Dear New World Investor:

Scotland Yard detective Gregory: “Is there any other point to which you would wish to draw my attention?”

Sherlock Holmes: “To the curious incident of the dog in the night-time.”

Gregory: “The dog did nothing in the night-time.”

Holmes: ”That was the curious incident.”

– From The Adventure of Silver Blaze by Arthur Conan Doyle

This morning’s January Personal Consumption Expenditures (PCE) Index rose 2.4% from last year, a slowdown from December’s 2.6%. The core PCE Index, the Fed’s favorite inflation indicator, rose only 2.8% from last year. That was the lowest annual increase since the 2.2% increase in March 2021.

But the stock market did not explode higher until the usual end-of-day ramp, and that was the dog that didn’t bark. It tells you everyone who wants to buy stocks right now has done so, and they’re waiting for someone else to push up stock prices. But for now, “someone else” seems to be AWOL. The most likely short-term path forward is down.

Most investors are asking the second-biggest question: “How long can the current uptrend continue?” That means last week’s recommendations of some portfolio insurance seems especially timely if you are worried about a decline lasting a few months. Whether you buy the April 30 SPY $505 put (SPY240430P00505000), the April 30 SPY $410 put (SPY240430P00410000); a reverse index fund like the ProShares Short S&P 500 ETF (SH), ProShares UltraShort S&P 500 ETF (SDS), orProShares UltraPro Short S&P 500 ETF (SPXU); or an increasing volatility fund like the ProShares Ultra VIX Short-Term Futures ETF (UVXY), you should do OK.

Remember that portfolio protection is insurance, and the cost of it is the insurance premium. Just like you don’t want your house to burn down so you can collect on your fire insurance, or your car to be wrecked, you don’t want to make money on portfolio insurance. It’s there to let you stay invested in this secular bull market that won’t hit a major top until 2036. Consider the cost of portfolio insurance as an expense – gone money you never will see again.

The biggest question every investor should be asking but isn’t: “Can I stay invested in the great bull market to 2036?” To the extent history is of any use, this rally is still far more subdued than the great melt-up of 1999 and 2000. The Nasdaq 100 (NDX) is around 35x trailing 12-month earnings. In the late ’90s tech bubble it went into the 90s. Which side of 1999 are you on?

Click for larger graphic h/t @TheMarketEar

Click for larger graphic h/t @TheMarketEar

Another way to look at that is in 1994, the surge in IT capital spending and productivity started a multi-year uptrend for Nasdaq. This time around, I believe ChatGPT in 2022 was just the beginning of a much bigger uptrend driven by the AI and metaverse revolution.

Click for larger graphic h/t @TheMarketEar

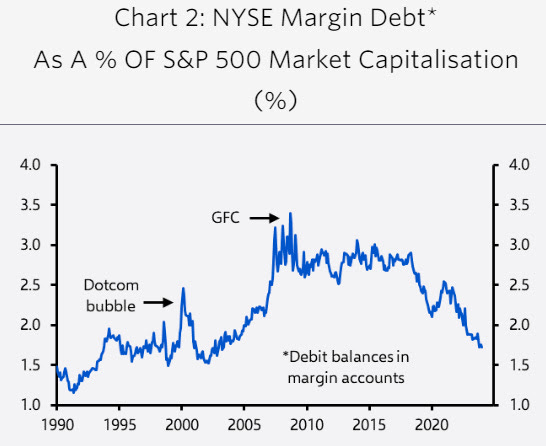

And unlike most bubbles, we aren’t seeing obvious signs of high and rising leverage. Margin debt has actually been falling recently. As has the ratio of margin debt to the size of the stock market.

Click for larger graphic h/t John Authers

Click for larger graphic h/t John Authers

Fed officials have signaled they do not need better news on inflation to cut rates, just continued good news. The trend in inflation still is downward and that’s good news. But I still don’t think they’ll cut the Fed funds rate until August or September, and Wall Street still believes there will be three cuts this year starting in May or June. That could keep a lid on stock prices for a while.

Market Outlook

The S&P 500 added 0.2% since last Thursday to a new record close today. It is up 6.8% year-to-date after booking the best February since 2015. The Nasdaq Composite gained 0.3% to an all-time record, its first record close since November 2021. The Naz is up 7.2% for the year and also had its best February since 2015. The SPDR S&P Biotech Exchange-Traded Fund (XBI) won the week, climbing 4.5%. It is up 10.2% year-to-date. The small-cap Russell 2000 rose 1.1% and is barely up in 2024, just 1.4%.

The fractal dimension is as stretched as I’ve ever seen it. The S&P could go sideways for several weeks in the necessary consolidation, or take a sharp, temporary dip.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model still is looking for strong 3.0% real GDP growth in the March quarter. The Blue Chip economists are slowly getting on board.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, March 1

GLW – Corning – 1on1s – Susquehanna Technology Conference

Monday, March 4

AG – First Majestic – Unspec. – Prospectors & Developers Association of Canada’s (PDAC)

FSLY – Fastly – 11:25am – Raymond James Institutional Investors Conference

CMPS – Compass Pathways – 12:50pm – TD Cowen Health Care Conference

Tuesday, March 5

GLW – Corning – 11:00am – Morgan Stanley Technology, Media & Telecom Conference

GILD – Gilead – 12:50pm – TD Cowen Health Care Conference

ABCL – AbCellera – 2:50pm – TD Cowen Health Care Conference

Wednesday, March 6

VET – Vermilion Energy – After the close – Earnings release; call tomorrow

FSLY – Fastly – 12:30pm – Morgan Stanley Technology, Media & Telecom Conference

INO – Inovio – 4:30pm – Earnings conference call

Thursday, March 7

VET – Vermilion Energy – 11:00am – Earnings conference call

Friday, March 8

February payrolls – 8:30am

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $180.75) is canceling their decade-long project to build an electric car and transferring most of the 2,000 people working on it to their artificial intelligence division to focus on generative AI projects,

Is this, as Yahoo Finance wrote, “abandoning one of the most ambitious projects in the history of the company?” Nope. The car was a testbed for AI development, as should be obvious from how many employees were transferred to the artificial intelligence division. We are going to see a lot of Apple AI at the World-Wide Developers Conference in June and a lot of AI features in iPhone 16 in September.

Since my December 17, 2015, Buy recommendation at $27.25, Apple has treated us well (as has Meta):

Click for larger graphic

Click for larger graphic

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $72.10) got FDA approval to expand Biktarvy’s label to include people with HIV who have suppressed viral loads with known or suspected M184V/I resistance, a common form of treatment resistance. HIV treatment resistance is permanent and irreversible, which can jeopardize future treatment options. The M184V/I resistance mutation has been found to be present in a range (22%-63%) of patients with pre-existing resistance. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $490.13) is expanding Instagram’s creator marketplace to eight new markets – Canada, Australia, New Zealand, United Kingdom, Japan, India, and Brazil – to help more brands and creators work together on partnerships.

At the same time, they’re testing new machine learning-based recommendations that use Instagram data to help brands discover creators who are the best fit for their campaigns. Since this stated in the US in 2022, they have on-boarded thousands of creators and brands. META is a Buy under $345 for a $400 target in 2024.

Small Tech

QuickLogic (QUIK – $14.92) reported December quarter revenues up 83.8% from last year to $7.5 million, driven by record high IP revenue and right on the $7.4 million consensus estimate. Pro forma earnings of 18¢ per share clobbered the 13¢ estimate.

On the conference call (PREPARED REMARKS HERE and TRANSCRIPT HERE), CEO Brian Faith said: “The short story here is the IP business model we launched in 2020 is delivering strong results. Over the last three years, we have delivered a top-line growth of 146%, increased our Non-GAAP gross profit dollars by over 230%, and with a modest decrease in Non-GAAP operating expenses, improved our operating leverage by over 250%. With this performance, a profitable year now under our belt, and an outlook for continued growth driven mostly by new IP customers, I think it’s fair to say our IP business model has developed solid traction.”

On Wednesday they announced a seven-figure IP contract with a top-tier defense customer. This design is for a new ultra-low-power system on a chip (SoC) that is targeting a variety of commercial and industrial Internet of Things (IoT) applications as well as aerospace and defense applications outside the US. This design is government-funded and will be fabricated by Taiwan Semiconductor (TSMC) on their 12 nanometer process. Within the SoC, QuickLogic’s eFPGA technology is used for AI acceleration, which is a necessary function in most AI applications.

They guided for March quarter revenues to grow 50% from last year to $6.2 million. The pro forma gross profit margin will be 70%, yielding $4.34 million in gross profit. Pro forma operating expenses will be about $3.5 million each quarter this year, so they expect a pretax profit between $0.5 million and $1.1 million, or three cents to eight cents a share.

Management expects 30% revenue growth in 2024, which is realistic given their record $168 million opportunity funnel. Plus, Samsung has worked through its excess inventory and QUIK resumed shipping during the December quarter to support production. They expect the volume to increase in 2024 as they were selected for new designs that will ship into 2025.

QuickLogic ended the quarter with $24.6 million in cash. Wall Street was late to this powerful turnaround story and the stock jumped 23.3% on Wednesday. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $4.59) reported December quarter revenues up 15.9% from last year to $59.99 million, short of the $61.21 estimate. On a GAAP basis they lost 10¢ per share, a tad worse than the nine-cent loss estimate.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they signed 25 launch deals in 2023, including 18 Electron and seven HASTE launches. They’ve done two launches so far in the current quarter with two more scheduled for March.

Only SpaceX and Rocket Lab have launched, orbited, and successfully re-entered a capsule and payload to land on Earth.

Click for larger graphic

Click for larger graphic

Management guided for March quarter revenues up 67.6% to 78.6% from last year to $92 million to $98 million, slightly under the $98.57 million consensus estimate, That includes Launch Services revenue of $32 million to $33 million and Space Systems revenue of $60 million to $65 million. The adjusted EBITDA loss was guided to $28 million to $30 million, or about six cents a share. The consensus was expecting a loss of nine cents a share.

They now have a $1+ billion backlog across a diverse customer base, including civil, defense, and national security and government customers, as well as commercial constellation operators:

Click for larger graphic

Click for larger graphic

CEO Peter Best said: “As we’ve delivered more and more successful spacecraft missions, demand for these spacecraft or similar variants on them has grown. So we’ve expanded beyond Photon to create a full family of standard spacecraft buses. So allow me to formally introduce Lightning, Pioneer, Explorer, and of course the original Photon. Lightning is our newest spacecraft bus designed for a twelve-year-plus orbital lifespan in LEO. It utilizes electric propulsion, delivers high power and radiation tolerance, and incorporates full redundancy in all critical subsystems. This is a half-ton, three-kilowatt bus, ideal for communications, imaging, and remote sensing.

“Then there’s Pioneer, a highly configurable platform designed to support large payloads and unique mission profiles, including reentry. For interplanetary missions there’s Explorer, a high delta V spacecraft with around about a kilowatt of power, large propellant tanks, and precision orbit determination system ranging transponder, and all the things you need to go into deep space. Explorer enables small spacecraft missions to planetary destinations, near-Earth objects, and Earth-moon Lagrange points. And of course, Photon is sticking around as the original spacecraft plus launch option.

“Thanks to our vertical integration strategy, these spacecraft share many common components and subsystems designed and manufactured in-house by us, enabling us to deliver spacecraft quickly, affordably, and reliably using flight-proven components. Each of the spacecraft are currently on order in a range of quantities, with 40 plus satellites currently in our production backlog. So from humble beginnings with one spacecraft just four years ago, to a full family of them designed to serve commercial and government partners is certainly an exciting time for our space systems business.”

Neutron is coming with the first launch planned for the end of 2024, three in 2025, and five in 2026. The first engine build is nearing completion in preparation for the first hot fire. A Neutron mission will generate much higher revenue than an Electron mission.

Click for larger graphic

One surprising thing the CEO said was: “’I’ll remind you that the end goal here is not just to be a bus provider or even a prime. It’s to ultimately have our own constellation in orbit providing services because that’s where we ultimately think this all goes.”

Why? Because, he added: “If you read any of the reports where the space industry is, the value of the space industry going, whether it’s $1 trillion or a $2 trillion, pick your report. It’s always true that the vast majority of all of that TAM is going to reside in the services that you provide, not being the freight truck that gets it there or the car builder that builds the truck. It’s actually the service. And what we’ve been very methodically going about doing is building all the infrastructure that we need to be able to ultimately provide a service.

“Now, the natural question that always comes after that is, well, what service are you going to provide? And I don’t think we’re ready to talk about any of that yet. But what I can say is that when we look to jump into that larger tam, we will have a very disruptive way of going in there and executing and providing that service, because we will be able to build whatever spacecraft we require using all of our own components, and it will fly in our own rocket.

“And I think you’ve seen one other real-life example of that with Starlink and with Internet from space. And it’s very, very difficult to compete with that unless you have your own ability to manufacture your satellites using your own components and your own ability to launch those you know said satellites. So we’re just marching very methodically towards that step after step.”

The company finished the quarter with the resources to execute their plans, including $327.9 million in cash. They’ll spend about $100 million on R&D and capital spending for the Neutron program this year, but after that they should become cash flow positive pretty quickly. I think 2024 is the last year to build a Rocket Lab position inexpensively. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $0.27) former CEO Benny Buller is selling 2,000 shares every day. He still owns 5.06 million shares.

The company announced Flow Deneloper, a new feature in their Flow 7.0 print preparation software that greatly simplifies the migration of existing additive manufacturing projects to Velo3D’s fully integrated solution. Users can transfer their experience and knowledge from previous projects by importing proven parameters they have developed, develop new material processes, and control their optimization objectives.

It can be challenging to produce repeatable results across different metal 3D printers, even when they’re the same model of printer. Developer can consistently produce parts within spec across any of VLDs printers, which provides obvious benefits for companies to scale production of their parts. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $5.05) said Peter Thiel has decided to resign from the board for personal reasons. I happen to know he does have personal reasons right now, so this doesn’t bother me. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.58) is closing in on the March 27 PDUFA date for vadadustat and may run up into it, even though the big launch won’t come until October, after TDAPA approval (which is automatic once they get FDA approval). Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after FDA approval in March 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat PDUFA date 3/27/24

Probable time of next FDA approval: March 27, 2024; TDAPA October

Probable time of next financing: Late 2024 or never

Compass Pathways (CMPS – $) reported a December quarter loss of 53¢ this morning, missing the 35¢ loss estimate. On the conference call (TRANSCRIPT HERE), management said their overall Phase III clinical program completion remains on track. But they are experiencing some recruitment delays in the 005 trial, because they are formally confirming every patient’s treatment-resistant depression (TRD) diagnosis.

This has been a challenge in the US because medical record keeping is decentralized, which slowed the pace of screening and enrolling. However, now that nearly all 005 sites are open and with the addition of resources, they will see an increased pace of recruitment, which should help improve enrollment.

This problem is specific to the US clinical sites. They don’t see the same impacts to COMP006, which is a global trial that remains on track, with top-line data from the 006 trial still expected in the middle of 2025. But it extends their guidance for top-line data from the 005 trial from the middle of 2024 into the December quarter.

Importantly, this change in guidance does NOT impact the expected timing of the submission of their NDA filing, because results from both trials always were required for NDA submission in late 2025. That’s also the target for completing all the necessary preclinical and clinical pharmacology studies for a complete NDA dossier.

Compass did an exploratory Phase II safety study of 22 PTSD patients who have been followed for 12 weeks. We’ll see the full data set including efficacy later this Spring. I expect it to be good and pop the stock.

They finished the quarter with $220.2 million in cash and have raised another $31.4 million since then. In the March quarter they expect to use $17 million to $23 million. For the full year they expect to use $110 million to $130 million. The cash position at December 31, 2023, together with the net cash raised to date in the first quarter, is expected to be sufficient to fund operating expenses and capital expenditure requirements into late 2025. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inovio (INO – $8.86) reports December quarter results next Tuesday. The four publishing analysts have estimates ranging from a loss of $1.83 a share to -96¢ per share, with a consensus average of a $1.27 per share loss. As always, the important news will be progress on their various trials. The most important will be any update on preparing to file the Biologics Licensing Application (BLA) for INO-3107 for recurrent respiratory papillomatosis (RRP). INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

TG Therapeutics (TGTX – $17.22) jumped after they reported (1) three new patents for Briumvi extending protection through 2042; (2) their partner Neuraxpharm’s European launch of Briumvi in Germany, with additional launches throughout Europe to follow; and (3) December quarter revenues of $43.97 million, much better than the $40.06 million Wall Street expected. $39.9 million was from Briumvi, which included $3.2 million sold to Neuraxpharm in support of that commercial launch. The GAAP loss of $14.4 million or nine cents a share beat the 11¢ loss estimate.

On the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Michael Weiss said Briumvi has had 3,200 prescriptions from 640 healthcare providers at 400 centers.

He said: “…this is a competitive market and BRIUMVI is the newest entry, so differentiation matters. One obvious difference is that BRIUMVI is the only anti-CD20 monoclonal antibody that can be given as a one-hour infusion every six months after the starting dose, which may be an attractive profile for both patients who want to get back to their daily lives and for healthcare practices seeking to increase the efficiency within their infusion suites.

“Beyond the one-hour infusion, we are excited to continue to explore biological-based differences that may not be as readily apparent, but are perhaps clinically relevant. As a reminder, BRIUMVI is differentiated by design, having been glycoengineered for enhanced immune effector cell engagement and efficient B-cell depletion.

“Preclinical data demonstrates that compared to the other anti-CD20s approved or used to treat MS, BRIUMVI has the highest binding affinity to CD20. The target for these types of drugs found on B-cells, and through its glycoengineering has the ability to induce the highest level of antibody-dependent cellular cytotoxicity regardless of patient-specific polymorphisms.

“Whether or not these biological attributes of BRIUMVI have clinical relevance in patients with MS has not yet been determined, as no head-to-head trials have been conducted for BRIUMVI versus the other anti-CD20s. However, what has been well established is that BRIUMVI is the only anti-CD20 monoclonal antibody to achieve an annualized relapse rate of less than 0.1 in Phase 3 trials.

“Also, in clinical trials, BRIUMVI rapidly depleted B-cells with a median of 96% reduction within 24 hours and 95% on-time infusion completion rate, which we believe speaks to the tolerability profile of BRIUMVI.

“As we move forward, we are eager to explore to what degree the design attributes of BRIUMVI may be contributing to the robust activity scene. We plan to do more work to evaluate some of these unique attributes and to understand whether the molecular and non-clinical differentiation translates into clinical differences.”

In 2024 they will begin clinical development of subcutaneous Briumvi. They also will start a trial of Briumvi in an other autoimmune diseases. They will start a trial of the recently in-licensed azer-cel in autoimmune disease.

They plan to present data “at multiple conferences throughout the year” from the ENHANCE Phase 3b trial evaluating patients who switch from prior CD20 therapy to Briumvi.,

Mike guided for full-year 2024 Briumvi sales of $220 million to $260 million, up about 150% to 200% from $88.8 million in 2023. Plus they’ll get launch milestone payments and royalties from Neuraxpharm, including $12.5 million for Germany. He is targeting operating expenses of $250 million, including R&D, so they’ll get close to or hit breakeven. The company finished the quarter with $217.5 million in cash, enough to take them to cash flow positive.Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,052.20) continues to fluctuate around $2,025 ±$25. The fractal dimension books this as continued consolidation, building up energy for the next push to new highs.

Miners & Related

Coeur Mining (CDE – $2.59) presented at the BMO Global Metals, Mining & Critical Minerals Conference (SLIDES HERE). It was their usual mine-by-mine review, supporting their investment case:

Click for larger graphic

Click for larger graphic

Rochester was top of mind, as usual. It is the largest open pit heap leach operation in North America and the third-largest in the world. It’s also the largest silver reserve asset in the US , third-largest in North America, and fourth-largest in the world. The Rochester expansion is complete and it will be fully ramped up by the end of June.

They privately placed 7.7 million share for $25 million in Canada to fund the Silvertip exploration program. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $4.49) reported their audited 2023 results, which were about the same as the preliminary report when the did their conference call in mid-January. Revenues of $573.8 million were down 8.1% from 2022’s $624.2 million. They had a pro forma loss of $23.8 million or eight cents a share

They produced 26.9 million silver equivalent (AgEq) ounces, consisting of 10.3 million silver ounces and 198,921 gold ounces. The realized average silver price was $23.29 per AgEq ounce, a 4% increase from 2022. Their consolidated cash cost was $14.49 per AgEq ounce and All-In Sustaining Cost (AISC) was $20.16 per AgEq ounce.

Interestingly, they held 300,000 silver bullion ounces in finished goods inventory at the end of the year that have been dedicated to build an initial inventory balance for their minting facility, First Mint. The fair value of this inventory on December 31 was $7.1 million.

They finished the year with $125.6 million of cash. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $4.16) did another, probably paid for, YouTube interview:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $61,205.70) cleared $62,000 for the first time since November 2021, almost hit $64,000 last night, and still could hit $100,000 before the April halving, although time is running out. Big investors are following Michael Saylor’s Microstrategy (MSTR), which recently bought another 3,000 coins for $155 million. That takes him to 193,000 coins. Fear Of Missing Out (FOMO) is in full-on mode, which means we may have to sell into a FOMO peak and step aside for a while. For now, just enjoy it.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

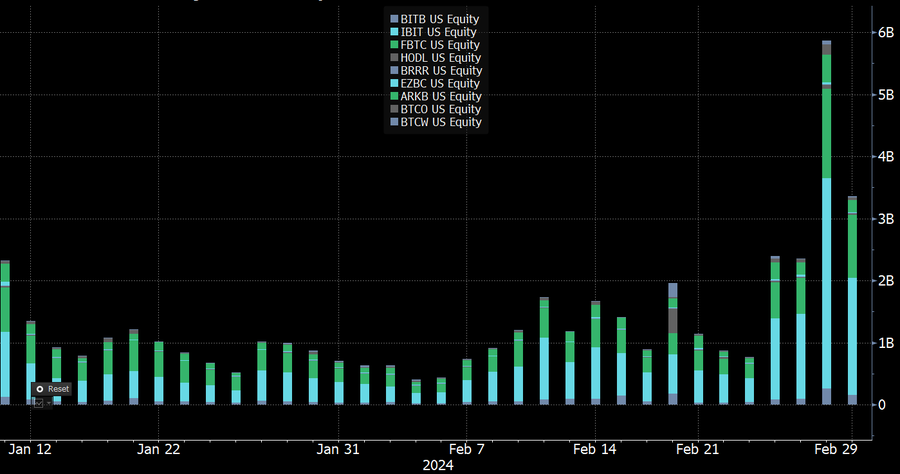

iShares Bitcoin Trust (IBIT- $35.42) traded record daily volumes Monday through Wednesday, as the nine bitcoin exchange-traded funds booked a record $673 million net inflow on Wednesday. That was the largest single-day allocation since their debut in early January. IBIT alone attracted $612 million of inflows, a record high. IBIT is only 0.2% of BlackRock’s ETF lineup but has accounted for 42% of its net inflows so far this year.

Click for larger graphic h/t @EricBalchunas

Click for larger graphic h/t @EricBalchunas

IBIT is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $3,331.65) topped $3,300 for the first time since 2022. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

Grayscale Ethereum Trust (ETHE- $28.88) is pressuring the SEC to convert to an exchange-traded fund, but I suspect it will take another lawsuit to budge Gary Gensler, unless he wants a cushy job with BlackRock. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $78.31

Oil is pinned just under $80 near the highest level of 2024 as China started buying crude cargoes at a higher pace since the Lunar New Year holiday in mid-February, while also increasing orders from Saudi Arabia. At the same time, OPEC+ is considering extending their voluntary oil output cuts into the June quarter and possibly to the end of the year. They want to see oil around $85.

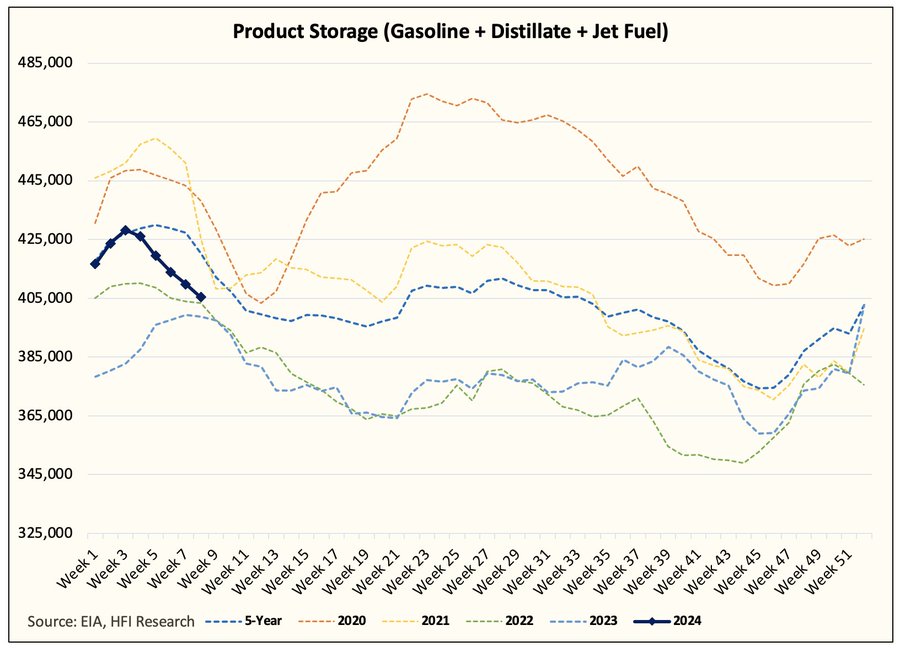

The 3-2-1 US refinery crack spread, a proxy for refining margins, rose to its highest in more than five months. That suggests increased profitability for refineries amid robust consumer demand for petroleum products. Russia announced a six-month ban on gasoline exports from March 1 to compensate for rising demand and to allow for refinery maintenance. Product storage is falling rapidly.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The July 2026 Crude Oil Futures (CLN26.NYM – $67.28) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.35) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.09) reports December quarter results next Wednesday after the close, with a conference call Thursday morning. The consensus expectation of the two publishing analysts is for revenues of either $409.30 million or $473.28 million (average $441.29 million) with earnings per share of 42¢ or 63¢ (average 52¢).

The company acquired another 12.5 million shares of Coelacanth Energy for $9.4 million, giving them a total of 110.2 million shares or 21.88% of Coelacanth. They said the shares were acquired for investment purposes, but now that they’re over 20% they probably have to consolidate Coelacanth’s results. VET is a buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

Energy Fuels (UUUU – $6.33) reported 2023 revenues up a whopping 203.0% from last year to $37.93 million with GAAP earnings of $99.76 million or 63¢ per share. Revenue was comprised primarily of sales of 560,000 pounds of uranium concentrates (U3O8) for $33.28 million, which resulted in a gross profit of $17.96 million and an average gross margin of 54%. They also sold 153 metric tonnes of finished high purity, partially separated mixed rare earth carbonate for $2.85 million and 79,344 pounds of vanadium for $0.87 million.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said their three uranium mines, Pinyon Plain (Arizona), La Sal (Utah) and Pandora (Utah) all began production on schedule.

Click for larger graphic

During 2024, they expect to produce anywhere from 150,000 to 500,000 pounds of U3O8 from newly mined conventional ore, stockpiled ore, and recycled alternate feed materials, depending on the timing of the ramp-up of production at the mines. Once production is fully ramped up at these mines, which is expected by mid- to late-2024, they expect to be producing uranium at a run-rate of 1.1 million to 1.4 million pounds per year.

Energy Fuels is preparing two additional mines, Whirlwind (Colorado) and Nichols Ranch (Wyoming) for expected production within one year. If market conditions remain strong, as I expect, the Whirlwind and Nichols Ranch mines could potentially increase Energy Fuels’ uranium production to a run-rate of over two million pounds of U3O8 per year as early as 2025.

They also are beginning advance permitting on their Roca Honda, Sheep Mountain, and Bullfrog uranium properties for additional uranium production in the future, which could expand their uranium production to a run-rate of up to five million pounds of U3O8 per year.

So far this year, they contracted to sell an additional 100,000 pounds of uranium in March in the spot market at an average sales price of $102.88 per pound, which it expects to result in a gross profit of approximately $66.04 per pound, for a gross profit margin of 64%. As of February 16, the spot price of U3O8 was $102.00 per pound and the long-term price of U3O8, which is the price most relevant for long-term uranium sales contracts, was $72.00 per pound.

They have more inventory to sell in the spot market. In the current quarter they expect to sell approximately 300,000 pounds of uranium under long-term contracts and on the spot market at an expected weighted average sales price of $84.38 per pound at substantially higher gross profit margins.

They are well-positioned in the uranium market:

Click for larger graphic

And in the rare earth elements market:

Click for larger graphic

The company finished the quarter with $57.45 million in cash, $133.04 million of marketable securities (uranium stocks and interest-bearing securities), $38.87 million of inventory worth $76.1 million at current prices, and no debt. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

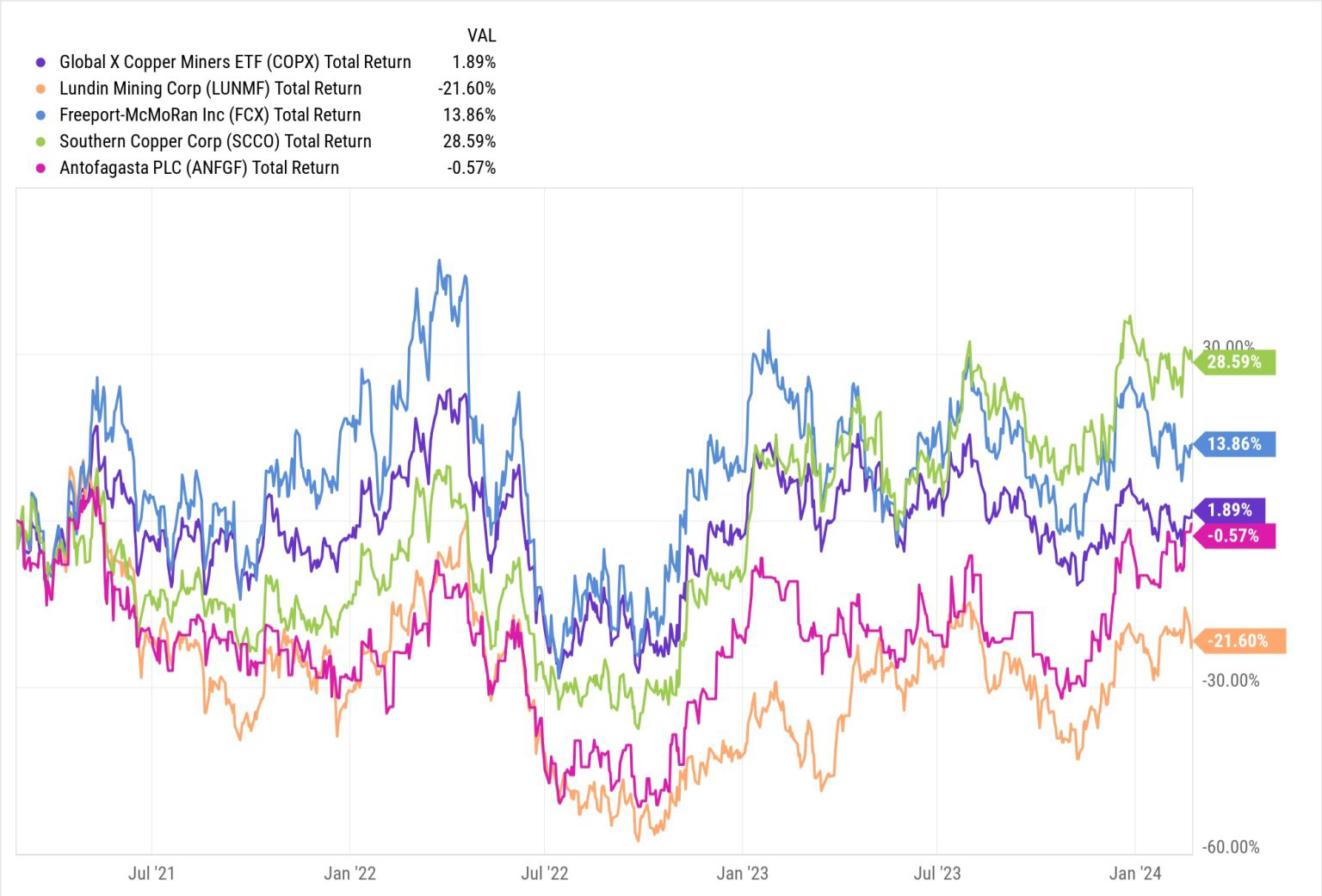

Freeport McMoRan (FCX – $37.81) was teased by Dan Ferris, a well-known value investor, to get subscribers for Stansberry’s The Ferris Report. Here’s what the price of copper has looked like over the past 35 years or so. The emergence of China as an economic force from 2003-2007 was by far the most important driver of copper prices.

Click for larger graphic h/t Stock Gumshoe

Click for larger graphic h/t Stock Gumshoe

Ferris said: “Over the past 11,000 years, all the copper ever mined in history comes to about 700 million metric tons. That’s about three and a half million Statues of Liberty all standing in a line.

“But today – because of the skyrocketing demand – the world needs to mine another 700 million metric tons all over again…But instead of having 11,000 years to do it, it has just 22!

“It’s hard to even get your head around the immensity of the task at hand….A supercycle is a sustained spell of abnormally strong demand growth that producers struggle to match, sparking a rally in prices that can last years or, in some cases, a decade or more. Since 1899, there have only been four distinct supercycles. And they are a dream come true for anyone who is in the right place at the right time…Like you are, right now.

“The last time a copper supercycle took place, Freeport McMoRan surged 1,214%.”

Well, Ferris probably didn’t write that – some copywriter did, after interviewing him – but you get the idea. Over the last three years, in spite of its huge size. FCX has been the second-best performing copper stock behind Southern Copper (SCCO).

Click for larger graphic h/t Stock Gumshoe

The company presented at the BMO Capital Markets Global Metals, Mining & Critical Minerals Conference (WEBINAR HERE and TRANSCRIPT HERE). Richard Adkerson, the current CEO, was downright funny and this was a good insight into the incoming CEO and current CFO, Kathleen Quirk. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

<

* * * * *

* * * * *

Your reading The Law Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 2/29/24. Check out the complete Portfolio page HERE.

Portfolio Protection

April 30 SPY $505 put (SPY240430P00505000 – $6.98)

April 30 SPY $410 put (SPY240430P00410000 – $0.42)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $180.75) – Buy under $150 for new iPhones

Corning (GLW – $32.24) – Buy under $33, target price $60

Gilead Sciences (GILD – $72.10) – Buy under $80, target price $120

Meta (META – $490.13) – Buy under $345, target price $400

SoftBank (SFTBY – $29.62) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.75) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.68) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $14.22) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $24.16) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $14.92) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.59) – Buy under $13, target price $30+

Velo3D (VLD – $0.27) – Buy under $6, target price $50

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $5.05) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.58) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.80) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $10.27) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $8.86) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.83) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.62) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $17.22) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($22.86) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $21.29) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $26.19) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.59) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $23.10) – Buy under $30, target price $50

Coeur Mining (CDE – $2.59) – Buy under $5, target price $20

First Majestic Mining (AG – $4.49) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.31) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.16) – Buy under $10, target price $25

Sprott Inc. (SII – $36.93) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $61,205.70) – Buy

iShares Bitcoin Trust (IBIT – $35.42) – Buy

Ethereum (ETH-USD – $3,366.13) – Buy

Grayscale Ethereum Trust (ETHE – $28.88) – Buy

Commodities

Vermilion Energy (VET – $11.09) – Buy under $11; $24 target

Crude Oil Futures – July 2026 (CLN26.NYM – $67.28) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.35) – Buy under $40; $100+ target

EQT (EQT – $37.15) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.33) – Buy under $8; $30 target

Freeport McMoRan (FCX – $37.81) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.14) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $20.74) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.26) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $25.36) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.20) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.01) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $2.70) – Hold for buyout

Invitae (NVTAQ – $0.01) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

Thanks for the helpful TGTX update, been wondering..

I have trouble understanding why on Feb. 29, 2024 with META at $490, you are targeting META to reach $400 in 2024. Does no one edit?

I have lengthy comments on ACXP, VLD, TGTX at the end of the last board.

RE;ACXP I do appreciate all your input. I went back to last year and it went down to under 2 dollars in August and September. I bought some then but only a couple thousand shares. My average price is well above that.3.25. You could be right but I don’t think it goes under 2 again, because were getting possibly closer to a buy out. When it went under 2 last time they had there 2b trial to do and there was plenty of time. But who knows with stocks. In January 24 it went to over 5. It seemed everybody wanted some.Sometimes they go ballistic to the upside and downside. Unfortunately I think it goes under 2.80 but I hope not by much. I would bet Luci has someone from big pharma help design phase 3. Loved hearing your take so I can be prepared for it. Would also love to hear Chris’s take.

Yes, I thought it was CRAZY when last year there were several quick spikes to $8 that even Chris missed. TGTX a few years ago had CRAZY advances to $50 when it looked like U2 was a winner for malignancies and MS use was just in its infancy. Many TGTX bears point to declining tops despite the current excitement about Briumvi prospects about becoming the CD20 leader.

It is clear that many stocks reach outlandish tops purely based on hope and hype. Later, reality sets in about actually whether phase 3 trials succeed. Many years ago there was a comical NWI subscriber named Show Me the Money, who then changed it to Show Me. How true. To me, it appears that ACXP is in that stage–show me. Of course, Luci as a lawyer is getting help designing the phase 3 trial from a friend in BP, but he is still at the mercy of the FDA. If Luci comes through in a month with a financial deal, the stock may bottom at $2.50 just before that. But come Dec, if Luci doesn’t announce a firm deal with a partner for phase 3 or even confirmation that ACXP is doing it alone, the stock could easily trade at $1 or even lower as a bankruptcy candidate. This happened to Algernon which couldn’t raise money even though their trials for repurposed drugs were supposed to be low cost. The best realistic outcome for ACXP is that a partner funds and expedites phase 3. The stock rises to $6 and settles at $4-5 while we wait for a successful phase 3. Without doing phase 3, a buyout could happen only at $5, because the buyer would be taking a gamble that the phase 3 outcome would be successful. Perhaps the microbiome science is so accurate and predictive that BP might think early buyout is not much of a gamble. Still, their BO offer at this stage will be much less than it would be after successful phase 3, better yet after approval. I don’t think that BP executives gamble with their money, because their board would oust an executive for losing on the gamble. They want to continue to get their multimillion buck salary and other perks. They are not like NWI subscribers who gamble on the stocks at MM’s overly optimistic buy and target prices. I have gambled on TGTX, VLD, AKBA at recent prices MUCH LOWER than original buy prices. I think my bets are reasonable, but I have to admit that I am still gambling.

APTO – Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard

https://www.aptose.com/investors/sec-filings/all-sec-filings

This is not due to the stock price. Rather, the NASDAQ contends that APTO did not obtain shareholder approval prior to issuing stock to Hanmi.

APTO indicated that they will work with NASDAQ to regain compliance.

How is APTO going to argue with bureaucratic NASDAQ, a regulatory body? A company has to do what it needs to do to get funding. No moral sin. All shareholders big and small are passive investors.

Hey Chris – need your insights – what’s your top 2 picks right now with catalysts for rapid price growth the next few months? Thanks

how many is “a few”?

Sorry, didn’t mean to time limit it, I’m looking for a relatively quick 2-3X (3-6 months) then I want to put all profits into TGTX by EOY.

6 months from now will be early September. I think we will have Phase 2 results from NGENF by then (or soon after) and shares will be more than 3x higher. I have very high confidence in that assessment.

I have less confidence that a big BP agreement from ACHV or ACXP will occur in the next 3-6 months but if those happen, they will at least double.

For a quick double, look at NAT. Last week they announced a 12 cent dividend payable April 10 to holders as of Mar 20. Last year NAT pd .15, .15.,12 and .06 in dividends. With Russian oil sanctions, China re-opened and the Suez Canal creating longer voyages (exacerbating a shortage of supply in the tanker market), an aging industry fleet and few replacement tankers coming online, NAT is more profitable than it has been in years (except for when Covid shutdowns began and those who had ordered oil had no options for storage except tankers). The main shareholders just bot more at 4.25. It is down this today at 4.07. With a healthy dividend payment coming up and a very healthy tanker market, I anticipate share price to rise as March 20 approaches, The rise in share price will be accompanied by a rise in the price of Call options. At today’s depressed price I bought NAT April 19 Calls at ten cents and less. I will sell half when I can get .15. Also bot a few Mar 4.50 at .03 but those will expire 3 trading days before NAT goes ex-.

Good stuff Chris, thanks. I’ll buy NGENF after a quick review. So you think NAT will maintain the $.12 quarterly dividend going forward, thats in the 12% yield range?

in fact, could you send me any writeup on NGENF that supports your thesis in a 3X? thanks again

NervGen’s mkt cap today is about $200M they have a drug which has been shown in animal models to improve, with a once daily subcutaneous injection:1) motor function in acute and chronic spinal cord injury (SCI); 2) recovery from stroke; and 3) multiple sclerosis. That drug is now in a Phase 2 trial for people with chronic SCI and will read out in about 6 months. If results are positive in SCI, how much will the company be worth just for SCI which annually costs $50B to treat in the USA and affects an additional 18,000 people each year (290,000 people in the US live with SCI). Let’s say NervGen’s treatment costs $100,000 for a few months of treatment. If only 10,000 people take their drug at $100,000 per, that’s $1B in revenue. And that’s just SCI. Ischemic stroke is a problem roughly 30 times bigger than SCI and also has very limited therapeutic options. A lifetime of treatment for each of America’s est. 1M cases of MS is about $4M per person. TGTX with its MS drug has a mkt cap of $3B. In feline MS models, nothing works better than NervGen’s drug.

By contrast Elon Musk’s Neuralink project wherein he hopes to use electrodes implanted in motor areas of the brain to link to a rec$5Beiver which can operate a keypad or robot by electric signals, recently underwent an addistional round of funding at a valuation of $5B but is still 10 years away from commercialization

https://www.reuters.com/technology/musks-neuralink-valued-about-5-bln-despite-long-road-market-2023-06-05/

When NGENF was 1/2 the current mkt cap I said every $1 invested could eventually be worth $100 and I still believe that. Rich Macary (an early investor in SRPT (mkt cap $3B) said NervGen could be 10 x bigger than SRPT.

So yes, I think this year NGENF will be at least 3x higher than today if the Phase 2 readout is positive.

NGENF is the company doing the most to elevate the quality of life for otherwise healthy victims of neurological injury. All we know now is that about 1 patient so far is rumored to have had some improvement. Whether that means a small improvement of now moving only fingers or the person jumped up and played ball we don’t know. Even a tiny improvement would be exciting news from the scientific point of view. Full enrollment is promised by June 30, and reporting is due Sept 30. Depending on the response rate and minor or major improvement, the stock could remain steady or jump hugely. I am confident of at least a tiny improvement in some of the patients, but to me the stock is still a speculation. Before the great rumor, the stock was in the low $1’s. Now $2.50, the stock already reflects some small improvement in the patients. I got lucky and got a small position at $1.75 after the excitement wound down. I am hoping to buy more at $2.00 or below in the next months. Don’t get giddy and chase the stock.

I am negative on ACXP for maybe 1 year, but optimistic for the long term. ACHV to me is less risky. Both A’s have great drugs that I have good confidence in approvals. They will pay off for investors in due time.

I anticipate the next dividend (after this 12 cent one) to be around 15 cents or more. The tanker business is better now than it was in the first half of last year when they paid back to back 15 cent dividends.

TGTX–I believe it is overvalued at present. Despite the patent extension to 2024 and more trials coming for other autoimmune disease, 2024 guidance hasn’t changed. I am still looking to buy more at $10-12, rather than the current $18. If you make lots of money short term on NGENF, don’t roll it into TGTX at high prices. If buying NGENF now is only 1% of your portfolio and it then becomes 3%, it is worth holding for the really big payoff in 10 years if the great result in rats holds true for people. TGTX is more certain to have big gains, but both are long term prospects. Don’t attempt to change lanes on a fast highway with hairpin turns.

Thanks for the insights JGMD – so youre basically not excited about any major moves on any of the stated stocks this year, is that an accurate translation?

If NGENF has wonderful results, it will fly this year. But if it has mild promising effects in only a few patients, it could decline to $1 and change. It won’t go to zero. I like the open label extension, whereby placebo patients who probably all had no results may be given the active agent to see if they get results. Frankly, I prefer the open label trial to double blind placebo controlled trials. Open label is more like real life where if X doesn’t work you try Y. Double blind trials to me are pseudoscience which is not the way things go in the real world. The protocols will be modified for humans based on these early results. Effects were seen in rats after 2-3 weeks. Who knows how long humans need treatment. Same for therapeutic doses for humans. Jerry Silver is brilliant, but extrapolation from rats to humans is always difficult.

I don’t expect success for ACXP this year, but I am holding in case things happen faster than I expect. ACHV may get FDA approval soon with the requirement that ACHV does postmarketing monitoring of side effects. The drug is already being sold in the rest of the world, with good safety. ACHV is probably a payoff the earliest of these stocks. Just don’t overpay.

Sorry, I didn’t update myself on ACHV. A PR 4 days ago said the FDA and the company agreed on the open label extension. This will monitor side effects on patients who already did trials. But it will take a full year, and approval might not be for 1.5 years. I am very disappointed that the FDA didn’t merely require post approval monitoring for side effects. That was the bullish case for soon this year. But no more. FDA is an obstructionist regulatory entity that requires companies to re-invent the wheel each step of the way. A few months ago, some ymb poster said not to buy ACHV before the inevitable dilution. I wanted to wait until the stock went down to the low $3 range, but Chris advised getting in because of the extraordinary value of the approved drug. I agree with the value. However, Chris has one thing in common with MM–both set target prices based on market potential of the approved drug. But in the meanwhile, for possibly several years, there are inevitable risks with FDA nonsense and the need for dilutions to keep a company alive for years without revenue. ACHV has EPS of negative $2. The market cap now is $93 million. They are doing a $124 million capital raise from $60 million of stock and the rest from exercised warrants. HUGE dilution. The stock could plunge to $2 before FDA approval. I am optimistic about FDA approval in 2025. The stock bounced from $4 a few days before the FDA news to $4.45 or so today. I’m surprised the stock didn’t sell off on this disappointing news of the FDA and the capital raise.

Chris, do you suggest selling ACHV now, and re-entering at much lower prices at least a year from now?

I was also surprised when ACHV went up.Had bought some in low 3’s. Sold some calls along the way. Sold in high 4’s. When I saw the news thought i could get some in low 3’s again. On to ACXP.Somewhere along the way I read 0% chance they do phase 3 on their own.Don’t know if thats true or not. But if it is true when would be perfect time. Late April phase 3 will be laid out. I think May or June would be perfect time to partner up or buy out. If it doesn’t happen then it will be a year latter. And stock will definitely trade much lower. From what Iv’e read he’s sold companies with far less data. I know he wants to sell but can he do it? He said at one time he thought he had spoken to the buyer. We can’t know what happens in private meetings with CEO’s.Is he just a dreamer? Maybe…Your like the voice of reason sometimes though. But were all gambling.Buy AAPL tomorrow at 175,,blue chip.If it goes to 170 it probably goes lower.

ACHV–On stockscan.io, tonight someone said that recently the estimate for another trial was $20 million. Why is $124 million needed? The open label extension is nothing that complicated–just monitor some of the patients already in the previous trials. This is the FDA obstructing progress and wasting time for ACHV. The drug is used safely in many countries.

ACXP–I don’t like the glibness of CEO Luci. “I have already spoken to the partner”–horsecrap. “To fund the phase 3 is just a nip and a tuck.”–evasive, euphemistic BS language. Maybe the partner is waiting on the slow moving FDA. All roads of corruption lead back to the FDA.

Chris, what now with ACHV? Sell and re-enter in a year? Before this news, it was $4 to 20, now maybe $2 to 10? More likely to only $5.

ACHV–Also, there were about 22 million shares outstanding prior to the capital raise. 13 million shares purchased at $4.50 represents 60% more shares. Future warrants of 13 million shares exercisable at $4.90 is another 13 million shares. The only good aspect is ACHV got high share prices which enables less dilution than otherwise, but it is still massive dilution. It is confusing why they are raising $124 million when all they project is $20 million for the trial. Perhaps the remaining $104 million is for commercialization in case no BP partner shows up. The bad news is that FDA approval won’t occur until first half of 2026, over 2 years from now. This is a complicated set of data collection, so it could take longer than that.

Chris?

ACHV–I am surprised the stock hasn’t plunged from at least the 40% dilution from the 13 million extra shares. Perhaps the near guaranteed EVENTUAL approval is supporting the stock. This action is basically FOMO (fear of missing out). Also, there is more confidence now that the company is well funded for the trial and future marketing. Approval is anticipated a long 2.3 years from now (1st half of 2026), but it could be longer if the picky FDA criticizes the data collection from the open label side effects study. But I still say that the target price should be reduced by the dilution factor which could be 63% (22/35) of the prior price target based on 13 million extra shares, or only 46% (22/48) based on 26 million extra shares. Perhaps the market will acknowledge this in a month or more, and shares will decline accordingly. I suppose the safest strategy would be to hold now and buy more on declines over the next 1-2 years. A more profitable but gutsy strategy would be to sell now and re-enter in 1-2 years. Selling call options could capture more $ at the risk of losing the stock position for the eventual payoff.

Rick Taylor, what’s your strategy for re-entering?

Chris? Thanks for your time.

ACHV-I like your gutsy strategy. i’m just watching for now. I can’t understand what’s propping it up. Buy out rummer, maybe.I think you can buy in low 3’s sometime in the year. It was trading there in December under better circumstances.

I think your strategy is best–re-enter in the low 3’s. I made a case for buying even at $2.00 because of the extreme dilution. Trading volume is low, and the stock is at best dead money for the next 2 years. On the other hand, since the dilution news, the stock has gone up slightly as if nobody else is concerned and they are looking forward to 2026. Prior to the dilution announcement, I was hoping for a much earlier approval with the need for postmarketing safety monitoring. The average price target of $20+ seemed based on that scenario, but now we have to wait 2 more years, so the target should be about $10, accounting for dilution. If I just hold, that still is a reasonable return for a 2+ year wait. But you may be smarter to re-enter much lower than the present $4.40, for a much better eventual return.

Chris?

My humor is getting warped by this BS of the underachieving Achieve. When I get stressed out, I make spelling mistakes. You meant to write “rumor” instead of “rummer.” In ancient times, body “humors” were analogous to today’s terminology, “hormones.” I remember the Good Humor ice cream truck as a child. I hope this fun free associating helps you to remember the correct spelling, haha.

Thank you. I was always better at math than english. After I posted all I could think about was how funny rumor looked. I’m probably wrong on ACHV. I just think there’s a better place to put your money until it corrects. I just don’t understand it. It should have crashed.Some time I feel like if I sell a stock you should buy it and vice versa. I think you know my plan. But timing is everything. I finally convinced my wife to invest 10000 dollars of her 50000 dollar roth ira account in ACXP. Plan being if it goes up 7 times to 70000 dollars, then if lucky enough to get NGENF at 2.50 and it goes to a 100 would be 40 times. 2.8 million. It probably won’t work. Luci has to find a buyer in May or June. If not it moves it back a full year. I know I.m dreamer.We call my wife the dream crusher.HaHA. Buy price is important though. If NGENF could be bought for 2.00 it would go up 50 times. Funny thing, I tried to buy NGENF at 1.20 in my merrill account. They won’t allow it. Then it went to 2.50 and fell back to 1.75. Called up broker with roth account and he bought 8000 dollars for me. Filled the rest with ACXP.. Then rolled a standard ira to roth. I will have tax to pay on that. Put half and half in ACXP and NGENF. NGENF was trading at 2.70 so put a limit at 2.25. A week later got a call half order was filled. It only went down to 2.25.Asked if I wanted them to go up 2 cents to try fill it. I said yes and they filled it all. Enough of my ranting.Please excuse any misspelling.

I was always better in math than in English, too. Funny thing, I had a chemistry teacher in HS who said that English is the most important subject. We would ask “Why” does the chemical reaction work that way? He said it is proper to ask “how” but invalid to ask “why” because “why” is a philosophical question. I will always remember his precision in many areas.

Unfortunately, timing of stock trading is even more speculative than the stocks themselves. It is best to buy a basket of a few stocks, or individually when the time is right for each.

ACXP–if Luci found a buyer as early as June, the BO price would be much lower than after the phase 3 gets done and reported. For a BP that invests objectively and prudently, how much can they offer based on 100% sustained cure in only 5 patients so far for Ibeza and the same 100% in only 7 patients on Vanco? The microbiome theory seems valid, but real comparative trials with large numbers of patients will have to be done to get any worthwhile BO price for ACXP investors.

NGENF–although the opportunity is exciting for patients and shareholders, a good rumor is what advanced the stock from the low $1’s to now $2.40. That assumes at least a minor benefit in 1 patient so far. If the final result is still lukewarm, the stock could decline to $1.50 or lower. I was able to get a few shares last year at $1.75. Although the payoff 10 years from now may be $100, there will be heart ache and financial stress for investors meanwhile if results are lukewarm.

JGMD – is there a PDUFA date for ACHV? Why do you think they could get FDA approval soon, and how soon?

They have to do that ridiculous data collection from hundreds of past patients, with complicated rules imposed by the FDA. My head is spinning from confusion. They project completion of the study in 2025, with submission of the application later, anticipated approval in 1st half of 2026. So if they do precisely everything the FDA wants, you could think of the PDUFA date as mid 2026. They will eventually get approval, but not soon.

Correction–the patent is extended to 2042.

That’s the TGTX Briumvi patent extension to 2042.

Europe took a big bite out of APPL. So lucky I sold at $199. Maybe MM’s price of $150 will get there?

Read the 4th qtr release from NVTA and square it with filing for bankruptcy… https://ir.invitae.com/news-and-events/press-releases/press-release-details/2024/Invitae-Reports-Estimated-Unaudited-Fourth-Quarter-and-Full-Year-2023-Financial-Results/default.aspx

Just listened to the latest update from ACHV. In case you are interested, here are my thoughts:

Their drug works in a 6 week trial and even better in a 12 week trial (which is the standard) outperforms everything out there by a wide margin in effectiveness plus has a very healthy side effects profile

In December they announced the surprise from the FDA that the FDA wanted to see data on longer term use as quitters often make several attempts.

Since that announcement, none of their suitors has lost interest. To the contrary. they have even more suitors! Their recent cash raise has eliminated any concerns about money and has boosted share price.

What the FDA will require before they submit their NDA in the first half of 2025. Last year ACHV thought their NDA would be filed Q2’24. Now they say H1’25. That gave me pause as to whether to stay invested.

When ACHV has data on 100 users who have been exposed to their drug for a cumulative 26 weeks, they can file their NDA. After that they will have to add data for another 200 w/12 months of exposure (this will be done after the NDA is filed and added to the application). Sounds like a big lift, BUT ACHV already has data on 1700 people who have 6 to 12 weeks of exposure so they can go back to them and just add another 14 to 20 weeks to get the 100 subjects with 6 mos. exposure and an additional 6 mos for the rest. I think approval in Q1 or Q2 of 2026 is all but guaranteed.

Do I think you will have an opportunity to buy it lower? Yes.

Am I selling now to take advantage of that belief? No.

I am sure the shares will be several times higher on approval.

I haven’t mentioned this but my holding in ACHV is not nearly as big as in ACXP or NGENF. A deal with Big Pharma could be announced at any time. Because of that, I will hold what I have and add as price drops, And maybe sell some puts.

Thanks. I also am optimistic about ACHV approval in 2026. But, what about the massive dilution from the additional 13 or even 26 million additional shares issued? On ymb, I posted tonight in response to Matt who spoke with IR. I was surprised that the stock price has been stable since the capital raise announcement a week ago. Do you think the unchanged average target price of $23 reflects the share dilution? It was obvious months ago that there would be a capital raise, and one ymb poster said to wait until that happened before buying. However, if the target price of $23 needs to be corrected for the dilution factor, the revised target would be $14 for the additional 13 million shares, or $10-11 for the additional 26 million shares. What do you think about the dilution question?

ACXP–Luci is moving at a snail’s pace. Phase 3 will have to be done before we get a good BO price, due to the tiny number of Ibeza cases so far, and the fact that Vanco did much better than its historical record due to the small numbers. A 2024 deal with BP will be positive, but a buyout price will be nowhere near what it would be after phase 3. Optimally a deal gets done just to get phase 3 expedited. This is also another 2 year situation like ACHV. What do you think?

NGENF–I want to buy more way under $2. Over $2 still discounts a mild benefit from the drug, since it is double the low $1 price before the rumor of results in probably only 1 patient. Today’s plunge to $2.25 is a retest of that level. We have until late Sept to buy more. It is still a speculation on whether the results are fabulous or merely promising.

Selling puts gets a cheaper buy price. Ideally, still wait until the price drops, and at that time sell the puts.

New World Investor for 3.7.24 is posted.