Dear New World Investor:

This morning’s June Consumer Price Index report showed headline inflation actually fell 0.1% from May and increased only 3.9% from last year. Both numbers were below May (0.0% MoM and 3.3% YoY) and below the consensus estimates for +0.0% MoM and +3.1% YoY. This is the first time since May 2020 that monthly headline CPI came in negative. It’s also the slowest annual gain in prices since March 2021.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

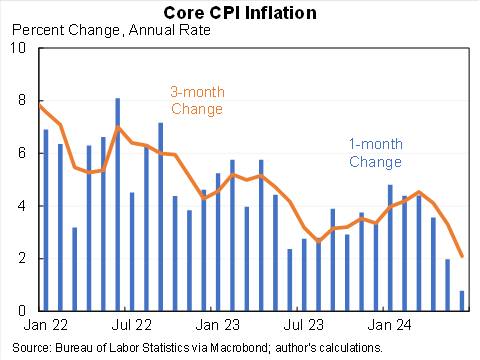

The core CPI, which strips out the more volatile costs of food and gas, climbed 0.1% MoM and 3.3% YoY. Again, both numbers were below May’s 0.2% MoM and 3.4% YoY, and below the consensus estimates for +0.2% MoM and +3.4% YoY. It was the smallest month-over-month increase in core prices since August 2021. The three-month annualized core CPI dropped to 2.1% in June, its lowest level since Covid.

Click for larger graphic h/t @jasonfurman

The troublesome shelter index rose 5.2% YoY, the same as May, and 0.2% MoM, a slowdown from May’s 0.4%. The indices for rent and owners’ equivalent rent each rose 0.3% MoM, the smallest increases in these indices since August 2021. Shelter is 34% of the core CPI and 18% of the core Personal Consumption Expenditures Index (PCE). As we know, aside from the core PCE, the Fed is most focused on core Services CPI inflation ex-shelter. That had a very unusual month-over-month negative print in May and did it again today – minus 0.1% was the lowest since August 2021.

Click for larger graphic h/t @BobEUnlimited

Inflation is over. The CME FedWatch tool showed markets were pricing in an 89% chance that the Fed begins to cut rates at its September meeting, up from 75% on Wednesday. I doubt the decline in the consumer price index between May and June will repeat, but it does strengthen the case for the Federal Reserve to begin cutting interest rates in September, especially since the labor market has softened.

Some market watchers think the Fed could even cut in July, but I doubt it. It would raise questions of “What do they know about the economy that we don’t know?” Plus, the Fed still needs additional evidence of slowing price pressures to be absolutely certain of the inflation path getting to their 2% target.

Of course, there’s not a chance the Fed will raise the Fed funds rate. June was the first month since October 2020 when not a single global central bank raised rates. If the Fed raised, the Dollar Wrecking Ball would cripple many other economies.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The only question is when the Fed will cut rates, not if – so that cut is already discounted by the markets. Today the small-cap Russell 2000 was up 3.57% while the tech heavy Nasdaq 100 was down 2.24%. This is what happens when markets broaden out, and broadening markets mean more upside to come. Even biotechs caught a bid:

Click for larger graphic

In other news, June payrolls supposedly increased by 206,000, above the 190,000 consensus estimate. I say “supposedly” because the May number was revised down just a smidge from the 272,000 initially reported to 218,000.

The first and second revisions have been pretty dramatic. Something is seriously wrong with their models.

Click for larger graphic h/t Mish

Click for larger graphic h/t Mish

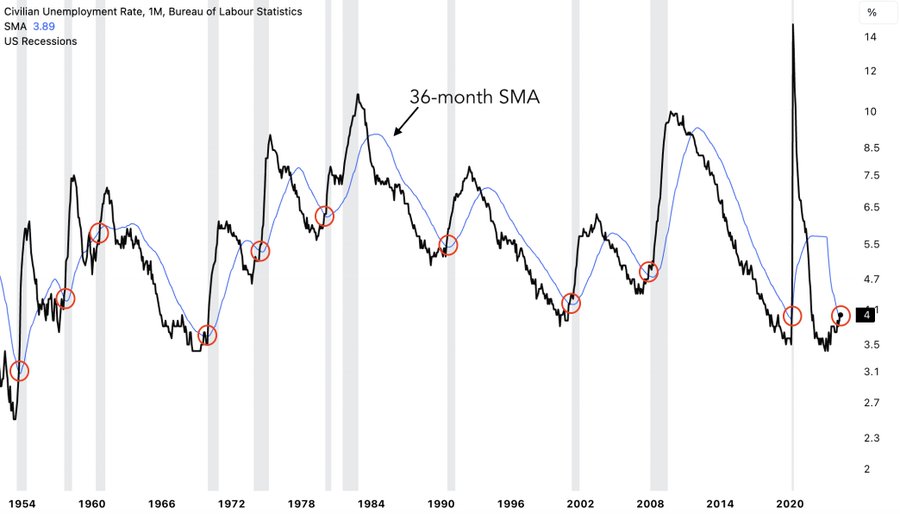

All of the job gains over the last year have come from typically low-earning, part time roles. The number of full-time jobs peaked at 134.8 million in June 2023, and is now down to 133.2 million – a loss of 1.6 million full-time jobs over the last year. The unemployment rate rose from 4.0% in May to 4.1% in June, the highest reading in almost three years. It has jumped from a low of 3.4% to 4.1%, while continuing jobless claims have reached 1.86 million – the highest level since November 2021.

Click for larger graphic h/t @OphirGottlieb

Click for larger graphic h/t @OphirGottlieb

A recession is now inevitable and we may already be in one. Job openings have been rapidly declining, and such sharp drops have only occurred three times since 2000: The dotcom bubble, the Great Financial Crisis, and the pandemic. All three ended with a sharp economic downturn. The bad part this time is that the consumer has run out of excess savings and is holding record levels of credit card debt.

Click for larger graphic h/t @GameofTrades_

Click for larger graphic h/t @GameofTrades_

The unemployment rate has moved above its 36-month moving average. Such a development has happened 10 prior times since 1952. Every single time, it ended in a recession.

Click for larger graphic h/t @GameofTrades_

Click for larger graphic h/t @GameofTrades_

At the same time, the “strong” monthly payroll numbers are being revised down sharply by the more accurate quarterly Business Employment Dynamics (BED) report from the Bureau of Labor Statistics. Mike Shedlock (Mish) said for the September 2023 quarter, the BED report shows gross job gains of 7.559 million and gross job losses of 7.751 million for a net loss of 192,000 jobs. The BLS monthly jobs reports show a gain of 640,000 jobs.

Click for larger graphic h/t Mish

Click for larger graphic h/t Mish

The BED data is based on 9.1 million establishments while the monthly jobs reports are only based on 670,000 establishments. The monthly reports are timely but inaccurate. In the June 2023 quarter they overstated payrolls by 489,000 jobs, and in the September quarter by 832,000 jobs, That’s a total of 1.321 million phantom jobs. We get the December quarter BED report on July 24.

Finally, we just got the lowest ISM Services number since the heart of the pandemic.

Click for larger graphic h/t @Lisaabramowic

And, Most Important: I often talk about the 36-year stock market cycle, due to peak again in 2036. @jimwpaulsen has noticed a similar pattern and writes: “The US stock market is in its 3rd Super Cycle of the last 100 years. If it continues to mimic the last 2 cycles for the next 6 years, it will deliver 14.7% average annualized price gains. See my full report and sign up for a free trial @ http://paulsenperspectives.substack.com.”

Click for larger graphic h/t @jimwpaulsen

The Bottom Line: I still expect a mild recession and a drop in the S&P 500 back to the 5000 area, but it may not happen until 2025. It will be a buying opportunity for the continued uptrend to 2036 as Artificial Intelligence and the metaverse remake the world’s economy.

Market Outlook

Even after today’s drop, the S&P 500 added 0.9% since last Wednesday with seven straight up days to a new all-time high yesterday over 5600 – its 37th record this year. The Index is up 17.1% year-to-date. When the S&P 500 was up double digits at the midpoint of the year, the second half of the year again does better than most years.

Click for larger graphic h/t @RyanDetrick

The Nasdaq Composite gained 0.5% to new records yesterday and is up 21.8% for the year. The tech-heavy Nasdaq 100, driven by the Magnificent 7, has been doing the heavy lifting so far this year and it may be just getting started:

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

Backing up the Magnificent 7, BofA pointed out that earnings for the S&P 493 haven’t registered year-over-year growth since the fourth quarter of 2022 – and that is about to change. The stealth earnings recession for the vast majority of companies in the S&P 500 is over.

Click for larger graphic h/t @BankofAmerica

The SPDR S&P Biotech Exchange-Traded Fund (XBI) jumped 7.8% as investors realized interest rate cuts benefit long-term growth stocks the most. It is up 9.7% year-to-date. The small-cap Russell 2000 booked a strong 4.3%, including 3.8% today, and is up 4.8% in 2024 – with much more to come.

Wrong-footed investors have poured a record amount of cash into money-market funds that will cushion any decline:

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

And it’s very strange that new daily all-time highs aren’t enough to get investors greedy yet. They will – at the wrong time, as usual.

Click for larger graphic h/t CNN

Click for larger graphic h/t CNN

Finally, JPMorgan fired Marko Kolanovic, their macro analyst, for being the last macro bear on Wall Street. Kolanovic called for a recession that hasn’t materialized (I sympathize), largely missed the artificial-intelligence boom that has propelled technology stocks for the past 18 months, and is predicting a 24% decline in the S&P by yearend. If you tell clients that markets will fall and they rise instead, your clients hate you, your sales force has trouble writing tickets, and your firm loses face and money.

Morgan Stanley’s Mike Wilson, long one of Wall Street’s most prominent bears, dropped his bet against the S&P 500 in May, leaving Kolanovic and JPMorgan as the outlier. Morgan Stanley sent an internal memo in February announcing that Wilson was leaving his post as chairman of the bank’s Global Investment Committee.

The fractal dimension at least stopped dropping after today’s S&P sell-off, but it’s going to take many more points or, more likely, many more weeks to get the fractals fully consolidated again.

Top 5

Changes this week: Added CMPS to Near-Term

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

CMPS – Compass Pathways – Phase 3 data release and rebound from negative AdCom review of MDMA

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for June quarter real GDP growth increased back to +2.0% due to big increases in personal consumption expenditures growth and private domestic investment growth. Color me dubious. The first government estimate comes July 25.

Click for larger graphic

Click for larger graphic

The June payrolls report showed a 1.2% year-over-year decline in Full Time Work. In the past, that shows no false positives in predicting a recession.

Click for larger graphic h/t @DrJStrategy

Click for larger graphic h/t @DrJStrategy

Coming Events

Our companies start reporting on July 30, followed by the earnings deluge. All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, July 15

AKBA – Akebia – 9:30am – H.C. Wainwright Virtual Kidney Conference

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $227.57) rose even though Samsung announced its all-new Galaxy Z Fold6, Galaxy Z Flip6, and Galaxy AI. Samsung, not surprisingly, is making its generative AI offerings a major selling point for both of the phones. Samsung’s software provides generative AI features ranging from real-time translation and conversation capabilities – that’s impressive – to photo editing tools and productivity options.

Starting at $1,099 for the Z Flip6 and $1,899 for the Z Fold6, these are not cheap. Apple’s iPhone 15 Pro starts at $999 and the larger Pro Max starts at $1,199. I expect the coming iPhone 16 to underprice Samsung.

The addition of Apple Intelligence to the iPhone 16 is expected to drive up consumer demand. According to Bloomberg, Apple plans to ship at least 90 million iPhone 16s before year’s end, which would be an 11% increase over the number of iPhone 15s shipped during the second half of 2023.

In a very odd research note, Piper Sandler (1) raised their target price, and (2) said the good news was already priced in. They kept their Neutral rating and raised their target from $190 (oops) to $225. They wrote: “From our perspective, the excitement is warranted, as AI could be a needle mover for upgrades. In addition, a return to growth in iPhone sales in China could create a tailwind as well in the second half. However, given the current valuation (~32x NTM consensus EPS) and the growing risk of a consumer spending headwind, we feel like a lot of good news is already priced into the stock…We’ve been hesitant on consumer use-cases for AI to-date. From our perspective, we certainly see a scenario where Apple Intelligence drives a ‘super cycle,’ but we aren’t ready to ascribe a ‘super cycle’ as a base case as the recent stock move might suggest.”

Needham raised their target price from $220 to $260 and reiterated their Buy rating. But they expressed concern that Apple’s revenue growth rate could be at risk in the next three years and suggested that Apple build an advertising business similar to the one Amazon has built. Gee, I wonder if Apple has ever thought of that?

They grumbled that the company is spending its capital on share buybacks instead of generative artificial intelligence infrastructure, apparently unaware that Apple gushes cash and spends all it has to on both.

Apple and Major League Baseball announced August’s Friday Night Doubleheader schedule on Apple TV with no blackouts. Just on the off-chance there are subscribers who are interested:

Friday, August 2

Kansas City Royals at Detroit Tigers

6:30pm ET

Milwaukee Brewers at Washington Nationals

6:30pm ET

Friday, August 9

Cleveland Guardians at Minnesota Twins

8:00pm ET

Cincinnati Reds at Milwaukee Brewers

8:00pm ET

Friday, August 16

Toronto Blue Jays at Chicago Cubs

2:00pm ET

Seattle Mariners at Pittsburgh Pirates

6:30pm ET

Friday, August 23

St. Louis Cardinals at Minnesota Twins

8:00pm ET

Cincinnati Reds at Pittsburgh Pirates

6:30pm ET

Friday, August 30

Seattle Mariners at Los Angeles Angels

9:30pm ET

San Diego Padres at Tampa Bay Rays

6:30pm ET

AAPL is a HOLD – expect to move back to Buy under $175 for new iPhones.

Corning (GLW – $45.05) jumped after they said June quarter core sales around $3.6 billion will exceed their $3.4 billion guidance and mark their return to year-over-year growth. Core earnings per share will be at the high end or slightly above their 42¢ to 46¢ guidance. The outperformance was primarily driven by strong adoption of new optical connectivity products for Generative AI – OMG, Corning is an AI stock!

Just kidding, but get ready for 12 straight quarters of announcements like this, and collect a 2.5% dividend along the way. And they began buying back stock in the June quarter. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences (GILD – $69.97) was upgraded from Market Perform to Outperform with a $93 target by Raymond James on positive data from the PURPOSE-1 trial of long acting lenacapavir in HIV pre-exposure prophylaxis and expected approval of seladelpar on August 14. They think lenacapavir PrEP and seladelpar could contribute $3.7 billion in combined annual sales by 2030. GILD is a Long-Term Buy under $80 for a first target of $120.

Palantir (PLTR – $27.64), as my friend Keith Fitz-Gerald pointed out, is up over 360% since its late 2022 low at $6.10. So two days ago, FXEmpire said a “rare bullish signal” flashed for PLTR. Really? How timely. The “rare bullish signal” is unusually large, presumably institutional, volumes in Palantir stock, as signaled by the green bars:

Click for larger graphic h/t @FXEmpirecom

Oracle certified Palantir’s Foundry Platform and Artificial Intelligence Platform (AIP) on their cloud infrastructure. Customers don’t have to build an expensive AI supercomputer to begin using Palantir’s AI and decision acceleration platforms. Customers can easily meet their regulatory, performance, and security needs. It even is available on Oracle’s air-gapped regions for defense and intelligence customers. PLTR is a Buy under $22 for a $100+ target.

SoftBank (SFTBY – $36.02) completed the early redemption of all $766.814 million of its US$-denominated 4.750% Senior Notes due September 19, 2024, which were issued in 2017.

A rumor is going around that CEO Masayoshi Son wants to borrow up to $10 billion to invest in energy-related projects. Masa said last month the group would ramp up its power generation business primarily in the US to supply power to generative AI projects worldwide. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $17.76) will hold a grand opening of Fab2, its high-volume production facility in Penang, Malaysia, on August 8. Fab2 will house up to four high-volume production lines capable of producing tens of millions of high-performance batteries for consumer electronics devices like smartphones, IoT devices, and laptops.

Enovix has begun producing initial samples for customers from its Agility Line in Fab2 and, in parallel, is finalizing Site Acceptance Testing of the line. Enovix is also far along in bringing up its first high-volume production line in time to support customer needs as they progress through the qualification process this year. Factory Acceptance Testing of the high-volume line was recently completed.

Meanwhile, lithium prices have dropped sharply and lithium-ion battery prices are plummeting.

Click for larger graphic h/t @colinmckerrache

This will not pressure Enovix battery prices any more than a drop in nickle-cadmium battery prices would have any impact on lithium-ion. Devices that desperately need more battery life to cope with AI applications need to move on to newer technologies.

Today, Volkswagen announced their second bad EV decision in two weeks. The first was to invest $5 billion in Rivian, the fourth-most troubled car in the J. D. Power survey that I posted last week and a failing EV maker with near-zero self-driving capability. Today’s was a license from QuantumScape to mass-produce battery cells based on QuantumScape’s technology platform “upon satisfactory technical progress” (which they will never see). Under the non-exclusive license, Volkswagen can manufacture up to 40 gigawatt-hours (GWh) per year using QuantumScape’s technology, with the option to expand up to 80 GWh annually – enough to power about one million vehicles per year. Note that “The agreement supersedes a joint venture between the Volkswagen Group and QuantumScape to co-manufacture batteries.” Gee, I wonder why co-manufacturing didn’t work out.

There are a number of positive headlines in the weeks ahead that could serve as a positive catalyst for Enovix stock. The June quarter earnings call should be as constructive as the March quarter call. The Fab 2 grand opening event will take off the table concerns about the company’s ability to scale production. Short interest is 43.280 million shares or 30.92% of the float, according to yesterday’s report. With the stock held 16.39% by insiders and 50.22% by institutions, you need to have your head examined to be short Enovix. When the short covering starts the stock could trade well into the $30s in a heartbeat. This Seeking Alpha author gets it. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

QuickLogic (QUIK – $11.12) got a $5.26 million contract award, the third tranche of the Strategic Radiation Hardened Contract that started in August 2022. The contract is to develop and demonstrate a Strategic Radiation Hardened (SRH) high reliability Field Programmable Gate Array (FPGA) technology to support identified and future Department of Defense strategic and space system requirements. QuickLogic will continue as the Prime Contractor, collaborating with subcontractors including Honeywell Aerospace and Everspin Technologies. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $5.33) said they are making great progress at Stennis. The team is methodically working through more than 300 integrated tests bringing the test stand and Archimedes to life. They are into the big tests now with spin primes (pictured) complete and all the data looking good.

Click for larger graphic

Streaming July 17th, Wild Wild Space is an HBO Original Documentary by Academy Award winning director Ross Kauffman, based on Ashlee Vance’s New York Times best-selling book When The Heavens Went on Sale. This is the most candid behind-the-scenes look at Rocket Lab’s founding and the fierce race to open access to space for small satellites.

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me. Today, the market agreed.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Inovio (INO – $11.04) appointed Steven Egge as Chief Commercial Officer. He will lead the commercial strategy and operations to launch INO-3107 as a treatment for recurrent respiratory papillomatosis. He was Senior Vice President and General Manager for Women’s Health at Sumitomo Pharma (formerly Myovant Sciences), and before that was at Merck for twenty years. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

Inflation MegaShift

Commodities

It looks like we’re going to hit “unprecedented levels” in each commodity group before the markets realize it’s a trend.

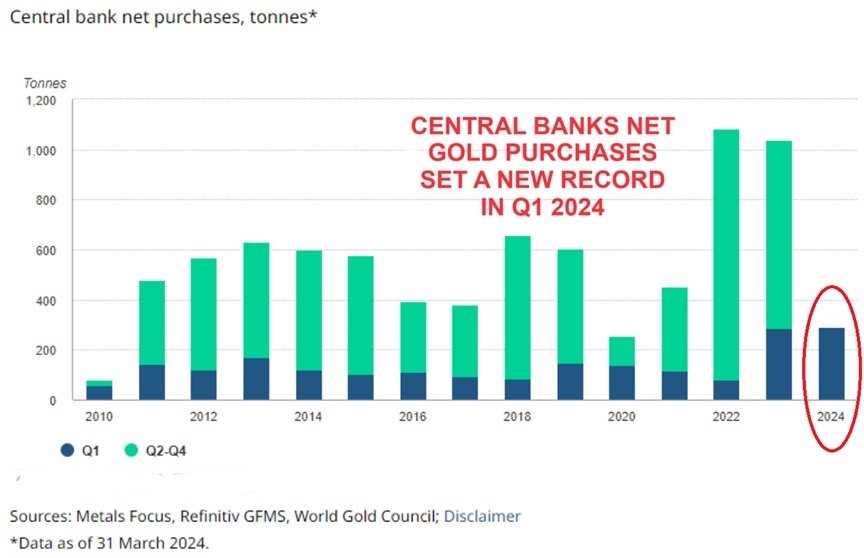

Gold ($2,420.90) gained as central banks continued their gold-buying spree with record gold purchases in the March quarter.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Hedge funds have built their largest long gold position in more than four years, with room for more.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Yet gold miners have the cheapest Price/Book Value ratio in 40 years.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

The fractal dimension is nearly fully consolidated. It’s ready and able to support another big leg up in the yellow metal.

Miners & Related

Coeur Mining (CDE – $6.77) reported that its recently-expanded Rochester silver and gold mine in Nevada successfully completed ramp-up activities to steady-state throughput at the end of the June quarter by achieving daily throughput rates of over 88,000 tons per day. CEO Mitch Krebs said: “With the ramp-up now achieved, Rochester is expected to lead the Company to a free cash flow inflection point during the second half of the year, which will enable the Company to reduce debt levels.”

That’s what I wanted to hear! CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.77) reported June quarter preliminary sales and revenue. They sold approximately 17,400 attributable gold equivalent ounces and realized preliminary revenue of $41.4 million. Preliminary cost of sales (excluding depletion) was $4.7 million, resulting in cash operating margins of approximately $2,043 per attributable gold equivalent ounce.

CEO Nolan Watson did his fifth shareholder FAQ:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $57,328.18) dropped as the Mt. Gox bankruptcy trustee moved 47,228 coins (worth $2.71 billion) from cold storage to a new wallet, possibly in preparation for payouts to creditors. The slump forced the largest wave of liquidations since mid-April, as $541.45 million in future contracts was wiped out. Long liquidations accounted for a whopping $472 million. Analysts feared a drop to $51,000, but bitcoin quickly began recovering.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $32.70) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $82.84

Oil is solidly bid in the low $80s, with the next $10 far more likely to be up instead of down. This is month-to-date data, but still… Saudi crude exports need to materially jump over the next 20 days to bring up the overall average.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Maybe OPEC+ is trying to force a US recession?

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

But US demand is very strong. Total 4-week average US implied oil demand is at the highest level for this time of the year over the last five years.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The July 2026 Crude Oil Futures (CLN26.NYM – $no trades – June closed at $71.14) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $40.76) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.16) got approval to purchase up to 15,689,839 common shares, representing approximately 10% of its public float, over the next 12 months. VET is a buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

Energy Fuels (UUUU – $6.65) ticked up after Kazakhstan increased extraction taxes for uranium, which will be passed on to customers as higher U308 prices. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

500 years of interest rates, visualized:

Click for larger graphic h/t @BrianFeroldi

Click for larger graphic h/t @BrianFeroldi

* * * * *

“About every ten years, we have the biggest crisis in 50 years.”

—Paul Volcker, Former Chairman of the Federal Reserve

from Boom and Bust : Financial Cycles and Human Prosperity by Alex J. Pollock, AEI Press, 2010.

* * * * *

Your worried about assassinations Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 7/11/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $45.05) – Buy under $33, target price $60

Gilead Sciences (GILD – $69.97) – Buy under $80, target price $120

Palantir (PLTR – $27.64) – Buy under $22, target price $100+

PayPal (PYPL – $59.99) – Buy under $68, target price $136

SoftBank (SFTBY – $36.02) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $17.76) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.08) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $7.48) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.99) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $11.12) – Buy under $10, target price $40

Rocket Lab (RKLB – $5.33) – Buy under $13, target price $30+

Velo3D (VLD – $3.08) – Buy under $10, target price $100

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.13) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.27) – Buy under $2, target $20

Compass Pathways (CMPS – $7.22) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $5.47) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $11.04) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.41) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.22) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $21.39) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($31.73) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.77) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $34.96) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $23.31) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $35.69) – Buy under $30, target price $50

Coeur Mining (CDE – $6.77) – Buy under $5, target price $20

First Majestic Mining (AG – $6.66) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.48) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.77) – Buy under $10, target price $25

Sprott Inc. (SII – $45.74) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $57,328.18) – Buy

iShares Bitcoin Trust (IBIT – $32.70) – Buy

Ethereum (ETH-USD – $3,107.43) – Buy

Grayscale Ethereum Trust (ETHE – $29.11) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $no trades – June closed at $71.14) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $40.76) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.16) – Buy under $11; $24 target

EQT (EQT – $37.19) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.65) – Buy under $8; $30 target

Freeport McMoRan (FCX – $51.51) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $227.57) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $512.70) – Expect to move back to Buy under $400

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

2

For the gamblers. TNA might be a decent play on the rotation. I picked up a small amount with a tight stop. 3x plays are dangerous though.

So far, so good.

I hope btc hasnt finished its upward cycle this time yet.

MM – why the ignoring of requests for SCYX updates. You said before you need to be more responsive to this message board, youve advocated for SCYX and many here own it, where are the triial results and whats status of return to manufacturing, please provide some answers, thank you

ditto

I can’t update if the company doesn’t do an SEC filing or a press release.

TO SCYX INVESTORS:

I didn’t know much about the contamination issue at SCYX. I found this which some may find interesting. It sounds like to me the problem is in a component of the drug capsule?

Sep 27, 2023 | Audience: Health Professional, Pharmacy, Consumer

JERSEY CITY, N.J., Sept. 27, 2023 — Scynexis, Inc. is conducting a voluntary nationwide recall of 2 lots of Brexafemme (ibrexafungerp tablets) to the consumer level in the US market due to potential cross contamination with a non- antibacterial ß-lactam drug substance in the ibrexafungerp citrate used to manufacture the Brexafemme tablets. During a review of manufacturing equipment and cleaning activities at a supplier, Scynexis was made aware of potential cross-contamination risk with a non-antibacterial beta-lactam drug substance. This press release provides additional details on the voluntary product recall recently disclosed by Scynexis.

Risk Statement: The potential cross contamination with a non-antibacterial beta-lactam drug substance could lead to hypersensitivity reactions such as swelling, rash, urticaria and anaphylaxis, a potentially life-threatening adverse reaction. To date, Scynexis has not received any reports of adverse events established to be due to the possible beta-lactam cross contamination.

Brexafemme is an antifungal product indicated for the treatment of vulvovaginal candidiasis (VVC) and the reduction of the incidence of recurrent vulvovaginal candidiasis (RVVC).

Brexafemme is dispensed in a carton and packaged in blister packs with four 150-mg tablets (NDC 75788-115-04). Brexafemme tablet for oral administration is a purple, oval, biconvex shaped, film-coated tablet debossed with 150 on one side and SCY on the other side. The affected Brexafemme lots include the following lots and expiration dates: LF21000008 (expiration date 11/2023) and LF22000051 (expiration date 11/2025). The recalled lots were distributed nationwide to wholesalers across the US, beginning in December 2022.

Scynexis is engaging with Sedgwick to manage the recall of the product down to the consumer level. Sedgwick will be notifying Brexafemme® distributors via a recall notification letter and will be arranging for the return of the recalled lot from distributors, retailers, and consumers.

Consumers with questions regarding this recall can contact Sedgwick at 1-877-551-7154. Office hours: Monday to Friday, 8:00 AM to 5:00 PM ET.

TO:CUNNINGHAM

Ibrexafungerp is used to treat fungal or yeast infections, including vulvovaginal candidiasis. It is also used to reduce the risk of the vulvovaginal candidiasis infection coming back. This medicine works by killing the fungus or yeast, or preventing its growth.

I don’t know if this is part of the drug or part of the capsule. This was off a Mayo clinic article.

TO: CUNNINGHAM

My last post. Everyone but me probably knows all my 3 posts. The artical below clarifies the problems to me.

“We have relied on third-party contract manufacturers for synthesis of our clinical compounds and manufacture of drug product,” Scynexis said in its 2022 annual report. “We expect to continue to rely on either existing or alternative third-party manufacturers to supply ibrexafungerp for our performance of clinical trials and for supplying GSK needs for clinical and commercial product until it obtains its own source of supply.”

A recent GSK review of the manufacturing process and equipment at an unnamed third-party manufacturer found equipment used to make a non-antibacterial beta-lactam drug substance is also used in the manufacturing of ibrexafungerp, Scynexis said in the regulatory filing. FDA guidance recommends segregating the manufacturing processes because beta-lactam compounds may trigger hypersensitivity or allergic reactions in some people. The filing states that without the FDA recommended segregation of manufacturing processes, there is a risk of cross contamination.

The recall is also a setback to efforts to expand Brexafemme to other indications. A Phase 3 clinical trial was testing the drug in invasive candidiasis and other difficult-to-treat fungal infections. Though GSK has rights to the drug in all indications, Scynexis is responsible for this Phase 3 clinical trial. In the regulatory filing, Scynexis said the Brexafemme recall means a temporary halt to clinical tests of the drug until the company comes up with a mitigation strategy and resupply plan.

Manufacturing issue RESOLVED

RESOLVED

MM Thanks for helping all members here who hold SCYX allay their fears of something amiss but required only “steady as she goes” remarks (NOT)

The issue is resolved. As I write GSK Is manufacturing for sales and for MARIOstudy

So are you saying GSK is the new manufacturer and are they approved by the FDA to resume production? If not, what are you saying??

Mr Murphy, RIVN might be a bad deal for VW but it’s an excellent deal for RIVN. RIVN is now backstopped by VW AND Amazon. Currently you can order a new Rivian truck with delivery in 1-6 weeks and every (almost) every Amazon delivery I get now is via a Rivian Van. I test drove the R1T and it is every bit as smooth as my Model 3. I don’t need a truck but it is far more attractive that the Cybertruck.

You are correct that Rivian doesn’t offer FSD .. yet. Tesla has made it clear that they plan on selling FSD to the open market.

Note RIVN is up 9% today on no news.

I still maintain that any new VIABLE battery tech will come from Tesla, not ENVX ( which is currently riding all on hype).

You think Tesla makes batteries?

ENVX will make batteries for small devices like phones, if OEM customers approve their test samples, which hasn’t happened so far. Large batteries may be in the distant future for ENVX?

VERY distant. Moving from phones to CARS?? Come on man.

Agree. My tone in my last question was skeptical.

No, but you don’t think an 800 BILLION dollar company can partner/buy the best tech available? Silly comment.

Tintweezl on YMB for ENVX said that their tech is not state of the art–energy capacity, etc. Their battery is probably more fire-resistant than current batteries, which alone is a big plus. It is an improvement over current cell phone batteries. TintW favors AMPX which has better tech. But Musk is interested in state of the art tech for his car batteries, and ENVX probably won’t ever deliver on that.

VLD – Velo3D, Inc. Receives Continued Listing Standards Notice from the NYSE

Velo no longer in NYSE compliance as their market cap & stockholder valuation have both fallen below $50 million.

https://ir.velo3d.com/news-events/press-releases/detail/154/velo3d-inc-receives-continued-listing-standards-notice

Monday’s trading may see a temporary small decline in PPS, but it is a nonissue for 18 months. If VLD’s business gets going again, it’s a nonissue, but if BK occurs, nothing matters.

On YMB, I have a heated exchange with Bob, who insists that being NYSE listed is important. I point out that the RS was done to keep the PPS above $1, but it backfired because the market cap has declined drastically to below $50 million where they would get delisted anyway if their remedy plan is rejected by the NYSE soon. I believe that the market cap would have been higher if it had not done a RS. My position is that a company can trade on any exchange it is on. A company is judged on its business fundamentals, not on which exchange it lives on. What do you think?

MM?

I agree. Reverse splits are giving in to bullying

Thanks. Do you think VLD can raise money just as effectively if they are on a minor exchange? I think they did a great move by getting the lender to agree to repayment monthly instead of a big lump sum for the July 1 payment due. Either the lender figured they would never get any payment if VLD were to go bankrupt soon, or they had some confidence in the business to take payments stretched out over time. That lender wouldn’t care whether VLD was on NYSE or OTC/pink.

Why are you fishing around the bottom of the barrel with these bullcrap stocks? VLD is most likely going BK.

Buy established leaders like AMZN, GOOG, TSLA and for god’s sake keep with the profitable companies.

NWI stands for Net Worth Incinerator.

You’re right. Even my repeated averaging down has resulted in greater absolute losses in VLD. The problem with these well established companies is that valuations are expensive, so they are risky as well. I like Musk. Is TSLA the best of them? What’s your current strategy?

Yes they are but they are safe. At this point in my life, I don’t need home runs. I do have a couple spec stocks though. AXON owns the body cam market for police and military but has run up a lot. ENPH is very profitable but a trump presidency might kill it (solar).

I maintain a core position in TSLA always. I trade around it if the stock takes hits ( like last week). People don’t understand that long term, TSLA is an energy and an AI play. They aren’t just a car company.

Watch for earnings next week. They might miss deliveries but could be a great buy on weakness.

Thanks. Trump, like myself if I were President, would cut regulations and taxes which benefit all companies. All methods of energy production are important, and the best way is to let the free market decide what the balance will be among all the technologies. The question for solar stocks is whether they have gotten govt subsidies or other forms of favoritism. If that is the case, then they will do worse in the free market without govt intervention. Trump is not the ideal free marketeer because of his tariff policy, but most of his policies would produce more growth than Dem socialist policies.

Please help me, your lifetime subscriber for about 30 years. For whatever reason my email was out for over 3 weeks. Now that it is back I find that you are NOT Emailing my weekly Radar Report. I am only getting it thru pulling up a June report and logging in from there. I don’t want to go thru all that and get it late. Email it to norm21@cox.net.

Norm21

Readded. If Aweber gets a couple of weeks of bounces, they do stop emailing but they don’t tell me.

SCYX

Facts and opinion for those who care to listen:

1 FURI and CARES studies, the delivery is not considered material by GSK because the results are published on the SCYX website. fact

2 Delivery has taken place and milestone payment received. Opinion

3 As I write, manufacturing is taking place….SCYX for MARIO study and GSK for commercial sales. Fact

4Companies do not need FDA approval per se to manufacture, they only need the FDA to lift the hold, which is imminent, Fact

5 We may not get an announcement that the hold has been lifted, SCYX is unable to announce anything without GSK’S permission. opinion

6 I suspect a Q2 announcement similar to Q1 in mid August, there may be some releases before. At ths time we might get a slight bump in share price. Opinion

7 There will be a large infectious disease conference this fall. At this time GSK may wish to highlite the results of FURI and CARES. This may allude to commercialization based on the decent results…possibly a huge bump in share price to follow. Fact and opinion

8 Bottom line, stock is relatively safe ( in the hands of GSK)

Price: STUPID CHEAP!! Looking for additions and/or opinions

thanks zman

yes and that’s why im DCA down. the world needs better anti-fungal

I’d love to know where you got all this info. I just reviewed their site.

Your point 1. Where’s the latest CARES study data? NO, results are NOT on the website as of today. Did I miss it, where did you find it? Previous published reports in Sept 2023 were OK for resistant UTI’s at 86%, but only for 6 out of 7 patients. Tiny numbers. For intra-abdominal Candida infections, also small numbers of patients, 41% complete/partial response, 40% stable disease (this is not a cure). I call it all PISS POOR. My guess is that the latest promised results not published were mediocre, so they are trying to hide that info. Sure, this info is not material because it SUCKS, period. Most of the attention is on SCY 247, not Brexa. Brexa has been mediocre for VVC in sales numbers, and in efficacy–an expensive new drug only slightly better than cheap generic azoles. That’s what happens when patient care is solely about prescribing drugs. The solution to recurrent yeast infections is a no sugar diet that starves the yeast from growing in the intestines, the source of urinary, vaginal and systemic yeast infections. As an aside, I have a young 50 year old male patient without prostate disease who got a UTI from sitting in the bathtub for over 30 min habitually. I had that hypothesis, but his wife actually first made that assessment. The Enterococcus bacteria in the urine came from the rectum from inadequate wiping. Tell everyone you know not to take baths. But if you’re a mainstream doctor, tell them a new drug is coming out that is the panacea for your problems. CRAP GARBAGE STUPIDITY. Your wife is smarter.

Point 3. Where did you get that info?

Point 4. Gobbledeguck semantics. The FDA has not lifted the manufacturing hold, so no manufacturing yet.

Point 5. GSK should be eager to grant permission to release info that the hold has been lifted.

Point 8. Among small bios and from NWI, this stock is relatively safe. But it is not stupid cheap. We would get a better, guaranteed 5% annual return from a CD for the next few years, until and only if SCY 247 demonstrates good results. There might be a brief bump when the hold is lifted, then a modest decline for several years until and if 247 is approved.

Factual information is from several conversations with Investor relations. The remainder is speculation on my part based on some of the cryptic messaging from investor relations. I find no reason for there being dissemination of falsehoods. Of course they are limited in what they can tell you and not

Even with those facts, my main worry is the mediocrity of the FURI and CARES results. Brexa royalties and milestones will keep the company afloat. MARIO may boost sales of Brexa, but SCYX can only capture royalties and milestones from that. The bullish case rests on the success of 247 trials and sales. This won’t occur for quite a few years. The stock is fairly priced, but is not cheap.

Chaikin rates SCYX “very bullish” with solid financials (price to sales, free cash flow, okay LT debt to equity), good earnings growth and earnings trend, not good projected P/E, good industry relative strength and insider activity, not good short interest. Mostly poor technicals (money flow, price trend, volume trend) except good price strength.

Over the years I’ve lost more money on this stock than any other, trading in and out. SCYX looked potentially promising. I’m in now. Will see how it goes.

I put more weight on my impressions of 247 prospects and Brexa mediocrity I wrote above, rather than those generic metrics from Chaikin. I had been down from several buys many years ago at $10-20, until I bought more at $1.70 in Oct, getting my cost average down to $4.70. 247 will take years to prove itself. I am holding now. I am too overweight to justify buying more at current prices.

Why?

Dictator Till The End,

I stuck with SCYX off and on too long. (Still not as bad a financial loss as divorce! 😉 Usually bet smaller until a good trade seems likely. Cash in quickly, trading not investing.

Best investment trading ever for me was Arena ARTH post their corrupt initial rejection. Otherwise, Murphy’s picks and continuing guidance typically were not good. 90% of early stage biotechs go broke. Trade don’t invest in them. Lesson: Seek out better sectors to invest.

Arena (ARNA) was good for me, although my mistake was not selling at $12-13 on approval, and listening to MM’s advice to hold on for EU approval of Belviq. I rode it down to $4 before selling most at a small profit. The remainder I held until they re-incarnated themselves in autoimmune diseases. They got a great buyout at $90, post 10 fold reverse split, still $9 pre-split where I made good profits on my remaining position.

You’re right about your statements.

MM, Did you know something we didn’t . Worried about ASSASSINATIONS ?

I agree with MM. I think this is going to be the mother of all elections. The lunatics will come out of the woodwork since they have been spoon fed with so much bullshit from various news outlets over the past several years. Case in point, the Pennsylvania gun fight. Which by the way I think the secret service did a horrid job of providing adequate security. They dropped the ball on the setup for success. That rooftop where the shooter was should have had many eyeballs on it prior to and during the rally. What the hell were they thinking? The only saving grace was that it was some 200 yards away and it created a challenging situation for a 20 something kid with no sniper experience.

Trump was really lucky that this kid tried to shoot him with an AR-15 rather than a scoped rifle. Really lucky.

It won’t move the needle though, trump/vance are an extremely dangerous pair and the country knows it.

None is so blind as he who refuses to see.

I agree. Put on some glasses.

The shooting in Pennsylvania did one good thing . It got Trump elected. What if that was a rally for grandpa Joe? And he got shot at? Have you watched him walk off stage or up the stairs to his plane? He moves like a sloth. He is too damn old. That’s dangerous. He can barely make it thru this term , how in hell is he going to make it through another one? But if you listen to his press secretary, and the bias media he is sharp as a tack, can run a mile a minute, has the mental capacity of Elon Musk and can stand on his head and do a juggling act. China, Russia, and North Korea are watching his every public appearance. The only reason they haven’t attacked the US is that they have their hands full with other more pressing issues. Ukraine, Taiwan, South Korea, Iran, Isis, and the list goes on. That’s what I can see and I don’t wear glasses. Democrats will come out of hibernation sooner or later and kick him to the curb for another also ran candidate before November.

Agree. However, the mainstream media and Wall Street jumped on Trump today when he said he would get Taiwan to pay for US military help. Taiwan Semi, my biggest win and hold from 30 years of subscribing to MM, lost 6% today, and the whole chip sector had similar losses. Despite my hope that the CCP doesn’t invade and take over Taiwan, all foreign aid has to be paid by the beneficiaries, otherwise the US will go even more broke. We will still provide military support, but if these countries know how important it is to them, they will step up and pay, the ethically proper thing to do. They cannot remain high class welfare recipients.

Agree.

MM or anyone. Glad UUUU ticked up. I bought 03-2022 on the initial recommendation, and it’s down 35% +/- since. Not many other uranium plays have performed so poorly in that time period.

It still lags way behind SRUUF Sprott Uranium and CCJ Cameco. What will move UUUU up to be comparable? Wouldn’t it be wiser to own either of the 2 mentioned alternatives ?

Miners ususlly move more than the metal. UUUU is smaller and riskier than CCJ but has more upside.

On June 17, I announced my asymmetrical bet on a Trump victory, NAK, which I bought under 28 cents. Four weeks later, it’s over 36 cents. Another one I liked was private prison operator CXW which had plummeted in June from the $15-16 range to the $11 to 12 range. Today it has jumped to around $14.50.

Murph’s picks for a Biden victory were SWBI and RGR which were both trading lower over the last 4 weeks. NOT ANYMORE! Both jumped this morning over 10% before turning back. Nothing like a political violence to move the price of the doom stocks.

TSLA is now a MAGA stock, get on board you right wingers. Seems odd though, trump hates electric cars. Is Elon playing 3d chess?

Right wingers don’t think a persons vehicle choice should be mandated. What a crazy idea.

Nobody is mandating anything. You are free to buy your gas guzzler.

Michael, you should re-examine your position on ENVX. Keep in mind they are making very small batteries, not the bigger ones that go into vehicles. All they have to do to be a smashing success is become the leader in the small battery market.

After that maybe they can compete in the bigger battery market.

I might when it gets back down where it belongs .. below 10.

Stocks with negative earnings are going to get hammered in the trump recession.

I’m going to cash, for the most part.

What do you think of YMB poster Tintweezl who says that ENVX doesn’t have state of the art tech for even very small batteries? I posted several paragraphs from him a few weeks ago here. TintW is usually a short trader, but he went long on AMPX a few weeks ago because of their superior tech and much cheaper valuation vs ENVX. The risk with AMPX is lack of financial backing to mass produce their superior batteries.

Without money, AMPX is irrelevant.

Maybe true. However, every successful big company starts out small. A young engineer solves a problem, impresses his friends who then help fund small production. Things work out, more people get involved, in a snowball effect. What’s the difference between the group of Apple, Google, Microsoft, AMD, Nvidia, Dell, Tesla, and the tiny AMPX?

MM, food for thought?

New World Investor for 7.18.24 is posted. I added AKBA to short-term Top Buys after a terrific CEO presentation at Wainwright.