Dear New World Investor:

We got the May Personal Consumption Expenditures Index (PCE) report last Friday morning. Year-over-year headline inflation cooled to 2.6%, the lowest in three years. The Fed pays close attention to the core PCE, which excludes volatile food and energy price changes. Core PCE also was up 2.6% year-over-year in May, in line with estimates. The month-over-month core PCE rose 0.1%, also in line with Wall Street’s expectations and slower than the 0.3% increase seen in April.

It was a good report. According to the CME FedWatch tool, investors expect the Fed to hold interest rates steady at the July 31 meeting but see a 66% chance the Fed will cut rates twice by December.

This Friday’s June payrolls report and next Thursday’s Consumer Price Index release probably will set the tone for the overall market, especially after Fed Chairman Powell said “we are getting back on a disinflationary path.” Of course he had to add the mandatory “the central bank will need to see more evidence before cutting interest rates.”

No matter which party holds the Presidency, in an election year it’s always hard to predict data releases and the often-quiet, often-large revisions of previous releases. I think what’s really going on is weak payroll numbers and a slow increase in unemployment that will continue throughout the year. Job cuts have been fluctuating and trending up – this is NOT what an economic expansion looks like.

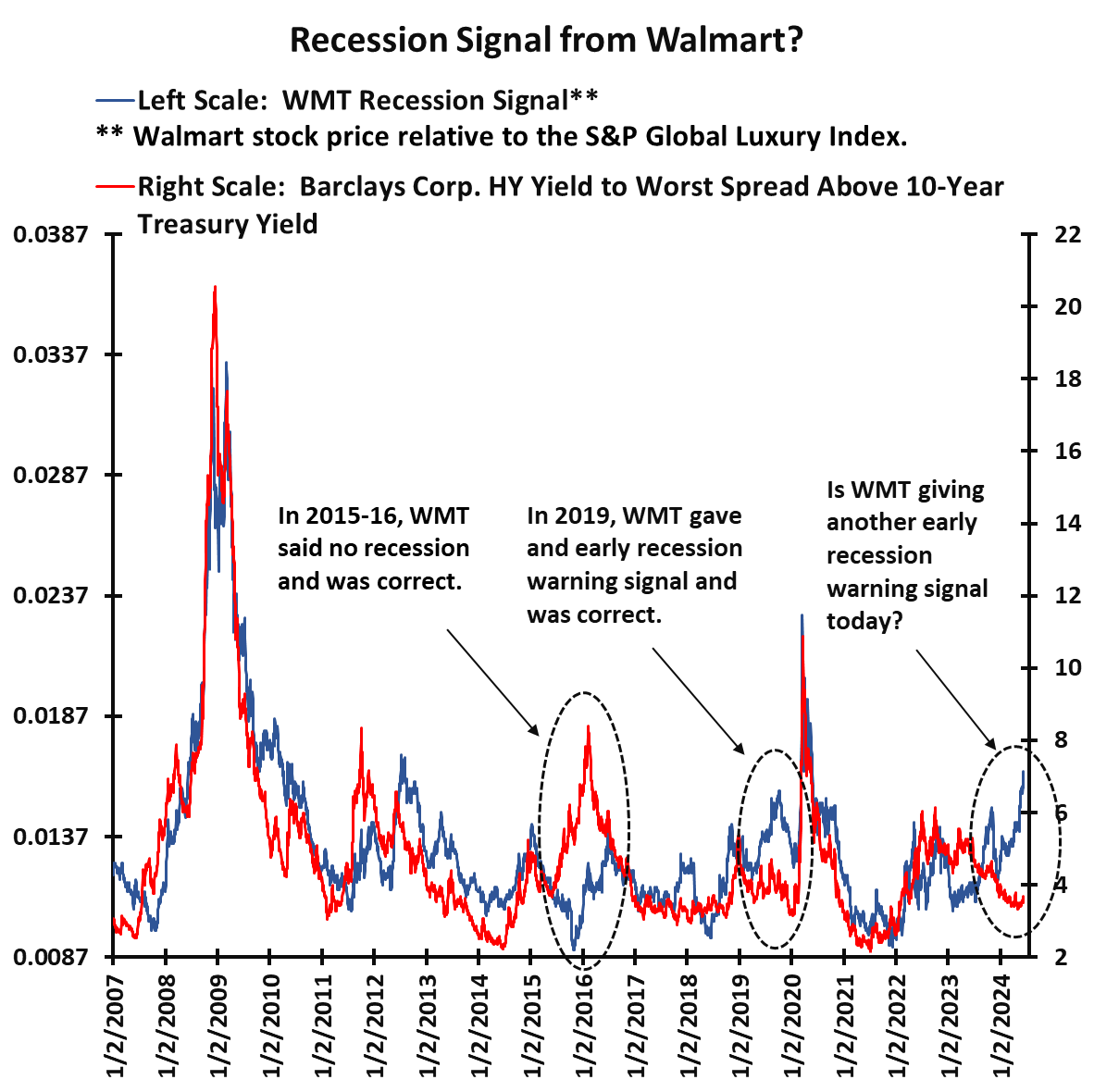

![]()

Click for larger graphic h/t @MacroEdge

The Walmart Recession Signal, developed by Paulsen Perspectives, “compares Walmart’s stock price performance to a group of stocks whose businesses are tied to the wealthiest parts of the economy – the S&P Global Luxury Index. As economic activity slows and recession risk builds, retailing purchasing patterns tend to gravitate toward discounters like Walmart and away from luxury retailers. Consequently, a rise in the WRS could warn of a potential recession.

“The accompanying chart overlays the WRS (blue line) with corporate credit spreads (red line). Since 2007, the WRS and corporate credit spreads have moved closely. When recession risk builds credit spreads often widen and spending trends typically are driven toward Walmart and away from high end retailers. Both the WRS and credit spreads provide similar recession warnings. What is most interesting, however, is when they diverge.

Click for larger graphic h/t @jimwpaulsen

Click for larger graphic h/t @jimwpaulsen

“In 2007, both correctly began warning about an approaching recession which ultimately was the Great 2008-09 Recession. In 2015-16, however, when credit spreads widened significantly to about 8%, implying another recession was nearing, the WRS remained docile – ‘correctly’ indicating that credit spreads were giving a false signal about a near-term recession. Then, in the last half of 2019, while credit spreads stayed tight, suggesting the economy was healthy, the WRS spiked higher and ‘correctly’ gave investors an early warning of the 2020 pandemic recession.

“Since the end of 2023, credit spreads and the WRS have again parted company. Credit spreads have been tightening all year and currently remain close to historic lows, suggesting a lack of any significant financial pressures and an economic expansion which remains healthy. Meanwhile, the WRS has been increasing all year and currently stands at its highest level since the 2020 recession. Credit spreads suggest balance sheets are strong, which should dampen recession risk. But the WRS advises caution since retail purchasing is trending toward discounters, suggesting pressures may be building among lower income consumers. The last two times these recession gauges disagreed, it was best to be attentive to the WRS. which eventually was proved correct.”

Market Outlook

The S&P 500 added 1.0% since last Thursday to yet another all-time high today. It is up 16.1% year-to-date. The top 10 US stocks now account for 37% of the market capitalization of the S&P 500, the highest concentration in decades. Even the 27% concentration reached at the height of the dotcom bubble in 2000 has been surpassed. Most people are worried about that – just check the stories on your favorite finance site.

What they are missing is that profits in the Index also have never been as concentrated in the top 10 stocks as they are today. In 2000 the top 10 accounted for just 15% of the S&P 500’s earnings. Today it’s over 25%.

Click for larger graphic h/t High Growth Investing

The way this gets corrected (and it never lasts) is for the other 494 companies to attract investors as AI spreads through the economy, increasing revenues and cutting costs. The Magnificent 6 don’t need to crash and can keep going up as long as the other ones go up faster.

The Nasdaq Composite gained 1.8% and closed right on its latest all-time high today. It is up 21.2% for the year and outperforming most managed money, including hedge funds. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 2.1% as the biotech sector weakness resumed. It is clinging to a 1.8% gain year-to-date. The small-cap Russell 2000 edged down just 0.1% and is clinging to an even smaller 0.5% gain in 2024. The Russell had its worst first half of a year in history.

Click for larger graphic h/t @WinfieldSmart

The fractal dimension Magical Mystery Tour continues with the fractals in record low territory. The coming consolidation will be either uncomfortably long or uncomfortably sharp. Buckle up, cowpokes.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for June quarter real GDP growth was cut in half from +3.0% on June 27 to +1.5% this morning due to weaker personal consumption expenditures growth and gross private domestic growth. GDPNow’s forecast is lower than the Blue Chip economists for the first time in years.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, July 5

June Payrolls – 8:30am – +190,000 expected: May was +272,000

Monday, July 8

AG – First Majestic – Through 7/11 – Rule Symposium on Natural Resource Investing

Wednesday, July 10

Short Interest – After the close

Thursday, July 11

Consumer Price Index – 8:30am

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $220.94) introduced Apple Vision Pro in Apple Store locations across the China mainland, Hong Kong, Japan, and Singapore. Customers can book a personal one-on-one demo of Vision Pro to experience spatial computing.

Bloomberg News reported that iPhone shipments in China soared 40% in May amid retail partners cutting prices of the device by offering attractive discounts ahead of the country’s June 18 shopping festival. The China Academy of Information and Communications Technology disclosed figures that showed smartphone shipments rose more than 13%, but foreign brands, mostly Apple, grew almost four times faster.

iPhone sales slumped 37% in the first two months of 2024, then climbed about 12% in March. In April, iPhone shipments in China surged about 52%. I am moving AAPL to a Hold and planning to move it back to a Buy under $175 for new iPhone rollouts and augmented/virtual reality products.

Meta Platforms (META – $509.89) said Threads now has over 175 million monthly users and the rumor is they might start selling ads on that platform.

Raymond James reiterated its Strong Buy rating on Meta because the Generative AI nearly-$40 billion monetization opportunity is underappreciated. They raised their target price from $550 to $600 to reflect their bullish stance on GenAI monetization across Llama and consumer/business ad opportunities on the platform. They believe the Llama/open-source strategy is well positioned in enterprise and some combination of business and/or consumer AI to improve ad monetization with minimal core social business risk.

They also raised their 2025 capital spending estimate for Meta near a Street-high $50 billion, which places a modest degree of gross margin pressure because every incremental $10 billion is about a 1.25 percentage point gross margin headwind. They believe Meta’s nearly 350,000 Nvidia H100 footprint covers the Large Language Model Llama 4, but factor in a 2025 Llama 5 B200 build. So they lowered their 2025 earnings estimate by 3% to $24.26. I am moving META to a Hold and planning to move it back to a Buy under $400.

Palantir (PLTR – $25.98) software is used by AARP to cope with infrequent membership renewals, difficulty in projecting renewal figures, and understanding the key drivers behind membership renewals. By creating a digital twin of AARP’s business, Palantir enabled AARP to assess the effectiveness of their marketing across various customer journeys.

A standout feature of this partnership is AARP’s “Next Best Member Offer” model, an AI-driven methodology that provides dynamic, personalized member benefits, thereby driving higher conversion rates and membership renewals.

Palantir’s AIP Bootcamps are really working. Their commercial customer count is growing rapidly. In the March quarter, that translated to a 40% year-over-year increase in US commercial sales to $150 million and 27% worldwide commercial sales growth to $299 million.

Click for larger graphic

PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $59.50) stock keeps slipping, but it’s trading at 14.8x last 12 months’ earnings and is expected to grow earnings per share 15.93% a year for the next five years. In contrast, Visa (V), with a $560 billion market cap and a P/E ratio of 30.6x, is an expensive stock. PayPal gives you exposure to the digital payments industry and their new Fastlane product aims to be the fastest way to checkout for online shopping.

Customers seem to like it:

Susquehanna upgraded the stock from Neutral to Positive yesterday, saying the company is now focused on profitable growth, making it time to snap up the stock. But they just maintained their $71 target. They said margins have gotten squeezed because PayPal’s unbranded payment-processing business, Braintree, has had solid growth but lower profit margins. They think the solution involves pricing discipline and a re-emphasis on incorporating more value-added services.

Beyond that, a stronger presence for PayPal Complete Payments, an unbranded product for small and medium-size businesses, would also boost margins. PYPL is a Buy under $68 for a double in three years.

Small Tech

PagerDuty (PD – $22.07) surveyed 500 IT leaders of US, UK, and Australian companies with more than 1,000 employees and found that customer-facing incidents increased by 43% during the past year, with each incident costing nearly $800,000. The average incident takes nearly three hours to resolve (175 minutes) while the estimated cost of downtime is $4,537 per minute, meaning each incident can cost nearly $794,000. Respondents’ organizations saw an average of 25 high-priority/priority incidents in the last 12 months, so the cumulative costs add up to just under $20 million per year, per organization. PagerDuty’s software reduces the number of incidents and dramatically reduces incident response time. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Velo3D (VLD – $3.11) filed a couple of 8-Ks. On Monday, the note holders agreed to defer the July 1 partial redemption payment of $10.5 million over a period of ten equal monthly payments beginning August 1. They got 1,650,000 five-year warrants exercisable at $3.

Then the company said that with the appointment of Brad Kreger as the CEO, the compensation committee of the Board of Directors increased his base salary from $380,000 to $460,000 and his target bonus for fiscal year 2024 to 70% of his increased base salary. It’s hard to believe they would do that if VLD had a bad June quarter. VLD is a Buy up to $10 for my $100 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $6.22) completed their COMP-360 launch team by hiring a Chief Commercial Officer from Axsome Therapeutics, where she was head of commercial and business development and, most recently, head of product strategy. She played an integral role in bringing Axsome from clinical-stage to commercial-stage and was responsible for formulating their commercial launch strategy and scaling the commercial organization. Previously, she launched multiple CNS-focused drugs during 10 years at Amgen. Her appointment as CCO follows the new CFO in March and Chief Research & Development Officer in May.

Management did an excellent fireside chat at the H.C. Wainwright Neuro Perspectives Virtual Conference (AUDIO HERE) and participated in a panel discussion on “Commercialization of Novel Compounds in Psychiatry” (AUDIO HERE).

In the fireside chat, they said their Phase 2 trial was groundbreaking in terms of its size with over 200 patients in 22 sites. It and the current Phase 3 trials were designed to meet the placebo objection that sunk Lykos Therapeutics’s MDMA drug. They have aligned with FDA guidance, especially on functional unblinding.

Management specifically addressed the Lykos situation at 15:00 and easily differentiated themselves. MDMA is not a classic psychedelic and has a very different mechanism of action. Lykos submitted “MDMA-assisted psychotherapy” and the Advisory Committee couldn’t tell how much of the benefit was from the therapy and how much from the drug. Compass is submitting “drug therapy with psychological support.” Instead of Lykos’ non-specific psychotherapy, Compass will submit details on how they trained doctors to offer specific psychological support.

The adverse decision on the Lykos filing should never have impacted Compass’ stock, yet it was knocked down over 24% to its intraday low. That’s nuts. We will get the first Phase 3 top-line data soon and the second trial data in mid-2025. I firmly believe they will get approval early in 2027. This is a clear case of Wall Street making a major mistake – take advantage of it. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Inovio (INO – $8.39) was re-added to the Russell 2000 Index, not that that’s been a good place to be in this Big Tech market. There’s no doubt the small cap stocks are relatively undervalued and the pendulum will swing someday. In the meantime, CEO Jackie Shea said: “Being re-added to the Russell 2000 signifies the value of the progress we have made recently and our commitment to the next level of our strategy, which includes our plans to submit a BLA for INO-3107 under the FDA’s accelerated approval pathway in the second half of 2024 and preparing to be commercial launch-ready in 2025, should INO-3107 be approved. We also continue to work to advance other product candidates, including the next steps for INO-3112 in head and neck cancer, INO-5401 in GBM, and INO-4201 as an Ebola vaccine booster. We look forward to sharing our progress on these and other programs as the year unfolds.”

INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

Medicenna (MDNAF – $1.38) reported results for the March fiscal year. They lost $25.5 million or 37¢ a share. They said they are still looking for a partner for MDNA55. With its compelling survival benefit in recurrent glioblastoma, the most aggressive form of brain cancer that lacks a standard of care, they are spending a little money to get Breakthrough Therapy Designation with the FDA. It already has FastTrack designation from the FDA and Orphan Drug status from both the FDA and the EMA.

The proposed Phase 3 trial design incorporating a hybrid external control arm has been accepted by the FDA. Medicenna is currently working toward securing alignment with the European Medicines Agency, thereby enabling data from a single Phase 3 registrational trial to be sufficient to file for approval in the EU and the USA. The goal is to make MDMA55 an even more attractive asset to get a partner for the Phase 3.

They now have $37 million in cash, thanks to the $20 million investment on April 30 by RA Capital. That extends their cash runway through 2025 into mid-2026. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

Inflation MegaShift

Gold ($2,369.40) wrapped up its third straight quarterly gain last Friday after the PCE report. It continues to trade solidly over $2,300 in spite of the dollar’s strength. As soon as the Fed starts to cut interest rates, gold should soar.

John Hathaway, Senior Portfolio Manager of Sprott Asset Management, told Kitco that $3,000 gold within the next year is “not crazy” in the current economic and geopolitical environment, and the implications on mining stocks are profound.

Hathaway said: “There’s a huge mean reversion trade ahead of us, assuming gold prices stay at these levels. And then I could make an argument for why they could move even higher, if and when people lose their degree of comfort and complacency with how they’re currently positioned. I think that lies ahead, and that’s why I would say we are at the cusp of a big move in mining stocks even if the gold price stays where it is.”

The fractal dimension is nearly fully consolidated and ready to support another upleg even with gold near its recent all-time highs. There’s nothing like a consolidation due to churning over time instead of a sharp retracement to drive the bears nuts.

Miners & Related

Coeur Mining (CDE – $5.97) reported continued positive results from their multi-year exploration drilling and development program at the Kensington underground gold mine in Southeast Alaska. They said recent assays show the potential to extend its reserve-based mine life to over five years by year-end.

Kensington consists of multiple deposits including the Kensington, Elmira, Raven, Johnson and numerous other prospective vein zones. In the upper area of the Kensington deposit, previously outlined zones appear to be converging into single, wider mineable areas. The newly discovered Zone 50 in lower Kensington is growing rapidly, resulting in the development of additional exploration drifts to facilitate infill drilling before the end of this year. At the Elmira deposit, the Main and South zones have now been connected through infill drilling and expansion drilling is intersecting multiple wider zones to the south. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin‘s (BTC-USD on Yahoo – $59,671.95) proportion traded over weekends has declined from a high of 28% in 2019 to an all-time low of 16% this year, according to cryptocurrency research firm Kaiko. The drop comes after the launch of spot bitcoin exchange-traded-funds, which seem to have shifted the periods when bitcoin is traded to be more in line with the schedule of traditional equity exchanges and has lowered its price volatility. That’s a good thing – it means bitcoin is becoming a more mature asset that will be more acceptable to traditional investors.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $34.37) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $83.88

The Energy Information Agency’s badly flawed Adjustment Factor has been showing false crude inventory increases that kept a lid on oil prices. It is about to reverse, showing monster inventory draws. With the Middle East on edge even more than usual and deeper OPEC+ cuts about to print in mid-July, led by Saudi Arabia, now is the time to have your maximum exposure to oil.

It’s very much a contrarian call. Oil inventories are starting to draw, so market participants are overly bearish. Oil demand is healthy and trending higher. OPEC+ can always extend the voluntary production cut past the December quarter if needed. Yet energy fund investors are bailing at the fastest rate in over a year:

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Global oil inventories are still low:

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

I expect President Biden to release another 30 million barrels or so from the Strategic Petroleum Reserve starting in August to try to bring gasoline prices down before the election. That would keep crude rangebound between $80 and $95 through the end of the year, but set us up for prices over $100 in 2025.

The July 2026 Crude Oil Futures (CLN26.NYM – $71.71) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $41.25) is a Buy under $40 for a $100+ target.

Freeport McMoRan (FCX – $50.70) will be a major beneficiary of the copper shortage. There have been only TWO major copper discoveries since 2015. That’s 8½ years and billions of dollars of investment for very little discovery.

Click for larger graphic h/t @marketplunger1

The company had good news and bad news. The good news: Their Indonesian subsidiary, PT Freeport Indonesia (PT-FI), substantially completed construction of its new smelter in Gresik, Indonesia, in June and has commenced commissioning operations. Freeport expects the smelter will begin producing copper cathodes in the coming months and continues to target full ramp-up by the end of 2024, in line with previous expectations. The completion of the project positions PT-FI as a fully integrated producer in Indonesia, providing a foundation to extend its long-term operating rights.

On July 2, PT-FI received approval from the Indonesian government to export copper concentrates and anode slimes through December 2024, when the full ramp-up of the new processing facilities is expected.

The bad news: PT-FI’s prior concentrate and anode slime export licenses expired on May 31 so they could not export copper concentrates or anode slimes during June. As a result of the export license delays, management expects a portion of its June quarter production will be shipped in future periods. So June quarter revenues will be about 5% below their April guidance of 975 million pounds of copper and about 30% below guidance of 500,000 ounces of gold.

More bad news: Consolidated unit net cash costs for the June quarter, previously estimated at $1.57 per pound of copper, are currently estimated at $1.77 per pound, principally reflecting lower by-product credits as a result of the delay in shipments, especially of gold.

More good news: They do not currently expect a material change to their annual 2024 copper volume guidance. As a result of a change in mine sequencing principally to address wet conditions in certain of the Grasberg Block Cave draw points, 2024 gold sales are expected to approximate 1.8 million ounces compared with previous estimates approaching 2.0 million ounces. This change is a timing issue and not expected to affect long-range plans.

They’ll announce quarterly results on July 23. This is the most transient of issues and should not affect the stock’s future. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

EVs are giving new owners more headaches, and Tesla is a big reason why: J.D. Power study

Click for larger graphic

Click for larger graphic

* * * * *

Your wondering Does Coffee Cause Cancer? Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 7/3/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $38.26) – Buy under $33, target price $60

Gilead Sciences (GILD – $66.94) – Buy under $80, target price $120

Palantir (PLTR – $25.98) – Buy under $22, target price $100+

PayPal (PYPL – $59.50) – Buy under $68, target price $136

SoftBank (SFTBY – $33.35) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $15.28) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.39) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $7.40) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $22.07) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $10.46) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.63) – Buy under $13, target price $30+

Velo3D (VLD – $3.11) – Buy under $10, target price $100

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.71) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $0.95) – Buy under $2, target $20

Compass Pathways (CMPS – $6.22) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $4.63) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $8.39) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.38) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.94) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $18.65) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($30.84 – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.66) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $32.47) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.66) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $32.57) – Buy under $30, target price $50

Coeur Mining (CDE – $5.97) – Buy under $5, target price $20

First Majestic Mining (AG – $6.22) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.43) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.66) – Buy under $10, target price $25

Sprott Inc. (SII – $43.04) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $59,671.95) – Buy

iShares Bitcoin Trust (IBIT – $34.37) – Buy

Ethereum (ETH-USD – $3,303.18) – Buy

Grayscale Ethereum Trust (ETHE – $30.66) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $71.71) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $41.25) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.36) – Buy under $11; $24 target

EQT (EQT – $37.28) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.93) – Buy under $8; $30 target

Freeport McMoRan (FCX – $50.70) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $220.94) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $509.89) – Expect to move back to Buy under $400

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

Happy 4th

HAPPY FOURTH OF JULY

THANK YOU FOR ALL THAT

SERVED!!!

MM–your economic analysis suggests a mild recession with soft landing. Interest rates should be cut soon, and the market should continue up. On the other hand, fractals suggest correction. Which is correct? If fractals dominate, does the SP500 get a 10% correction to 5000?

A long sideways consolidation through the election is the other possibility. I’d put the probabilities at 50% for the sideways consolidation, 40% for the 10% correction, and 10% for the continued rally. The big surprise could be that the Fed cuts and the market doesn’t rally due to earnings estimate cuts in a weaker economy.

So there is a 90% chance that our stocks will decline during this period vs 10% chance they rise, other conditions being equal. Watch for better buying opportunities during this period.

Amen to that.

MM–on AKBA, by waiting nearly a year before sales under TDAPA begin, aren’t they giving up that amount of time of patent protection? This is a negative factor. Their justification is that they want to come out with a big launch from incentives that all parties get higher TDAPA payments. But what happens when TDAPA is over in at most 3 years? Will marketing partners lose interest because the payments will be lower? They are banking that Vafseo will be a well-established standard of care, preferable to IV ESA’s from Amgen. Maybe, but marketing is always needed, even when sales are doing well. Look at Ocrevus. They are well established, but TV ads are still going strong. They know that otherwise, their sales would peter out.

Please comment.

Vadadustat has patents until 2042 that could be extended. They do lose 9 months, but it’s not material. You are right that their strategy is Vafseo will become a well-established standard of care, preferable to IV ESA’s from Amgen.

Makes sense, thanks. The only drawback is that marketing has to be perpetual throughout the life of the patent. Doctors may learn that V is the standard of care, but new dialysis anemia patients need TV ads so they can ask doctors to prescribe it. The same is true of every patented drug. When the 3 year TDAPA period is over, the dialysis centers will have less incentive to push for V, and the marketing muscle of Amgen may re-establish ESA sales they lost to V.

Could be. That’s a 2029 worry. We’ll probably be out of the stock by then.

Most companies have lower than expected sales after approval. DNDN, ARNA, to say nothing about wipeouts like NVTA, ARTH. Mediocre sales with mounting net losses from Auryxia from KERX is a bad omen about possible poor marketing for Vafseo. Terrible AKBA management with Butler collecting an inappropriate high $3 million dollar salary presiding over shareholder value destruction. Data for Daprodustat is hard to come by. Vafseo may succeed, but the odds of good investment results are poor in the short/medium term. We may be stuck as a bag holder in 2029, hoping for better results in 2030 and beyond.

Does anyone have any comments as to what the 5 year return might be on Velo3D. Is this the sleeper that MM thinks it is and just how much is it at risk? Thanks Ron C

I don’t know whether VLD will go bankrupt, be bought for a pittance, or somehow squeak through to MM’s optimistic target of $100 ($2.86 pre-split). If you were shrewd to not yet bought since MM’s reco at $10 pre-split, you can figure out your expected return from either wipeout, buyout at 50% higher than today’s price, or MM’s lofty 32 fold eventually. Read the YMB from astute investors Lazerator, Full Safe Driving, dealwithit, PatrickHenry, UWHuskies, Bob (not too recent). Most are guarded bulls who may be getting ready to give up if the Aug Q2 earnings report shows few sales. Brent is the most realistic commentator here.

That’s the most honest answer I can give.

What’s with SCYX another delay?

How about an “Evreything all at once” moment:

Second quarter report

Approval of Manufacturer and resumption of sales

Marketable results from delivery of final reports to GSK

Milestone payment from GSK

Halt in SCYX and opens at $6.50 on buyout from GSK

Corning Expects Second-Quarter Core Sales to Exceed Guidance, with Core EPS at the High End of or Slightly Above Guided Range

–MM what’s going on with SCYX. Reached out to pr but no response. Is there another delay, problems with the last two studies (doubtful),? Is it possible that GSK could drop them flat(again doubtful)? or is this normal, that is, “on or about EOQ”, It is at this point my largest holding by far and I would rather not lose sleep over it. SHOULD I BE WORRIED?

Right. Where are FURI, CARES results? I don’t trust the FDA to approve the new manufacturing soon. Typical inefficient govt.

Thank for your supportJG. I am reluctant to use the term misery loves company, and I hope this is not what it is. Market action seems to say we aren’t the only ones that are in a holding pattern. If f you look at Q1 release, it appears a lot of news could be received on August12(expected release date) I wish MMurphy would check it out.

MM any insight on delay with SCYX?

I guess you are extrapolating from Q1 that Q2 earnings report would be Aug 12. That’s fine for earnings, but it was expected that by the end of June we would get results of FURI, CARES trials. This is material, crucial info and shouldn’t wait until a convenient Aug 12. Since earnings are predictably based on royalties and milestones, I am not excited about that. But FURI and CARES are about use of Brexa in serious fungal infections. I was never impressed with Brexa for VVC, but the trials for serious fungal infections seem to be better designed, and the real money is in the treatment of serious infections. If FURI and CARES show good efficacy, we won’t have to wait for SCY 247 to make it through the lengthy 3 year trials before getting that revenue. The stock should get a shot in the arm upon release of good FURI and CARES data, and a booster shot when the manufacturing problem is resolved and the MARIO trial can begin.

I agree, there are material gains to be had from immediate adoption as a stepdown oral admin for serious infections with tremendous savings in money and time so what is the holdup? MM always seems to go AWOL at the most critical times. At the very least he could say that he is not privy to any other info

As an aside, cipro is a well established antibiotic used for mild and serious bacterial urinary infections. Blood levels from oral use are comparable to from IV use. IV use would be for the patient who can’t swallow capsules, or if serious illness inhibits GI absorption of oral capsules.

Step-down use of Brexa would be very important, as you say. I think only the MARIO trial address this. But this won’t be done until the FDA gets off its badass bureaucracy and approves the new manufacturing of Brexa.

Iam not sure but what Murphy told me is that resumption of step down use was not dependant on completion of MARIO but on FURI and CARES and the website supports this but not the IV application. .I believe both studies had decent results previously released so I do not believe that it is material release. So the holdup must be FDA related to manufacturing approval?

Hey MM your insights are appreciated, a lot of SCYX holdees wondering whats going on??

Interesting day so far.

ABCL +10.9%

AKBA +10.2%

EDIT +8.5%

INO +15.1%

MDNAF +3.6%

SCYX +10.7%

TGTX +4.5%

Picking cherries?

Agree. Any news or update on SCYX would be appreciated in today’s report.

Hello Mike, I am a lifetime subscriber, but I had trouble with my Email due to a Cox.net transition, which they fixed after 3 weeks of effort. But now I am NOT receiving the newsletter. I had to jump in through an old one I had saved. Please restore my email to your distribution. It is norm21@cox.net. Thank you If there is a problem, send me another way to respond to you.

New World Investor for 7.11.24 is posted. Added CMPS to Near Term Top Buys.