Dear New World Investor:

Stocks hit new highs as Chairman Powell told Congress the central bank is in no hurry to ease policy, though he said rate cuts are likely to come this year. I’m still doubtful, although I think a mild recession will start this year. It takes the National Bureau of Economic Research about a year after a recession starts to call it. That delay will give the Fed enough cover to not cut unless the recession spirals into something much bigger than I’m expecting.

The labor markets are slowly weakening. January’s Job Openings and Labor Turnover Survey (JOLTS) showed 5.7 million hires were made in the month, a slight decrease from the 5.8 million in December. There were 8.86 million jobs open at the end of January, another slight decrease from the 8.89 million job openings in December, and the lowest level since March 2021. The quits rate, a sign of confidence among workers, slipped slightly to 2.1%, down from 2.2% in December and the lowest level since August 2020.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

The ISM reports agree that employment has weakened notably in the last five months. The chart below shows the average of the employment sub-component for the ISM Manufacturing and ISM Services Index. The chart is smoothed by four months to reduce the choppiness

Click for larger graphic h/t @EPBResearch

Click for larger graphic h/t @EPBResearch

Tomorrow, the Bureau of Labor Statistics (BLS) will announce February payrolls. The big question is whether payrolls will match the 333,000 nonfarm jobs created in December and the 353,000 in January. The job market, although slowing, is still pretty strong, but it’s not that strong. I expect February payroll growth moderated to about +185,000, below the +200,000 consensus estimate, while the unemployment rate remained at 3.7%.

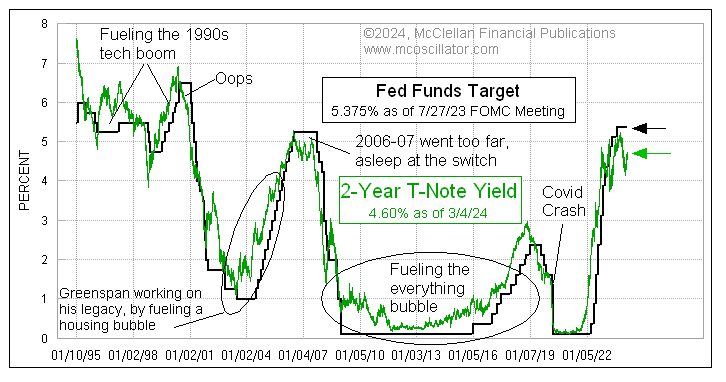

What will the Fed do? Torsten Sløk, Apollo Global’s chief economist, became one of first Wall Streeter’s to join me in saying “rates are going to stay higher for longer.” He even predicts the Fed will not cut rates this year. I think it’s too early to make that call, as I still believe a recession is imminent and the Fed probably will make tiny cuts in response.

If you want to know what the Fed will do next, you could try to guess what their 400 PhDs will advise them to do based on their complex economic models. Or you could just do what I do and follow the 2-year Treasury note.

Click for larger graphic lg @McClellanOsc

Click for larger graphic lg @McClellanOsc

Market Outlook

The S&P 500 added 1.2% since last Thursday to new all-time highs today as breadth improved and the percentage of stocks in the Index setting new 52-week highs surpassed the December peak. The S&P is up 8.1% year-to-date.

Since 1957, the S&P 500 has returned more than 20% over a four-month time frame only 14 other times, with the last coming in the summer of 2020. Twelve of those other 14 occurrences saw double-digit returns over the next 12 months, with the lowest return being a positive 1.16%.

In years after the S&P gained in both January and February, the final 10 months of the year were higher 26 out of 28 time. The next 12 months were higher an amazing 27 out of 28 times, with the returns in both cases much better than the average returns.

Click for larger graphic h/t Carson Group

Click for larger graphic h/t Carson Group

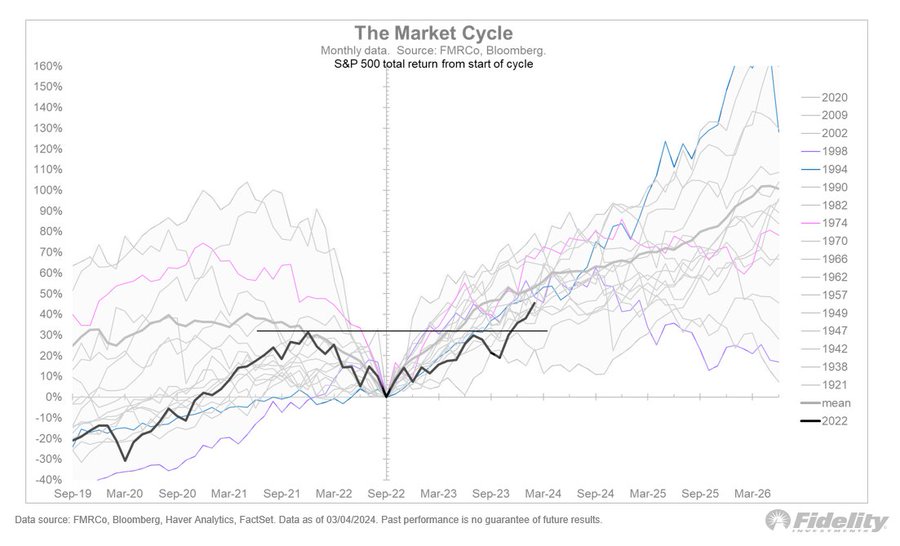

Looking at historical bull market analogs, we can see that after a slow start in 2023, the S&P 500 has now entered the zone of a typical bull market.

Click for larger graphic h/t @TimmerFidelity

Click for larger graphic h/t @TimmerFidelity

The Nasdaq Composite gained 1.1%, setting a new intraday high today. It is up 8.4% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) only added 0.4% as the biotech rally took a breather. It is up 10.6% year-to-date. The small-cap Russell 2000 booked a 1.5% gain and is up 2.8% in 2024.

The fractal dimension is ridiculously overextended, but I said that last week.

I’m going to have to expand the graphic to properly record both the S&P highs and the fractal lows.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model forecast for March quarter real GDP growth is down to +2.5%, a level the Blue Chip economists are rapidly approaching.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, March 8

February payrolls – 8:30am – +200,000 expected; January was +353,000

Sunday, March 10

Daylight Savings Time – 2:00am local time

“Spring forward; Fall backward”

Monday, March 11

Short Interest – After the close

Tuesday, March 12

NVTA – Invitae – Through 3/14 – ACMG Clinical Genetics Meeting

Consumer Price Index – 8:30am

GILD – Gilead – 10:00am – Leerink Global Biopharma Conference

Wednesday, March 13

GILD – Gilead – 11:15am – Barclays Global Healthcare Conference

Thursday, March 14

ENVX – Enovix – 8:30am – J.P. Morgan Industrials Conference

PD – PagerDuty – 5:00pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $169.00) had its third consecutive weekly close below its 200-day moving average and closed at its lowest price since early November. We may get a chance under $150 yet, but we’ll have to buy before the AI reveal at June’s Worldwide Developer’s Conference.

It’s lagging as the Magnificent7 stocks have stopped trading as a pack and instead show dispersion:

Nvidia +66.1%

Meta +41.9%

Amazon +17.3%

Microsoft +10.5%

Alphabet -2.0%

Apple -6.7%

Tesla -18.5%

The stock dropped after news broke that iPhone sales in China fell 24% in the first six weeks of 2024. The Chinese government is just starting a huge monetary and fiscal stimulus to get consumers spending again, and I expect iPhone sales to improve going forward, but the big unit growth opportunity has shifted to India.

Goldman Sachs removed the stock from its benchmark “Conviction Buy List – Directors Cut” but kept their Buy rating in place. They cited “reduced iPhone unit demand from a lengthening replacement cycle and reduced consumer demand for the PC & tablet category.” Both of those issues, the bank said, would “more than offset…Apple’s installed-base growth, secular growth in services, and new-product innovation.”

Yeah, right. I suspect Goldman’s sales force wrote lots of Sell tickets where the buyer was – surprise – another preferred Goldman customer. That’s the way the game is played – shake the tree, pick up as many apples as you can, and run through the hole in the fence to sell them to the highest bidder. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $32.60) presented at the Morgan Stanley Technology, Media & Telecom Conference (TRANSCRIPT HERE). The CFO said revenues are about 30% below trend line, which actually means about a 40% increase from the current level of sales when they get back to that trend line – and they will – with no increase in operating expenses. Corning is in the early stages of an earnings explosion.

Their goal for net income as a percentage of sales is 25% to 30%. They can raise the price of glass because it is less than 10% of the cost of a TV.

ICE vehicles in Europe and in China, including hybrids, have to add a gas particulate filter. That will be required in the US in 2026, which takes Corning from roughly a $15 a car opportunity to more like a $45 per car opportunity. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences‘ (GILD – $73.66) CFO presented at the TD Cowen Healthcare Conference (TRANSCRIPT HERE). She said they expect to grow the HIV business at 5% a year due to the rapid growth in prevention.

On top of that, they have a $2 billion cell therapy oncology business, where they are clearly the global leader in hematological cancers. Trodelvy, their antibody drug conjugate, is a $1 billion product and also growing double digits. Both of the cell therapy franchises and the HIV drugs have a very long product life cycle with no major patent cliffs for a decade.

In HIV, their first Phase 3 trial of every six-month subcutaneous lenacapavir for HIV prevention will report data in the second half of this year. This is a big one for Gilead, Their current prevention drugs, Descovy and Truvada, are oral. They are 99+% effective in preventing HIV infection if taken every day, but people at risk of getting HIV don’t tend to take the pills every day. In fact, many people on PrEP today take the pills intermittently or on demand. A twice-a-year jab would make a big difference in the real world. The second Phase 3 trial data will come early in 2025. Lenacapavir could be as big as Biktarvy, their treatment for HIV infections that brings in $12 billion a year.

They expect oncology to be one-third of revenues through the end of this decade. The US is using cell therapy drugs about half as much as Europe, mostly because in the US they are used in academic settings but not yet in community settings. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $512.19) presented at the Morgan Stanley Technology, Media & Telecom Conference (AUDIO HERE). Tom Allison, the head of Facebook who also oversees development and strategy across most of Meta’s divisions, said they are very focused on using AI to make Facebook more relative to Gen Z and younger users. Video, Reels, and AI-enhanced are key programs. META is a Buy under $345 for a $400 target in 2024.

SoftBank (SFTBY – $30.79) issued $3.7 billion of a seven-year unsecured corporate bond with – get this – an interest rate of 3.04% per annum. That tells you all you need to know about SFTBY’s creditworthiness. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Fastly (FSLY – $13.50) CFO presented at both the Raymond James Institutional Investor Conference (TRANSCRIPT HERE) and the Morgan Stanley Technology, Media & Telecom Conference (TRANSCRIPT HERE). They said as they look forward increasing scale gives them the ability to further improve their margin profile in the small markets and also reduce some of the variability in revenue in these markets. But they gave conservative guidance that basically assumed no improvement.

The single biggest driver of Fastly’s revenue growth is new customer acquisitions. In the fourth quarter for enterprise customers, those that generate over $100,000 or more per year, they booked 31 new customers. That was the highest number of new enterprise customers in a quarter in over three years. In the first year, new customers typically contribute less than 10% of Fastly’s revenue. But their first year to second year revenue growth is over 100%, and they continue to grow meaningfully in year two and year three.

The stock declined sharply after the December quarter conference call because the had a $1.5 million revenue miss that caused them to guide too conservatively for 2024. I think they will beat their guidance every quarter this year. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $24.34) reports January quarter earnings next Thursday after the close. Analysts expect revenues up 9.3% to $110.4 million with earnings nearly doubling to 15¢ per share. Guidance should be for April quarter revenues of $113.4 million with 18¢ a share. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $16.96) took a while, but lift off is here.

QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics‘s (ABCL- $4.91) CFO presented at the TD Cowen Health Care Conference (AUDIO HERE). They’ve signed about 200 partnership contracts to develop antibodies in return for an upfront fee and downstream royalties. 90% of the value is in the royalties, so they are very picky about which deals they make. Royalties used to average 2.5% and now average 4.3%. At this point they have completed 100 of them and handed over the antibodies to the partners for development. Thirteen are in human clinical trials.

They also do some hybrid co-development programs where they and the partner have 50/50 ownership, with the option to pay 50% of the development expenses to maintain their share. Expect more deals this year.

They also look at very difficult targets in the public domain to develop their internal antibody programs. The first two are in IND-enabling studies that will enter the clinic in early 2025. At least one more candidate will enter IND-enabling studies this year, and maybe two. Expect another one or two a year every year. The government of Canada is paying 50% of the development expenses through Phase 1 for 17 programs. Then they will be partnered out.

In 2020 the Canadian government agreed to fund half of the $180 million cost of building a GMP facility to manufacture antibodies for partners and internal programs. This is very attractive to small biotech companies as their only alternative now is to go to China. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Compass Pathways (CMPS – $11.28) was on an interesting neuropsych panel at the TD Cowen Healthcare Conference (AUDIO HERE), There was no new info on Compass – they can’t say anything much about the Phase 3 trials. But it’s worth a listen to get a feel for how other companies – almost sounding like partners instead of competitors – are doing. This is going to be a HUGE area of medicine, and Compass will be one of or maybe the leader. CMPS is a Buy under $20 and put it away for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inovio (INO – $9.03) reported a December quarter loss of $1.10 per share, beating the estimate for a $1.24 loss. On the conference call (AUDIO HERE and TRANSCRIPT HERE), management said they have prioritized the product pipeline to focus on INO-3107 and other late-stage assets that have both a high unmet medical need and strong commercial potential. Their commitment to financial discipline resulted in cutting operating expenses nearly in half in 2023 compared to 2022.

In 2024 they will start the confirmatory trial for INO-3107 in the second half and submit the Biologics Licensing Application under the FDA’s accelerated approval program by the end of the year. They are preparing for a 2025 launch. For the immuno-oncology candidates, they will finalize the trial design for evaluation of INO-3112 in combination with Coherus BioSciences’ LOQTORZI in patients with throat cancer.

With their partner Regeneron, they’ll also determine the next steps for INO-5401 in glioblastoma, a deadly form of brain cancer.

They also expect some key milestones for the infectious disease candidates. One is discussions in the first half of 2024 with collaborators and potential partners around development plans for INO-4201 as an Ebola booster vaccine. They recently received feedback from the FDA and identified a potential development pathway.

Another is a readout of the first clinical data from the Phase 1 trial evaluating the anti-SARS-CoV-2 dMAbs candidates in the second half of 2024.

They finished the year with $145.3 million in cash, enough to carry them into the June 2025 quarter. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

Invitae (NVTAQ – $0.02) reported December revenues up 4% from last year to $127.8 million. After adjusting for $10.5 million in revenues from discontinued businesses in last year’s quarter, revenues grew 14%. They booked a $74.1 million GAAP gross profit, up 150% from last year, with a gross profit margin of 58.0%.

They burned $57.6 million in cash and ended the year with $209.0 million. The bankruptcy auction is April 17, and while most bankruptcies wipe out the value of the equity, I think there’s a good chance the winner will either offer 5¢ to 10¢ a share or, better yet, 5% to 10% of the new company. We’ll know soon. Hold NVTAQ.

Primary Risk: Current shareholders don’t own any of the restructured company.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Mid-2024.

Medicenna (MDNAF – $0.84) will present an update from the Phase 1/2 ABILITY-1 trial of MDNA11 at the American Association for Cancer Research (AACR) annual meeting on April 9. It will include anti-tumor activity, safety, pharmacokinetic, and pharmacodynamic data. MDNA11 is the only long-acting, “beta-enhanced not-alpha” interleukin-2 (IL-2) super-agonist in clinical development. In addition, pre-clinical data for MDNA113, their novel first-in-class tumor-targeted and tumor-activated bi-functional anti-PD1-IL-2 Superkine, will be presented at the conference. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

TG Therapeutics (TGTX – $18.00) presented preliminary data at the Americas Committee for Treatment and Research in Multiple Sclerosis (ACTRIMS) meeting from the ENHANCE Phase 3b trial evaluating patients who switch from prior CD20 therapy to Briumvi. Patients who switched to one-hour Briumvi had a manageable safety and tolerability profile. TG will present updated data from this trial throughout the year. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,167.40) hit the long-awaited all-time highs, including today, despite broad hatred in the US, a higher dollar, and tighter monetary policy expectations. That suggests the surge in demand is from abroad, particularly China. According to some insiders, everybody at this week’s PDAC (Prospectors & Developers Association of Canada) meeting seemed skeptical on this gold move. Gold is climbing a wall of worry. I love it! It’s especially positive that gold’s price is rising even as US ETF assets keep falling:

Click for larger graphic h/t @BobEUnlimited

Click for larger graphic h/t @BobEUnlimited

The fractal dimension is in perfect position, still with a full load of energy to push gold much higher IF it can break 55 this week. C’mon gold, you’ve been a heartbreaker so many times. Let’s do this!

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $67,075.62) also hit an all-time high, first in euros and then in dollars, briefly surpassing its previous record of $68,789 from November 2021. It had a sharp “sell the news” drop shortly after, plummeting 10% to trade around $62,000, and as promptly recovered. The 10 spot bitcoin ETFs have blown through $50 billion in assets, after beginning life seven weeks ago under $30 billion that was all in Grayscale’s Bitcoin Trust (GBTC). About $8 billion of the increase is from inflows. The rest is from bitcoin’s value going up. Less than two months in, they are more than halfway to passing gold ETFs.

When bitcoin has broken its all-time highs in the past, the price doubled very quickly immediately afterwards. Add in the halving in less than 50 days and it is hard to be bearish. Even Barron’s can’t be completely negative:

Click for larger graphic

Click for larger graphic

And JPMorgan predicted it will drop to $42,000 after the April halving because reasons. Oddly, they first said: “The bitcoin production cost has empirically acted as a lower bound for bitcoin prices.” OK, so what is the production cost? They estimate that post-halving production costs could double to about $53,000. OK. This could cause a 20% decline in the bitcoin network’s hashrate, meaning fewer miners would be competing to produce bitcoins simultaneously. OK. But where did $42,000 come from?

“This $42,000 estimate is also the level we envisage bitcoin prices drifting towards once bitcoin-halving-induced euphoria subsides after April.” Oh. So while diminishing supply has historically caused prices to soar, you guys think there is enough froth in the price to put enough downward pressure on bitcoin to overcome the new reality of a 50% cut in supply. Well, maybe. If bitcoin goes over $100,000 by the middle of April, I’ll probably want to step aside, too.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $35.63) bought 12,447 bitcoin just on Tuesday. That’s about 14x the daily new supply from all the miners. This presents a growth that will produce $1 billion dollars a day flowing into bitcoin just from BlackRock. If you owns even a fraction of bitcoin directly in your wallet or in IBIT, they will make it more valuable each day. Demand rules.

Click for larger graphic h/t @BrianRoemmele

Click for larger graphic h/t @BrianRoemmele

IBIT’s expense ratio is competitive with the fees for trading bitcoin, so it is a good option to keep your overall costs low while making it easy to trade from your existing online broker. IBIT is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $79.46

OPEC+ agreed to extend voluntary production cuts of 2.2 million barrels a day through the June quarter. I expect them to extend quarter by quarter as long as oil is under $85. Saudi Aramco just increased its Arab Light premium for Asia to +$1.70 for April. Expectation was for no increase.

And there it is! The year-over-year surplus in product storage is gone. Thanks to the large draws in gasoline (-4.5 million barrels) and distillate (-4.1 million barrels), product storage is now in line with 2023. US refinery throughput is finally starting to move up after a long period of low utilization, so if product draws continue with a flat crude storage outlook, then not only will oil hold the $79 to $80 range, but I expect it to move closer to $85 by mid-April.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Crude storage has peaked around 450 million barrels. US oil production is stagnating around 13.2 million barrels a day, so we should see US crude storage in the low-400 million barrels over the summer.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Wood Mackenzie, the highly respected energy research company. said global oil demand will grow by 1.9 million barrels per day (bpd) this year, a forecast close to OPEC’s estimate of 2.25 million bpd. Most of the increase will come from China and India. A wide-ranging Reuters survey showed most analysts expect global oil demand to grow by somewhere between 1.0 million and 1.5 million bpd in 2024.

Wood Mackenzie’s prediction for demand growth in 2025 is 1.4 million bpd. OPEC expects growth of 1.85 million bpd in 2025.

The July 2026 Crude Oil Futures (CLN26.NYM – $67.56) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.80) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.27) reported December quarter revenues down 37.9% from last year to C$522.97. Production increased 6% from the September quarter to average 87,597 barrels of oil equivalent per day (boe/d), comprised of 54,216 boe/d from North American assets and 33,381 boe/d from International assets. International production benefited from a full quarter of production from Australia and Ireland following maintenance downtime in the prior quarter, as well as increased production in the Netherlands due to new production from their 2023 drilling program.

They generated $372 million of funds from operations (FFO), up 38% from the September period, and $229 million of free cash flow (FCF), up 59% from Q3. Net debt decreased during the quarter by $164 million to $1.1 billion, the lowest level in a decade and a 50% reduction from the peak in 2020. In addition, they returned $45 million to shareholders, comprised of $16 million of dividends and $29 million of share buybacks.

It was a very good year:

Click for larger graphic

On this morning’s conference call (SLIDES HERE and TRANSCRIPT HERE), management said they achieved the midpoint of their annual production guidance of 84,000 despite wildfire-related downtime in Western Canada and unplanned maintenance downtime in Australia. Their ability to meet the annual production guidance despite these issues shows the strategic advantage of operating a diverse portfolio as they reallocated capital to offset the production impacts in Canada and Australia.

They have bought back 1.4 million shares so far and are increasing the pace of buybacks as long as the stock is this cheap. This is a major reason you want to be on board. They are forecasting annual Funds From Operations around $1.25 billion with Free Cash Flow around $650 million. So they expect to return about $250 million to shareholders through dividends and share buybacks of 10% of the market cap, all while continuing to reduce debt.

Their 2024 guidance is for a midpoint of 84,000 boe/d production.

Click for larger graphic

VET is a buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

EQT (EQT – $37.26) joined the party, announcing a strategic production cut of one billion cubic feet (Bcf) per day “in response to the current low natural gas price environment resulting from warm winter weather and consequent elevated storage inventories.” They will continue this through March, taking 30 Bcf to 40 Bcf out of first quarter production.

This plus Chesapeake Energy’s 0.73 Bcf/day cut last week and other cuts flipped total US natural gas production of about 101 Bcf per day to less than demand.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The production cut came out of necessity as storage is expected to exit this winter 550 Bcf above the five-year average.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The next question is how producers reacts to recovering prices. If prices rally too quickly it could prompt them to increase production again. By July, the Henry Hub futures curve put prices around $2.569/MMBtu. I don’t think Lower 48 gas production will see any production decline if prices are that high – so they won’t be. “The cure for low prices is low prices.” EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $6.41) and other owners of left-for-dead uranium mines are restarting operations to capitalize on rising demand for U308, but it will take years to restart most of them. The International Atomic Energy Agency estimates the world will need more than 100,000 metric tons of uranium per year by 2040 — an amount that requires nearly doubling mining and processing from current levels.

About 10 uranium firms were at PDAC, including Energy Fuels:

UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $39.81) will benefit for many years as the copper supply/demand imbalance grows:

Click for larger graphic h/t sprott.com/insights/copper-wired-for-the-future

China is launching a year-long program to boost domestic consumption – Quantitative Easing on steroids. Here comes $5 copper! FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $0.20) would shoot up if Senator Elizabeth Warren gets her way. This morning in a video post on X she said: “It’s time to legalize marijuana nationwide.”

This echoes what she said in a January 29 letter to Attorney General Merrick Garland and DEA Administrator Anne Milgram, where she urged the DEA to “swiftly deschedule marijuana from the Controlled Substances Act.”

ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

RIP Roni Stoneman

* * * * *

Your keeping an eye on Vitalia Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 3/7/24. Check out the complete Portfolio page HERE.

Portfolio Protection

April 30 SPY $505 put (SPY240430P00505000 – $4.72)

April 30 SPY $410 put (SPY240430P00410000 – $0.26)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $169.00) – Buy under $150 for new iPhones

Corning (GLW – $32.60) – Buy under $33, target price $60

Gilead Sciences (GILD – $73.66) – Buy under $80, target price $120

Meta (META – $512.19) – Buy under $345, target price $400

SoftBank (SFTBY – $30.79) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.30) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.84) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $13.50) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $24.34) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $16.96) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.43) – Buy under $13, target price $30+

Velo3D (VLD – $0.29) – Buy under $6, target price $50

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $4.91) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.46) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.68) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $11.28) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $9.03) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.84) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.69) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $18.00) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($24.58) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.84) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $30.08) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $19.84) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.40) – Buy under $30, target price $50

Coeur Mining (CDE – $3.19) – Buy under $5, target price $20

First Majestic Mining (AG – $5.31) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.35) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.69) – Buy under $10, target price $25

Sprott Inc. (SII – $37.08) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $67,075.62) – Buy

iShares Bitcoin Trust (IBIT – $35.63) – Buy

Ethereum (ETH-USD – $3,876.62) – Buy

Grayscale Ethereum Trust (ETHE – $33.86) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.56) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.80) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.27) – Buy under $11; $24 target

EQT (EQT – $37.26) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.41) – Buy under $8; $30 target

Freeport McMoRan (FCX – $39.81) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.28) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.14) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.20) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $24.91) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.20) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.05) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.90) – Hold for buyout

Invitae (NVTAQ – $0.02) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

I believe the FED will cut 3 times this year starting by June at the latest.

If they don’t they risk a lot more than a mild recession. I work for growing Cali City development department, we are slow as it’s been in decade. Not just slow, but very slow. Target and other retail biz with declining sales, we are already headed for a recession.

MM – do you expect MDNAF’s April 9th data release to be a significant share price catalyst? Would you recommend buying before April 9th?

MM please reply to the multiple questions

MM – so do you believe there will be a pullback in BTC prior to the big run or should we not wait and go all in now? I’m reading that Ethereum (ETHE) and Solana will be the bigger winners as the expectation for Ethereum to be the next ETF approval, and then Solana after will drive speculative buying and price action – thoughts?

I like and hold ETHE as well. My position has ballooned up to 21k.(in both, mostly ETHE.

GRPH – LENZ Therapeutics and Graphite Bio Announce Merger Agreement

https://graphitebio.com/

Graphite Bio Declares Special Dividend In Connection with Proposed Merger with Lenz Therapeutics

https://ir.graphitebio.com/press-releases

I bought 144,000 shares of NVTAQ and 4612 ACRDF today. Just spinning the roulette wheel.

ALL ON RED….A better gamble might have been VLD. I think all the note holders in NVTA will get all the money. We’re all speculating,investing,gambling.

I have that one too!! It will be interesting to see how that shakes out.

VLD just announced ER date March 26. Final opportunity to load up before then. Shorts are trying to scalp cheap shares today on brief dips. The Bechtel news gave a nice advance from 25 to 37 cents. At 32-34 today, this is still above the Fibonacci pullback to 32. If this holds until March 26, we are off to the races soon after. Lazerator on YMB thinks all the bad news from Q4 2023 is already discounted at 25-30 cents. Of all the bottom fishing you have done, I think this is the best one. I am fully loaded, full disclosure.

Question for you jgmd,what does your gut tell you about scyx going forward,besides the pop that should happens once there issues are solved with the cross contamination,tx

SCYX yesterday briefly touched $1.50, close to an all-time low. The actual all-time low, $1.15 is invisible on a long time chart, and was probably a brief dip just over 1 year ago. I wrote several times over the past few months that the stock will keep declining until GSK solves the manufacturing problem. MM has estimated that it will be by June 30. I don’t see why it should take 9 months from Sept 30 when manufacturing was shut down. Troubleshooting at the plant is a relatively simple engineering problem, but the delay is likely due to the damn political obstructionist regulatory bureaucracy in getting FDA approval, plus the worldwide political crap induced supply chain problems in getting factory parts for machine modifications.

You’re right that there will be a pop in the stock when this gets resolved. Then MARIO trial for invasive candida infections gets done. There are other invasive C trials that has been already done, and we are awaiting data on that. Analyst price targets are at least $7.00. I don’t have any more insights than that.

MM?

Thanks for your input . Much appreciate your opinions. Looking to trade now.

MM–on SCYX, please review how you come up with price targets of $20, then $50. Thanks.

Why is it taking so long to solve the manufacturing problem?

MM – With regard to ENVX, I would appreciate you providing the highlights of the presentation made by their CFO at the JP Morgan Industrials Conference this morning. Among the topics of interest is whether or not there has been any slippage in their projected dates for key milestones. The significant drop in the stock price (to less than $8) in recent weeks would suggest that they may be encountering some unexpected problems/delays.

QUIK now at $ 18.10. My 1645 shares are up $10,546. Just FYI

My QUIK sordid history. First buy in 2012 at $35, then 2013 at $29, then 2016 at $16. Then much more in 2020 at $4. Average cost $12.68, a little more than your average cost. MORAL–never buy any NWI stock without positive earnings at the recommended buy price. ALWAYS wait several years to do bottom fishing. I am down 95% in APTO, but it may be getting close to bottom time, although we’d have to wait until about 2027 for trials to bear fruit.

New World Investor for 3.14.24 is posted.