Dear New World Investor:

On Tuesday, Fed Chairman Powell said inflation is coming down slower than he expected, so it’s “high – but not higher – for longer.” Wall Street did a decent job of panicking the weak hands into selling them some cheap stock as the CNN Fear & Greed Index plunged to its lowest level since November 3.

Click for larger graphic h/t @WinfieldSmart

But the bond market said: “Whut?” as the 2-year note yield rose a measly two basis points to 4.96% and the 10-yr note yield settled an equally disdainful three basis points higher at 4.66%. Everyone already is on board with the idea that the Fed will lower rates slowly and reluctantly. Wall Street knows a stronger-than-expected economy means stronger-than-expected earnings to support high valuations.

In fact, according to the latest BofA Fund Managers Survey, 36% of fund managers now believe the most likely outcome for the global economy is a “no landing” scenario. This was substantially higher than the 23% who saw the outcome a month ago, and the highest level seen since June 2023.

Jefferies wrote: “Recessions don’t hit the US economy without a catalyst of some sort, and we just don’t see what is going to stop consumer spending. With demand still solid, it is hard to see how inflation will continue to slow down, and thus it is hard to see how the Fed can cut rates.”

Click for larger graphic

54% of respondents still believe a soft landing – where economic growth slows but not to the point of recession, and inflation returns to its historical average – is the most likely outcome. My scenario – a brief, mild recession that takes inflation below 2% – isn’t even a choice.

I am looking at the collapse in the money supply in 2023 plus the employment data showing most new jobs are part-time workers (taking second and third jobs to survive, I suspect) to arrive at my mild recession forecast. If I’m wrong, the “no landing” scenario is the next most likely.

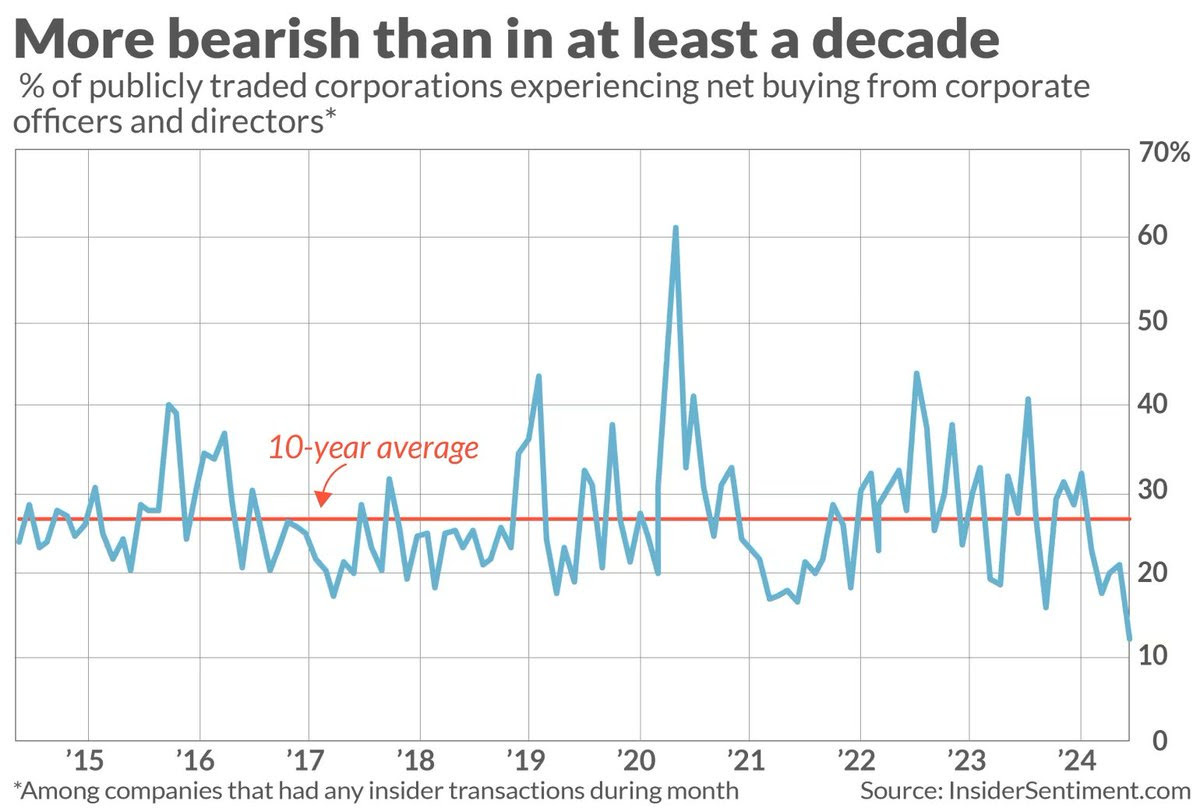

But retail investors still fear the Fed, and net stock buying by corporate insiders of publicly traded companies is the lowest in at least a decade. I think that’s just because these are the highest prices they’ve seen in a decade.

Click for larger graphic h/t @mayhem4markets

Market Outlook

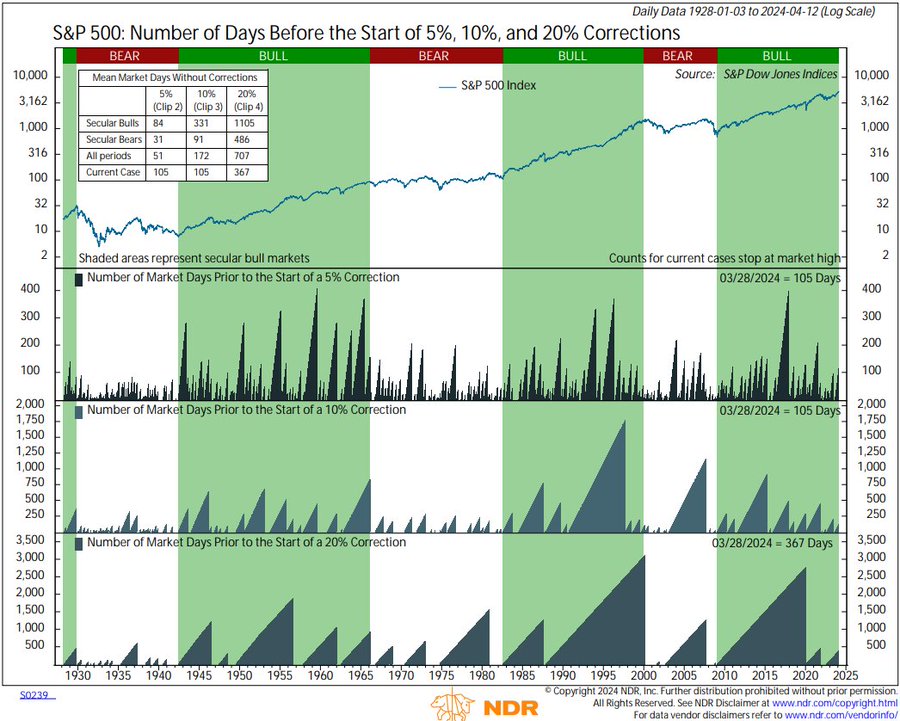

The S&P 500 lost 3.6% since last Thursday as weak hands panicked at “high for longer.” The Index now is only up 5.1% year-to-date. It has been 107 days since the last 5% correction in the S&P. Since 1928, during secular bull markets, 5% corrections occurred about every 84 days on average. It has also been 107 days since a 10% correction. 10% declines typically occurred every 331 days on average during secular bulls. The S&P 500 currently is off 4.82% from its all-time high on March 28 at 5264.85 h/t @NDR_Research.

Click for larger graphic h/t @DayHagan_Invest

The Nasdaq Composite lost 5.1% as Big Tech took more hits. Blow-out earnings from Netflix after the close today might offset some of that tomorrow. It is only up 3.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 8.5% as it was clobbered every day this week. It is now down 6.5% year-to-date. The small-cap Russell 2000 dropped 100 points or 4.9%, throwing it back to a 4.2% loss in 2024.

The fractal dimension indicates this correction has either a lot of time or a lot of points to go in order to consolidate the huge upturn from last October. Many recommendations may give us an entry point below the current buy limit, although not all (looking at you, META).

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model next-to-last estimate of March quarter real GDP growth ticked up from 2.8% to 2.9% due to a bit of strength in personal consumption expenditures and private domestic investment, The Blue Chip economists are estimating just over 2.0%, so we should see a slightly positive “surprise” on April 25.

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Tuesday, April 23

FCX- Freeport McMoRan – 10:00am – Earnings conference call

EQT- EQT – After the close – Earnings release; call tomorrow

Wednesday, April 24

EQT- EQT – 10:00am – Earnings conference call

Short Interest – After the close

META – Meta Platforms – 5:00pm – Earnings conference call

Thursday, April 25

March quarter GDP – 8:30am – First estimate

GILD – Gilead – 4:30pm – Earnings conference call

Friday, April 26

Personal Consumption Expenditures Index – 8:30am – The Fed’s favorite inflation measure

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $167.04) is down 13.1% this year due mostly to demand concerns in China, which are widely known. I resisted raising the buy limit until that worry was in the stock. What is not yet in the stock, but will be soon, is how far along Apple is in integrating AI into its devices. I expect major announcements on its progress with generative artificial intelligence at the Worldwide Developers Conference in June, followed by an AI-based iPhone 16 announcement in September.

Bloomberg reported that Apple will focus the next version of its M-family of processors, the M4, on artificial intelligence to boost Mac sales. The M4 is already nearing production and will eventually be put into every Mac, with announcements to come as soon as this year. Apple will give new iMacs, MacBook Pro, and Mac Minis the new chips. Market research firm IDC said Apple shipped 4.8 million Macs during the March quarter, up 14.6% year-over-year. It held 8.1% of the global PC market as of the end of March, up from 7.1% in the year-ago period.

Needham cut their estimates for the March quarter, citing weakness in the iPhone and China. They cut their revenue estimate 4% to $90.8 billion, and cut their earnings estimate 7% to $1.51per share. But the consensus already is at $90.78 billion and $1.51 – they are just getting in line with the rest of the Street. They kept their Buy rating and $220 target price.

Apple’s May 2 earnings announcement probably will be mildly disappointing, although Services revenue will set another new record. But the tip-off will be if the stock goes up over the following few days – that would set off a scramble to get back in. My first target is $225 to $250 by this time next year. AAPL is a Buy RIGHT NOW under $175 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $66.16) reports earnings next Thursday. The consensus is looking for $5.98 billion in sales and 37¢ earnings. I expect Gilead to beat substantially on the bottom line. June quarter guidance should be for $6.38 billion and $1.59. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $501.80) reports earnings next Wednesday. Analysts expect $34.00 billion in revenues and $4.06 earnings per share. Guidance should be for $36.03 billion and $4.47.

Truist expects Meta to beat the consensus estimates and raised their forecast from $36.12 billion in revenues to $36.54 billion. They raised their earnings estimate from $4.18 to $4.28. They also reiterated their Buy rating and raised their target price from $525 to $550. They wrote: “We’re raising our 1Q and FY24 estimates for META to reflect improving monetization after two years of compression, higher impression volume and a strengthened must-buy status within the digital ad ecosystem amid ongoing cookie deprecation and a volatile macro. Additionally, we believe Meta’s significant AI investments are yielding better ranking and recommendation results for users and advertisers, driving better outcomes for both.”

Truist pointed to data from Sensor Tower showing that Facebook led all social media platforms in year-over-year growth in time spent per daily average user during the first quarter at +3%. YouTube was next with +1%. TikTok declined 4%.

Citi said Meta isn’t really seeing any negative impact on users engagement due to rising advertising loads on its Reels video posts. META is a Citi top pick, and they boosted some projections and raised their target price. They said Instagram Reels, Meta’s short-video answer to TikTok, saw its ad load expand by 90 basis points from the December quarter to 20%, even as Instagram minutes per daily active user rose 4%. They wrote: “…with Meta’s newer ad innovations (Adv.+ Creative, Reminder Ads, longer form Reels, etc.), a new AI video architecture, and greater overall advertiser adoption, we believe advertiser demand for Reels (and Meta) continues to improve.”

Meanwhile, they said Reels are getting more commercial with 79% of Gen Z users purchasing a product after viewing a Reel. They now project 2025 revenue growth of 14% year-over-year, with pro forma earnings per share of $24.23, above the consensus expectations for $23.22. They raised their target price from $525 to $590.

Later this year, Meta will launch a new education product for Quest Augmented Reality headsets. It will allow teachers, trainers, and administrators to access a range of education-specific apps and features, and make it possible for them to manage multiple Quest devices at once. The new product is the result of extensive consultation and collaboration with educators, researchers and third-party developers working in the education space around the world. META is a Buy under $345 for a $400 target in 2024.

Small Tech

Enovix (ENVX – $6.01) has completed Factory Acceptance Testing for its Gen2 Agility Line in Malaysia and is on track to produce their first silicon battery samples for mobile and IoT customers from Fab2 in the June quarter.

Enovix’ patented manufacturing process uses dozens of machines to produce their battery cells with a unique architecture that enables the use of a 100% active silicon anode for higher energy density. CEO Raj Talluri said: “In just 100 days, the team built a world class factory.”

Raj is going to do a live Ask Me Anything on May 6 at 5:00pm EDT. The short sellers will be out in force! ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $12.38) was upgraded from Neutral to Overweight by Piper Sandler. They wrote: “Fastly is gaining share in the core CDN [Content Delivery Network] market, largely with Media delivery exposure, with inputs like our CDN Tracker suggesting gains are continuing. There are multiple confidence drivers in the sustainability of Fastly’s CDN business, including the favorable competitive landscape, OTT [Over The Top or streaming] metrics stabilizing, and new packaging.”

FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $3.55) will launch two satellites into two completely different orbits for their 47th mission on April 24. One satellite will be at a 520 kilometer low Earth orbit and the other at a 1,000 kilometer low Earth orbit. Only SpaceX or Rocket Lab could pull off a difficult mission like this. You can read the details HERE. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $3.91) CFO gave an excellent presentation at the Bloom Burton Healthcare Conference in Toronto (AUDIO HERE).

He said they believe it’s easy to build an extremely successful biotech company – just develop a blockbuster drug, And there are two ways to do that. One is to have a unique insight into biology that turns out to be right. The second is to partner with people who have those unique insights but have not been able to develop a molecule to test them. That makes it a technology problem, not a biology problem – and that is the path AbCellera is taking.

Drug development is too costly, takes too long, and fails too often. AbCellera developed technology to target all three of those problems and has been able to sign numerous partnerships with companies that have unique insights but no drug. AbCellera has invested $500 million in their drug discovery/development engine to be able to go all the way from the target to the clinic.

When they went public four years ago they had 100 employees. Today they have 600 on the teams they need to execute. They have completed a Good Manufacturing Practices facility in Vancouver that will be FDA-approved and open in the second half of 2025.

They are very stringent in accepting new partners, because although they get paid upfront, the bulk of the economic value comes from development milestone payments and eventual royalties. They have to believe in the biology, the commercial opportunity, the unmet medical need, the development pathway, the viability of making a commercial product at a reasonable cost of goods, and the capability of the partner as shown by an established track record of developing a drug and the capital needed to take the drug through the clinic and ultimately to patients.

They have negotiated over 200 such programs and have started over 100 of those, 87 of which have downstream participation. 13 partnered molecules are in the clinic. They eventually will look like a royalty pharma company without the huge balance sheet, because they don’t have to buy the royalties.

They are developing 19 antibody drugs on their own. Two programs are in IND-enabling preclinical studies, ABCL635 and ABCL575. They will bring them into the clinic in 2025. AbCellera has $800 million in cash and over $200 million in commitments from the governments of Canada and British Columbia to take these through Phase 1. That gives them a cash runway of more than three years.

The total market value of the company is about $1.15 billion versus over $1.0 billion in liquidity. Cheap! Success with any one of the internal programs would be worth 3x the market cap today, and they have a whole pipeline of candidates. AbCellera is both far less risky and has far more upside than most biotech companies. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various; Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2027 or never

Inovio (INO – $10.20) did a snap financing a year earlier than they needed to, selling 4.67 million shares (20% dilution) to raise about $33 million at $7.69 per share. This gives them a cash runway through FDA approval of INO-3107 next year. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2026

Invitae (NVTAQ – $0.00) apparently did not have its scheduled bankruptcy auction yesterday. The Department of Justice’s bankruptcy watchdog said on Monday that Invitae should not be allowed to hire Kirkland & Ellis as bankruptcy counsel because of the law firm’s work for one of Invitae’s lenders.

They said that Kirkland has a conflict of interest because one of its current clients is private equity firm Deerfield Partners, which is Invitae’s top lender and the “main beneficiary” of a 2023 debt restructuring that placed Deerfield at the front of the line for repayment in Invitae’s bankruptcy. Deerfield is the largest holder of $305 million in secured bonds that were created in the 2023 debt deal. Those secured bonds would be repaid before Invitae’s $1.2 billion in junior bonds.

Invitae’s junior creditors raised concerns about Kirkland’s role in the bankruptcy in an objection filed about a week before the DOJ’s objection. They want to unwind the 2023 debt transaction so that they can free up “hundreds of millions of dollars” to repay junior creditors instead of Deerfield. The bankruptcy Judge will consider Invitae’s request to hire Kirkland at an April 29 hearing in Trenton. Hold NVTAQ for the auction results.

Primary Risk: Current shareholders don’t own any of the restructured company.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: NM

Medicenna (MDNAF – $1.24) also presented at the Bloom Burton Healthcare Conference (AUDIO and SLIDES HERE). They expect a number of key milestones this year, beginning with more data from the MDNA11 monotherapy expansion trial before the end of June. We’ll also get the initial trial expansion data with Keytruda. By the end of this year we’ll get the top line monotherapy data and preliminary combination data. They also expect to get Breakthrough Therapy designation for MDNA55, where they still are looking for a partner.

Click for larger graphic

Click for larger graphic

MDNA11 is the original reason we bought the stock. About 25 years ago a friend died at 42 from kidney cancer after suffering – and I do mean suffering – the side effects of Proleukin. It’s a pretty effective drug but it has to be administered three times a day, each time with extreme side effects that can, quite literally, kill you. MDNA11 can be administered once every two weeks, with low or no side effects.

Click for larger graphic

Click for larger graphic

It is in a monotherapy trial that just expanded to include Keytruda. Merck’s Keytruda is the biggest selling drug in the world, $25 billion last year. They have partnered with Medicenna because only about 1/3 of their oncology patients respond to it. Both companies think a combination of MDNA11 and Keytruda will substantially increase the response rate.

Click for larger graphic

Click for larger graphic

The efficacy data from the monotherapy trial is good. In the last few years, we’ve seen Nektar partner with Bristol Myers Squibb in a $3.6 billion transaction and Sanofi acquire Synthorx for $2.5 billion for one drug. Both of those programs have been abandoned because they were not able to see even one patient responding to the treatment. In contrast, 14 patients taking MDNA11 have shown four responding to treatment, including two complete regressions, one in pancreatic cancer and another in melanoma. Even patients that just have stable disease see durability beyond six months, including one patient who has been stable for a year and a half.

Click for larger graphic

Click for larger graphic

The company has a rich pipeline:

Click for larger graphic

Click for larger graphic

They have over $21 million in cash to carry them through their 2025 milestones. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: 2025

TG Therapeutics (TGTX – $13.99) sold $92 million of Briumvi last year, with expectations of $263.9 million in 2024 and $412.7 million in 2025. TG should be just shy of breakeven this year and move into the black in 2025.

They are developing a subcutaneously injected version of Briumvi to compete with Roche’s SC Ocrevus. SC Ocrevus is expected to be approved in both Europe and the US this year.

Anti-CD20 treatments account for about 40% of the Multiple Sclerosis market and about 50% for those starting a new therapy. The leader is Roche’s twice-annual (for four hours) IV therapy Ocrevus, which generated 2023 net sales of $7.2 billion Second is Novartis’ once-monthly SC Kesimpta, which had 2023 net sales of $2.2 billion. Briumvi’s 1,000 prescriptions in the December quarter translated to about a 10% domestic market share of patients starting on a CD20 therapy, so there’s plenty of headroom for future growth. Briumvi has an average annual cost of $59,000, versus $70,000 for Ocrevus, and $92,000 for Kesimpta. Briumvi is patent protected to 2042.

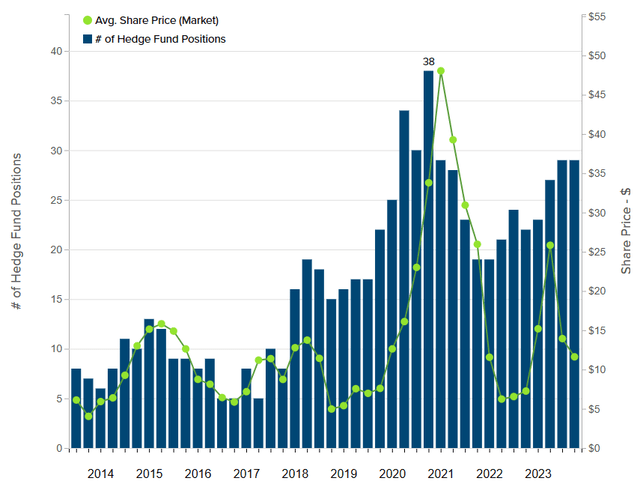

Wall Street has mostly Buy ratings on the stock, but target prices are all over the place. H.C. Wainwright is highest at $45, then B. Riley at $29, and J.P. Morgan at $22. The bears are Goldman Sachs at $13 and BofA at $7. Hedge funds have been buying the stock again:

Click for larger graphic h/t @insidermonkey

Click for larger graphic h/t @insidermonkey

In 2020-2021 the the number of hedge funds holding TGTX peaked at 38, then fell to 19 in early 2022, and now is increasing again. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

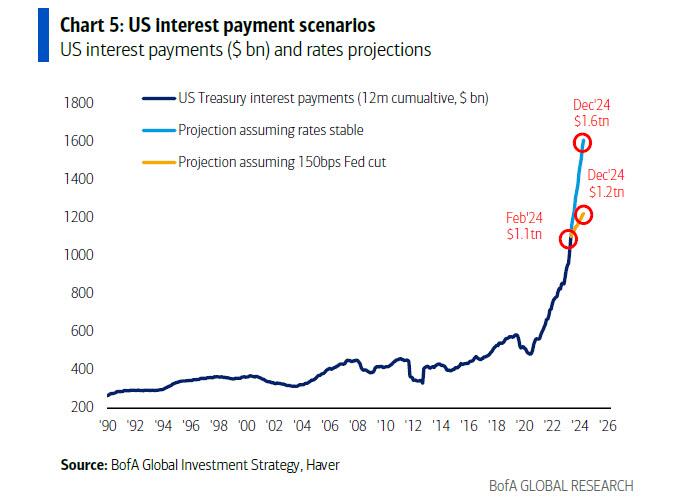

Gold ($2,393.50) hit new all-time record intraday and closing highs today even though significant interest rate cuts are off the table as the US possibly approaches the Minsky Moment of issuing $1 trillion in debt every 100 days. Interest on US debt, now at $1.1 trillion, is set to surpass Social Security spending and become the single largest government outlay before the end of the year.

Click for larger graphic

Click for larger graphic

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

Gold is up $300 in six weeks, its quickest rise in a decade. In his latest report, BofA CIO Michael Hartnett noted that investors are looking beyond the “here and now,” realizing that there is no way markets or the economy can sustain 5% nominal and 2% real rates, and are hedging two things: (1) the risk that the Fed has to cut as CPI accelerates, and (2, more ominously), the “endgame of Fed Interest Cost Control (ICC), Yield Curve Control (YCC), and renewed Quantitative Easing to backstop US government spending.”

In short, he thinks something big is about to break, and if the surge in gold leads to a spike in yields, start the countdown to one of two things: QE and/or YCC, because if the bond market sniffs out the endgame that gold is currently smelling, it will be up to Powell to once again prevent a catastrophic financial collapse.

BofA commodities strategist Michael Widmer wrote: “Gold and silver are among our most preferred commodities, with the yellow metal pushed up by central banks, China investors and, increasingly, Western buyers on a confluence of macro factors, including an end to hiking cycles. Accordingly, we see the yellow metal rally to $3,000/oz by 2025. Silver benefits from that too, with prices also boosted by stronger industrial demand. This could take prices above $30/oz within the next 12 months.”

UBS wrote: “The recent move in gold reminds me of a famous quote: ‘There are decades where nothing happens, and there are weeks where decades happen.’ Looking at history, the gold price can stay in the doldrums for a long time, but when it does breakout the surge is usually fast and furious…Should history repeat itself, it is not too late to participate in the current gold rally. An investor with a two- to three-year view could expect to see gold potentially double from here to more than $4,000. The take-profit signal is when real rates turn negative and when there is a full-blown recession. Today with real rates still high and a recession seemingly far away, it is too early to call the end of the ongoing gold rally.”

Costco is making $100 million to $200 million a month selling gold bars, according to a Wells Fargo equity research note. Last October, the company began selling one-ounce bars made of nearly pure 24-karat gold priced at about $2,000. They sell about 2% above spot prices to members before a 2% cash back reward for executive members and an extra 2% in cash back for those with a Citi card.

They also are selling silver coins in tubes of 25. The one-ounce Canada Maple Leaf silver coins were priced at about $680 before selling out online earlier this month. Silver is up more than gold so far this year as 2024 is expected to mark the fourth straight year of a structural deficit, according to the Silver Institute’s annual World Silver Survey.

The study showed an estimated global silver market deficit of 184.3 million ounces in 2023, the second-highest deficit on record behind 2022’s deficit of 263.5 million ounces. The silver deficit is forecast to rise by 17% to 215.3 million ounces in 2024 due to a 2% growth in demand to a fresh record high of 1.22 billion ounces, led by strong industrial consumption, alongside a 1% decline in total supply.

The fractal dimension continues to signal a trend that can continue for a few weeks before the necessary correction starts.

Miners & Related

Coeur Mining (CDE – $4.44) said the expanded Rochester mine has achieved commercial production and the ramp-up is on schedule. They said: “Materially higher production levels are anticipated to build throughout the second half of 2024 consistent with completion of Rochester’s ramp-up. Once operating at full capacity, throughput levels are expected to be approximately 2.5 times higher than historical levels, making Rochester one of the world’s largest open pit heap leach operations and a key driver of cash flow growth for the Company. It is expected to be America’s largest source of domestically produced and refined silver.”

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $6.77) said total March quarter production reached 5.16 million silver equivalent ounces, consisting of 2.0 million silver ounces and 35,936 gold ounces. The stock was hit because that was down 22% from the December quarter and 32% from last year. The company said the results were in line with its 2024 production plan, but Wall Street expected production of 2.2 million ounces of silver and 40,400 ounces of gold.

The company said that during the quarter they identified and developed a significant new water source at La Encantada in March, and are in the process of increasing water inventory levels and processing rates at the plant. They expects plant ore throughput rates will return to their targeted levels of 3,000 metric tons/day by the third quarter.

Silver production at San Dimas fell 23% from the December quarter and gold output slid 27%, primarily due to a decrease in ore processed and lower silver and gold grades. The company expects to see improvement in grades and throughput during the year.

They completed 120,485 feet of drilling in the quarter, a 10% increase from the December period. Throughout the quarter, up to 17 drill rigs were active, consisting of eleven rigs at San Dimas and six rigs at Santa Elena.

They will release March quarter financial results on May 8. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

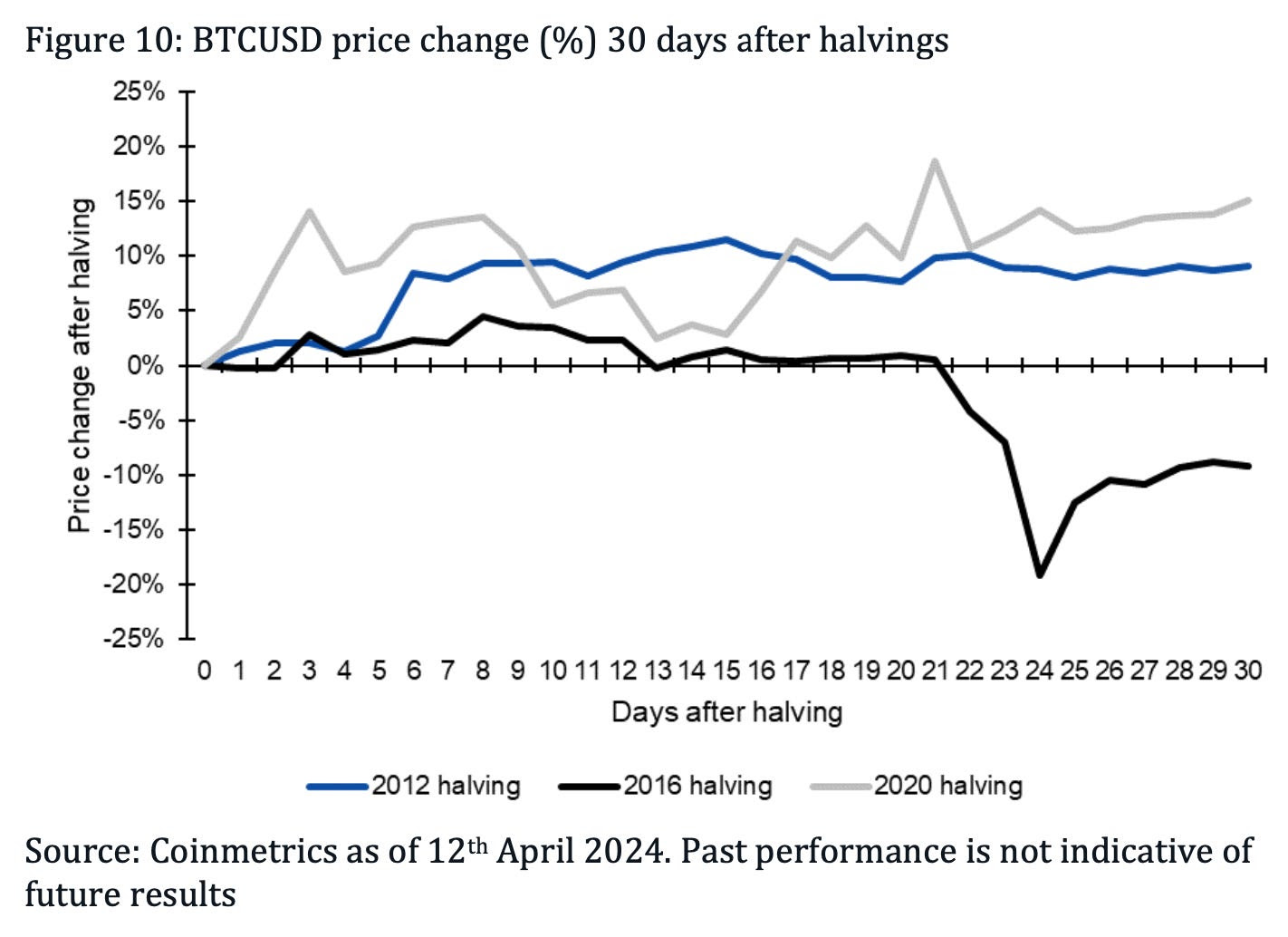

Bitcoin (BTC-USD on Yahoo – $63,493.37) fell before mining rewards are cut in half on Saturday. Here’s how bitcoin reacted in the first 30 days following each halving event.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

And longer term:

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $36.21) only has about 30 institutional holders so far, mostly funds and advisors. They account for only 0.2% of the outstanding shares, compared to the bitcoin futures fund ProShares Bitcoin Strategy ETF (BITO) that has 42% of shares reported via professionals’ 13F filings. It also shows lot of “nibbling” going on as evidenced by the tiny percentage of total portfolio numbers.

Click for larger graphic h/t @EricBalchunas

Click for larger graphic h/t @EricBalchunas

IBIT is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $82.55

Oil fell over $3 a barrel this week as the 4.09 million barrel crude build was far more than the 600,000 expectation, even though there was a huge 2.51 million barrel gasoline draw. I expect a small crude draw for the rest of April into early/mid-May. US production is falling as I expected, but demand is not as strong as I thought it would be.

After the current oil price correction ends, probably here in the low $80s, oil market fundamentals should drive prices back to a higher structural range, $85 to $95. But I don’t expect a spike over $100 this year. We should see oil trade range-bound for the rest of 2024 with a possibility of surprising to the upside by the end of 2025, depending on the US oil production outlook.

Part of the “range-bound” forecast is politics. At the BloombergNEF Summit, White House senior adviser John Podesta responded to a question about a potential further release of oil from the Strategic Petroleum Reserve by saying President Biden “wants to keep the price of gasoline affordable, and we’ll do what we can to make sure that that happens.” Rising prices at the pump will spike this summer.

The Energy Information Administration raised its average price estimate for Brent crude this year to $89 a barrel from $87 previously, which it says “reflects our expectation of strong global oil inventory draws during this quarter and ongoing geopolitical risks.” Middle East tensions and attacks on shipping in the Red Sea contributed to higher prices in March, while extended OPEC+ output cuts “add to upward price pressure right at a time of the year when oil demand typically increases because of the spring and summer driving seasons in the Northern Hemisphere.”

Goldman Sachs said: “Hedge funds sold US Energy for the third straight week (and five of the last six weeks), driven almost entirely by short sales … The sector’s long/short ratio is now at 1.22, a new five-year low.”

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

That should support oil prices over $85, which is where the Saudis want to see them. There are two very wrong perceptions in the oil market. The first is that the OPEC+ voluntary cuts are creating more confusion than answers because aside from the Saudis, voluntary cuts are not happening with any of the other producers.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The second is that US oil production was understated at the end of 2022. Following a methodology change in mid-2023, the Energy Information Administration now overstates US oil production. This has created a massive misconception of the implied growth rate of US shale.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

These two misconceptions will result in a much tighter-than-expected oil market going into 2025. The consensus is expecting the oil market to be in surplus by 2025 due to OPEC+ unwinding its production cuts, but only Saudi Arabia has cut. At the same time, the consensus overestimates US supply. It is making a crucial mistake in assuming the voluntary production cut is real, while also using an incorrect baseline for US oil production.

At the annual FT Commodities Global Summit, the CEO of Vitol Group, the world’s largest independent trader, said his firm now expects demand growth of 1.9 million barrels a day this year – more than 30% higher than the current view of the International Energy Agency. He added: “$80 to $100 feels a sensible range.”

The head of commodities at hedge fund Citadel said: “We are on track to have an extremely tight global oil market. OPEC has definitely regained control.”

A new Chinese mega-refinery just received about 170,000 barrels a day of import quotas, pointing to continued gains in crude demand from the world’s largest importer. At the same time, there was a sudden hit to supply by Mexico’s decision to restrict some of its exports, described as “a bit of a shock to the market.”

With a seasonal demand uptick due over the summer, many traders expect there could be a further rally to come for oil prices in the coming months. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $70.55) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $40.17) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.76) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

EQT (EQT – $36.22) reports March quarter earnings after the close next Tuesday with a conference call Wednesday morning. Due to low natural gas prices, Wall Street expects revenues to fall 16.3% from last year to $1.58 billion, with earnings per share plunging over 60% to 67¢ per share. EQT is a very well-managed company and should be able to do a little better than that.

EQT announced an agreement with Equinor USA Onshore Properties to sell an undivided 40% interest in its non-operated natural gas assets in Northeast Pennsylvania, representing approximately 225 million cubic feet per day (MMcf/d) of forecasted 2025 net production. EQT gets $500 million of cash and upstream and midstream assets:

* * ~26,000 net acres in Monroe County, Ohio with 2025 estimated net production of ~135 MMcfe/d directly offsetting EQT-operated acreage

* * ~10,000 net acres in Lycoming County, Pennsylvania with 2025 estimated net production of ~15 MMcfe/d in existing EQT-operated assets

* * The remaining 16.25% ownership in EQT-operated gathering systems servicing core operated acreage in Lycoming County, Pennsylvania

* * A gas buy-back agreement whereby Equinor will purchase gas from EQT at a premium to in-basin pricing through the March 2028 quarter

Based on recent strip pricing, EQT forecasts aggregate 2025 free cash flow of approximately $75 million from the non-cash consideration. CEO Toby Rice said: “This transaction marks an extremely positive start to our divestiture program, bringing in over $1.1 billion of value, including synergies and development plan optimization, for 40% of our non-operated assets, while retaining gas price upside. We plan to opportunistically divest the remaining portion of our non-operated assets in Northeast Pennsylvania and have tremendous confidence in being able to achieve our de-leveraging goals.”

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $50.16) reports earnings next Tuesday morning. The consensus is forecasting revenues down 1.1% from the 2023 period to $5.33 billion with earnings per share of 25¢, less than half last year’s 52¢. The interesting part will be guidance. For the June quarter, the Street is in print with a revenue forecast of $5.59 billion, down 2.5% from last year. But the copper shortage is hitting right now, and I expect FCX management to nudge them higher. The June quarter earnings estimate is for only 32¢, but increasing copper prices fall straight to the bottom line.

Bank of America metals strategists said the copper supply crisis is here. They wrote: “The much-discussed lack of mine projects is becoming an increasing issue for copper. This, along with investment in green technologies and a rebound of the global economy, should lift prices to $4.65/lb by the fourth quarter.”

Analysts at Citi said consumers of the metal should “urgently hedge” or risk facing $320 billion of cost increases over the next three years. Saying copper is the second bull market this century, they say copper prices are trending higher to average $5.00/lb in the fourth quarter and $6.00/lb by 2026. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

Acreage Holdings (ACRDF – $0.37) moved up after Robert Califf, the head of the FDA, said that there’s “no reason” for the Drug Enforcement Administration to delay its decision to reschedule marijuana from its current high-risk Schedule I category, which includes dangerous drugs like heroin and LSD, to a low-risk Schedule III category for medications like Tylenol and ketamine. Last August, the Department of Health and Human Services wrote a letter to the DEA recommending cannabis be reclassified from Schedule I to Schedule III under the Controlled Substances Act, based on the FDA’s findings. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

* * * * *

* * * * *

Your reading The Maintenance Race Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/18/24. Check out the complete Portfolio page HERE.

Portfolio Protection

June 21 SPY $505 put (SPY240621P00505000 – $13.71)

June 21 SPY $410 put (SPY240621P00410000 – $0.87)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $167.04) – Buy under $175 for new iPhones

Corning (GLW – $30.91) – Buy under $33, target price $60

Gilead Sciences (GILD – $66.16) – Buy under $80, target price $120

Meta (META – $501.80) – Buy under $345, target price $400

PayPal (PYPL – $62.10) – Buy under $68, target price $136

SoftBank (SFTBY – $25.10) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $6.01) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $52.83) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $12.38) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $20.83) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $12.01) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.55) – Buy under $13, target price $30+

Velo3D (VLD – $0.26) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.91) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.39) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.27) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.42) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $10.20) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.24) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.41) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $13.99) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($28.23) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $26.53) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $32.87) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.23) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $31.27) – Buy under $30, target price $50

Coeur Mining (CDE – $4.44) – Buy under $5, target price $20

First Majestic Mining (AG – $6.77) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.44) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.415) – Buy under $10, target price $25

Sprott Inc. (SII – $39.96) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $63,493.37) – Buy

iShares Bitcoin Trust (IBIT – $36.21) – Buy

Ethereum (ETH-USD – $3,054.52) – Buy

Grayscale Ethereum Trust (ETHE – $21.64) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $70.55) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $40.17) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.76) – Buy under $11; $24 target

EQT (EQT – $36.22) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.85) – Buy under $8; $30 target

Freeport McMoRan (FCX – $50.16) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.62) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.71) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.04) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $25.66) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.37) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.01) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.18) – Hold for buyout

Invitae (NVTAQ – $0.00) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st.

To alot of the others holder involved in nvtaq who have alot of sleep with this debacle there will be another hearing on may 6th at 10 am in regards to this auction

Invitae….first 99.99% loss in 50 years of investing. Glorious. Why did I suspend fundamentals to hunch investing? “The Amazon of DNA”. Right.

Agreed,also in March of 21 he had the membership buying scyx up to 24.00 first 54.00 after approval and then a buyout for 170.00 a share,approval did happen as we now sit at a 1.40 a share

The saddest part about nvtaq was that mm had been positive the whole way though the journey from having a buy up to 50.00 a share even as the stock turned snd went south still staying positive And continuing to have faith in it made me continue to dollar cost average all the way down,what a loser,for anyone else here who has lost sleep over this I feel your pain,I am with you,have a nice weekend

I wonder why it is so low as candida auris is so deadly and prevelant.

Somebody else at Seeking Alpha likes AUPH:

https://seekingalpha.com/article/4684467-aurinia-pharmaceuticals-potential-for-significant-upside-by-year-end-2024?mailingid=35091664&messageid=activity_alerts&serial=35091664.535973&utm_campaign=alert-activity&utm_content=authors_alerts&utm_medium=email&utm_source=seeking_alpha&utm_term=35091664.535973&v=1713440870#comment-97676304

MM–on VLD, have you been following recent finances? Phoenix Rising on YMB claims the company is now desperate. 80% probability of bankruptcy, 20% chance of buyout at only 33-35 cents. What do you think?

MM – In developing your response to the above question, please take into account (1) expected sales and gross margins and (2) the increasing likelihood that the warrants will not be exercised anytime soon due to VLD’s steadily declining stock price. Should you be so inclined, some scenario-based financial modeling of monthly cash flows would be very much appreciated. Best regards.

VLD – Reverse Split listed as an item of business at VLD’s 6/10/24 annual stockholder’s meeting.

https://ir.velo3d.com/sec-filings/all-sec-filings##document-771-0001825079-24-000013-2

We all knew it was coming, now it’s official…

“Approve an amendment to our certificate of incorporation, as amended, to effect a reverse stock split of our outstanding shares of common stock, par value $0.00001 per share, at a ratio, ranging from one-for-five (1:5) to one-for-fifty (1:50), with the exact ratio to be set within that range at the discretion of our board of directors without further approval or authorization of our stockholders.”

MDNA (long) ACXP (less so) — If you have any questions about MDNA or ACXP, I would advise joining BioPub right away. CEOs of each company will be appearing on Biopub Zoom calls to discuss the present and future and answer your questions. MDNA this Friday, April 26 at 12:30 pm and ACXP on May 10.

ACXP–I don’t believe much of what CEO Luci says. Liar–“a nip and a tuck”, “I have already spoken to the buyer”. All this many months ago when the stock was 50-100% higher than today. If he says anything that you believe, let us know, please.

ACXP Any reason you can think of for canceling there stock offering?

An S-1 filing is often done with something like an IPO; it’s a registration of new securities. An S-3 shelf registration is a much shorter, easier form that can also be kept confidential until a transaction is finished, but there are some restrictions. We usually see S-3s when we think of companies raising cash from a private placement or an ATM. But there are cases where an S-1 can be prevalent: very small companies. There’s an SEC clause known as the “Baby shelf restriction” for companies under $75M in market cap; they are barred from offering shares more than a third of their existing market cap in a given year.There’s a great overview article here (https://www.faegredrinker.com/en/insights/publications/2022/8/the-baby-shelf-requirements-a-compliance-guide-for-issuers). Interestingly, the last paragraph has this far too prescient note:

“An issuer can always file a Form S-1 and raise capital without being restricted by the baby shelf requirements, but a Form S-1 registration statement is usually specific to a single offering and must be filed publicly and declared effective by the SEC prior to any sales. This makes it significantly less beneficial to companies looking to take advantage of short trading windows and may trigger sales by existing investors (and a stock price slump) by alerting existing investors wary of possible dilution of future potential securities sales.”

How does all this relate to ACXP?

BLGO is a stock that could go to the moon

https://feeds.issuerdirect.com/news-release.html?newsid=4602562297433877

MDNA (longer today)

https://ir.medicenna.com/news-releases/news-release-details/medicenna-announces-oral-presentation-mdna11-data-phase-12

An oral ASCO presentation for Medicenna on MDNA11? Great news. The data must continue to look good. This will be a fresh view, so I’m optimistic we’ll see at least one or two new partial responders in the monotherapy setting. Would love to see the maturing combination data, but it might be too soon. We’ll see! Stock is up strongly today, though still shy of where it was just a few weeks ago

BLGO or MDNA?

MDNA is already proving its value in the IL-2 space where others have failed. BLGO has yet to prove that it can deliver what it promises, but if its New Jersey customer can verify BLGO’s claims (likely around the end of the year) then it will be off to the races for BLGO. I also expect BLGO to announce additional customers over the next few months, which should add momentum. I have both, but my MDNA stack is currently 5x the size of my BLGO stack.

MDNA or MDNAF? .157 vs 1.39 why one over the other?

MM recommends MDNAF

If you look at the chart for MDNA it only goes into the 4th quarter of 2023. It was delisted from the Nasdaq at that point, with the last price at $.157, and began trading as MDNAF. Same company but MDNAF is it’s current symbol and the only one that now trades.

Thanks for the help

APTO – Just released a new corporate presentation and one of the slides (attached) provides their triplet development plan through 2026. They project their Phase 3 trial to start late 2026 so FDA approval won’t happen until 2028 or maybe even 2029 as APTO has a history of progressing through trials slower than they’ve guided. Given that, I expect the more distant milestones in the slide to push out over time.

Their average cash burn over the last three years has been $40 million per year so it will take a huge amount of additional capital to get them into the 2028/2029 timeframe.

NVTA – Invitae Enters into Agreement with Labcorp for Sale of Business

https://ir.invitae.com/news-and-events/press-releases/press-release-details/2024/Invitae-Enters-into-Agreement-with-Labcorp-for-Sale-of-Business/default.aspx

And the winning bid…$239 million cash.

$239M? That’s a steal for the AMZN of genetic testing! China has invested at least $1B and maybe twice that into its genetic testing business, but at least they seem to be making money off of it.

https://bioedge.org/organ-donation/china-accused-of-sequencing-tibetan-and-uyghur-dna-to-supply-organ-transplant-market/

Interesting article you posted. The only way to make money in genetic testing is by boosting the number of tests to serve the amazon number of atrocities of the CCP. For the humane world, there is a place for judicious genetic testing, but the numbers of such tests multiplied by the modest revenue per test is small, a bad business model. I have warned about this for a few years. NVTA got a gift at $239M.

Labcorp bought the smaller lab Enzo that my office used. Quest and Labcorp grew to dominate the lab business by acquisitions. Labcorp has more available tests paid by insurance, so I regard it as the leader.

If you buy your labs via LifeExtention.com, then fulfill it through LabCorp, you can save a bunch. I just got a lipid panel with liver function test for $26 bucks. If I go through my primary, it’s more like $400 ( although discounted with insurance).

Life Extension is a great resource. I have wholesale accounts at numerous nutrition companies, but I still buy a few items from LE at great prices, especially during flash overstock sales at sometimes 70% off. The live personal customer service is tops–they answer the phone immediately, rarely do I wait as much as 1 min. I don’t do business with any company that doesn’t have real people answering the phone. LE is almost 24/7.

As for lab tests, basic things like lipid panel and liver function test won’t cost you anything besides a modest copay of $10 via insurance. The $400 charge is ala carte for each of many tests paid by cash for someone without insurance. If you have insurance with a huge deductible, it is discounted by about 90%. This is one way people without insurance are scammed. People are incentivized to carry insurance with expensive premiums. The insurance system screws you one way or the other.

I use the ICD 10 code book for all the diagnoses that justify each lab test. This book is thick, the size of a Manhattan telephone book. You can ask your doctor to do many tests that are mostly all covered by insurance if he provides the ICD 10 codes. The real problem is that the socialized medical system everywhere stigmatizes MD’s who go beyond the most basic tests. Even basic things like hemoglobin A1c for diabetes, vitamin D 25 hydroxy, B12 levels aren’t covered unless you know whatever arbitrary codes can be used for insurance billing. My office has a Labcorp rep to help with troubleshooting. Most MD’s won’t cooperate with intelligent patients who ask for specialized tests. They are too busy wasting time with electronic record documentation and stupid bureaucratic regulations. There’s where LE provides cheaper prices for sophisticated panels, for patients who are fed up with their socialist robotic MD’s.

Is it still a hold for buyout? 🙂

LOL!

NVTA’s latest 8K shows their financials as of 2/29/24. They reported assets of $476 million & liabilities of $1.702 billion.

“Labcorp will acquire substantially all of the Company’s assets on a going concern basis for $239 million in cash consideration, plus other non-cash consideration.”

So Labcorp gets $476 million in assets, $153 million of which is cash, for $239 million plus whatever the non-cash consideration is.

There’s a paltry $239 million available for $1.702 billion in payables & debt. Ouch!

NVTAQ was up 800 percent today. Just sayin’.

New World Investor for 4.25.24 is posted. Added ABCL to Long-Term buys. Sold all four China investments.