there’s a chance of a buy out for ACXP in quarter 2 but maybe just wishful thinking.

Read my negative comments about ACXP from yesterday just above. Today, I think the downside risk is much greater than the upside for the next 9 months. If they get a partner for phase 3, the upside in 2025 or later is well over $10, maybe over $20. If you don’t own any, you could buy a small position now at $2.80 so you don’t miss out in case Luci makes progress sooner than I estimate. But for the bulk of your position, I would wait until tax selling time in Dec when you might buy a lot around $1 or whatever the price is at that time, but no higher than $2.00.

Congrats to William Cunningham who scored a triple on Medicenna from 30 to 90 cents. That’s the only way to buy NWI spec stocks–after they have plunged 95-99% from MM’s buy prices. You’ll miss a few winners, but you won’t die in poverty which has happened to at least one former subscriber.

I thought I was a genius when I bought my initial position in VLD at $1.50 a few months ago when MM said it was a gift. I was following it since he recommended it over a year ago at $10 with a PT of $50. I tripled up on my next buy late Dec at 47 cents. Last week I doubled up on top of that at 29.5 cents and 24.5 cents. My average cost basis is 44 cents on a huge position. I am now down only 40%, but subscribers who bought at $10 are down 97.3%. The most level-headed poster on YMB, Lazerator got me interested in accumulating a large position, which is still only 3% of my portfolio. You will recognize my posts there, learning a lot from him. VLD is my most followed stock, and my top recommendation if you can deal with risks. Buy below 27 cents, not below 6 DOLLARS which MM refuses to revise. The earnings update will be up to a month late, Mar 31. So the month of March will be the best opportunity. Sales will be terrible, but Lazerator thinks that this scenario is mostly already reflected in the current price. He has been buying more times than I from high prices, and he even bought some more today. What nerve!!

I spend lots of time following TGTX. My average cost is $6. In this case I agree with MM’s buy below $12 and PT of $30+ in a buyout. If you bought at $17 today, you will likely make money, but the margin of safety is too small. In a news vacuum, or when shorts beat it down, I plan to buy more at $10-12. Crazy uber bulls are predicting $100 as soon as 2025. I objectively present analysis, but they give me universal thumbs down lately. That’s how I know that today’s $17 price is merely overheated enthusiasm. I think it can reach $100-200, but it will take many years.

New World Investor for 2.29.24 is posted.